Pc 591 Michigan PDF Form

In the labyrinth of legal documents that navigate the distribution of assets after someone passes away, the PC 591 Michigan form, sanctioned by the State of Michigan Probate Court, stands out for its use in concluding the unsupervised administration of an estate without the need for a hearing. This form permits the personal representative of the estate to legally declare that they have completed all necessary tasks, including the settlement of claims, payment of estate and administration expenses, as well as taxes, and the distribution of assets to rightful heirs. Furthermore, it requires the personal representative to notify all involved parties, including those with unsettled claims and the distributees of the estate, thereby ensuring transparency in the estate's closure. Additionally, it provides a mechanism for interested parties to raise objections within a specified period, thereby embedding checks and balances within the estate administration process. Complete with details regarding any outstanding Michigan estate or inheritance taxes and modifications to the list of interested persons originally filed, the form, detailed in its requirements, aims to safeguard the interests of all parties and facilitate a clear path to the estate's closure.

Preview - Pc 591 Michigan Form

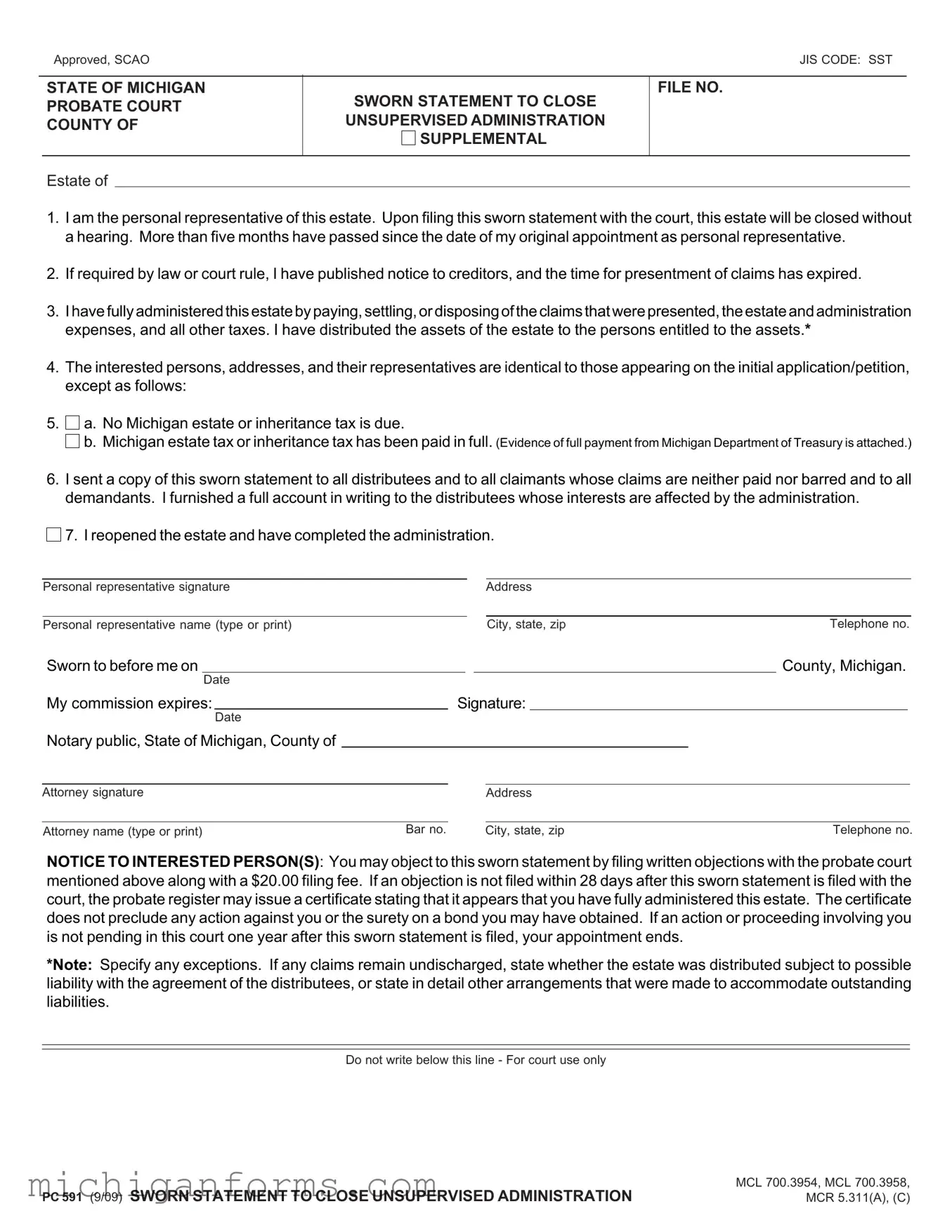

Approved, SCAO |

JIS CODE: SST |

STATE OF MICHIGAN PROBATE COURT COUNTY OF

SWORN STATEMENT TO CLOSE UNSUPERVISED ADMINISTRATION

SUPPLEMENTAL

SUPPLEMENTAL

FILE NO.

Estate of

1.I am the personal representative of this estate. Upon filing this sworn statement with the court, this estate will be closed without a hearing. More than five months have passed since the date of my original appointment as personal representative.

2.If required by law or court rule, I have published notice to creditors, and the time for presentment of claims has expired.

3.

4.

5.

6.

Ihavefullyadministeredthisestatebypaying,settling,ordisposingoftheclaimsthatwerepresented,theestateandadministration expenses, and all other taxes. I have distributed the assets of the estate to the persons entitled to the assets.*

The interested persons, addresses, and their representatives are identical to those appearing on the initial application/petition, except as follows:

a. No Michigan estate or inheritance tax is due.

b. Michigan estate tax or inheritance tax has been paid in full. (Evidence of full payment from Michigan Department of Treasury is attached.)

I sent a copy of this sworn statement to all distributees and to all claimants whose claims are neither paid nor barred and to all demandants. I furnished a full account in writing to the distributees whose interests are affected by the administration.

7. I reopened the estate and have completed the administration.

Personal representative signature |

Address |

|

|

|

|

|

|

Personal representative name (type or print) |

City, state, zip |

Telephone no. |

|

Sworn to before me on |

|

|

|

|

|

|

|

County, Michigan. |

||||

|

Date |

|

|

|

|

|

|

|

|

|

|

|

My commission expires: |

|

Signature: |

|

|

|

|||||||

|

|

Date |

|

|

|

|

|

|

|

|

|

|

Notary public, State of Michigan, County of |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Attorney signature |

|

|

|

|

Address |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Attorney name (type or print) |

Bar no. |

|

|

|

City, state, zip |

Telephone no. |

||||||

NOTICE TO INTERESTED PERSON(S): You may object to this sworn statement by filing written objections with the probate court mentioned above along with a $20.00 filing fee. If an objection is not filed within 28 days after this sworn statement is filed with the court, the probate register may issue a certificate stating that it appears that you have fully administered this estate. The certificate does not preclude any action against you or the surety on a bond you may have obtained. If an action or proceeding involving you is not pending in this court one year after this sworn statement is filed, your appointment ends.

*NOTE: Specify any exceptions. If any claims remain undischarged, state whether the estate was distributed subject to possible liability with the agreement of the distributees, or state in detail other arrangements that were made to accommodate outstanding liabilities.

Do not write below this line - For court use only

|

MCL 700.3954, MCL 700.3958, |

PC 591 (9/09) SWORN STATEMENT TO CLOSE UNSUPERVISED ADMINISTRATION |

MCR 5.311(A), (C) |

Form Characteristics

| Fact Name | Description |

|---|---|

| Form Identification | The form is identified as PC 591 in the State of Michigan. |

| Approved by | This form is approved by the State Court Administrative Office (SCAO). |

| JIS Code | The Judicial Information System (JIS) code for this form is SST. |

| Purpose | It is used for the sworn statement to close unsupervised administration of an estate. |

| Requirement for Use | The personal representative uses this form to close the estate without a hearing, indicating that the estate has been fully administered. |

| Notice to Creditors | The form requires confirmation that, if necessary, a notice to creditors has been published and the claim period has expired. |

| Estate Administration Confirmation | The representative must confirm that estate debts, expenses, and taxes have been settled and assets have been distributed. |

| Tax Statements | The form includes statements regarding the status of Michigan estate or inheritance taxes. |

| Notification to Interested Parties | Distributees and claimants must be sent a copy of the sworn statement, ensuring transparency in the process. |

| Objection Process | Interested persons can object to the sworn statement by filing written objections with the probate court along with a filing fee. |

| Governing Laws | The governing laws for this form include MCL 700.3954, MCL 700.3958, and MCR 5.311(A), (C). |

Guidelines on Utilizing Pc 591 Michigan

Once the administration of an unsupervised estate has been fully managed in Michigan, filing the PC 591 form, known as the "Sworn Statement to Close Unsupervised Administration," is a critical final step. This form allows the personal representative to officially close the estate without needing a court hearing, spelling out that all debts, taxes, and distributions have been appropriately handled, and notifying the court and all interested parties that the estate's administration is complete. The procedure outlined below is designed to ensure that you can accurately complete and submit the form, helping to facilitate a smooth closure to the estate administration process.

- Start by entering the county where the estate is being administered at the top of the form.

- In the "Estate of" section, write the full name of the deceased, as recorded on the estate documents.

- Under section 1, affirm your role by stating, "I am the personal representative of this estate."

- Confirm the duration of your appointment and your actions concerning creditors by completing sections 2 and 3.

- Detail how the estate has been managed, indicating payments, settlements, distributions, and tax matters in sections 4 through 6. Remember to provide any required evidence, such as full payment confirmation from the Michigan Department of Treasury if inheritance or estate taxes were due.

- If there are any changes in the interested persons or their representatives from the initial application/petition, list these differences in the relevant section.

- In the section provided, write your name (personal representative), address, city, state, zip, and telephone number. Ensure that this information is typed or printed clearly.

- Sign the form in the designated area. Note that your signature must be sworn before a notary public. Fill in the date of signing.

- Below your signature, a notary public will fill in their part, including their commission expiry date and signature.

- If an attorney assisted in the preparation of this form, their signature, printed name, bar number, address, city, state, zip, and telephone number must be included in the respective section.

After completing and submitting the PC 591 form, the next steps involve waiting for any potential objections during the allotted 28-day period. If no objections are filed, a certificate indicating the completion of the estate administration may be issued. This certification is crucial as it helps protect the personal representative and the surety against future claims. Remember, the personal representative's appointment terminates automatically one year after the statement is filed, provided no action or proceeding involving them is pending in court. By following these steps accurately, you ensure compliance with Michigan's legal requirements for closing an unsupervised estate, thereby minimizing the risk of complications or delays in finalizing the estate's matters.

Crucial Points on This Form

What is the purpose of the PC 591 Michigan form?

The PC 591 form, also known as "Sworn Statement to Close Unsupervised Administration," serves a crucial purpose in the process of finalizing the administration of an estate in Michigan. It is used by the personal representative (often referred to as the executor or administrator) of an estate to officially declare that the responsibilities of administering the estate have been completed. This includes paying off any debts and taxes, distributing the assets to the rightful heirs, and completing any other necessary administrative tasks. By filing this form, the personal representative seeks to close the estate formally without the need for a hearing in probate court.

When should the PC 591 form be filed?

This form should be filed after more than five months have passed since the personal representative's original appointment. This timeframe allows the personal representative ample opportunity to identify estate assets, notify creditors, pay debts, and manage the estate's distribution according to the will or state law. It's essential to ensure that all tasks related to estate administration are completed before filing this form, as its submission indicates that the estate is ready to be closed.

What are the requirements for publishing notice to creditors?

According to Michigan law, a personal representative is typically required to publish a notice to creditors in a newspaper. This notice informs creditors of the estate administration so that they can present their claims within a specified period, generally within four months from the time the notice is published. This process ensures that the estate settles all outstanding debts before distribution to heirs. If this step is required by law or court rule, evidence of this notice and the expiration of the claim period must be provided with the PC 591 form.

What information is needed regarding estate taxes?

The personal representative must declare the status of any Michigan estate or inheritance taxes. Specifically, the representative must indicate whether:

- No Michigan estate or inheritance tax is due.

- The Michigan estate tax or inheritance tax has been paid in full, attaching evidence of full payment from the Michigan Department of Treasury if applicable.

This information ensures that the estate has met all tax obligations, which is a prerequisite for closing the estate.

How does the personal representative account for asset distribution and claims?

The personal representative must fully administer the estate by settling claims, paying expenses, and distributing the remaining assets to the entitled persons. Moreover, they need to:

- Identify any changes in interested persons or their representatives since the initial application or petition.

- Provide a written account of the estate's administration to those affected.

- Send a copy of the sworn statement to all distributees, unpaid or undischarged claimants, and any individuals who demanded notice.

This comprehensive accounting and notification process is designed to ensure transparency and fairness in the estate's closure.

What happens if someone objects to the sworn statement?

If an interested person disagrees with the sworn statement or the manner in which the estate has been administered, they may file written objections with the probate court. This must be done within 28 days after the sworn statement is filed, accompanied by a $20.00 filing fee. Failure to object within this timeframe may lead to the probate court issuing a certificate that endorses the estate's administration as complete. However, it is important to note that this certificate does not protect the personal representative or the estate's surety bond from future claims or legal actions.

Common mistakes

When completing the PC 591 Michigan form, a crucial requirement often overlooked is the accurate representation of personal details. This encompasses the personal representative's name, address, and contact information. Inconsistencies or errors in this section can lead to unnecessary delays or misunderstandings, making it pivotal to double-check these entries for accuracy.

Another common mistake involves the documentation of interested parties. The form necessitates a detailed account of all interested persons, their addresses, and any respective representatives. Changes from the initial application must be explicitly noted. Failing to update this information can lead to complications in the estate's closure, as it's imperative that all parties are correctly identified and informed throughout the process.

The requirement to publish a notice to creditors and the management of claims is another area prone to errors. The personal representative must affirm that if obligated by law or court rule, a notice to creditors was published and that the timeframe for claim presentation has expired. Plus, it's their responsibility to address all presented claims appropriately. Overlooking claims or mismanaging the publication requirement can result in legal repercussions or disputes against the estate.

A critical step in this form is to confirm the full administration of the estate, which includes settling claims, paying necessary taxes and expenses, and distributing the assets to entitled individuals. Errors in this section, such as distributing assets prematurely or inaccurately reporting the estate's administration, can lead to significant legal challenges or objections from interested parties or claimants.

Ensuring that a full account in writing was provided to distributees whose interests are affected is another area where mistakes can occur. This written account serves as a transparent record of the estate’s administration and asset distribution. Neglecting to provide this could raise suspicions or concerns among distributees, potentially leading to objections or legal scrutiny.

The verification of Michigan estate or inheritance taxes is also a common stumbling block. The form requires indicating whether these taxes are due and, if applicable, attaching evidence of their full payment from the Michigan Department of Treasury. Misunderstandings about tax obligations or failing to attach the required proof can cause delays in the estate's closure or additional financial liabilities.

Another error involves the assurance that copies of the sworn statement were sent to all necessary parties, including distributees, claimants with unresolved claims, and demandants. Skipping or inaccurately completing this step can lead to a lack of transparency and accountability, undermining the trust in the process established by the administration of the estate.

Finally, the failure to specify any exceptions regarding claims or arrangements made to address outstanding liabilities is another oversight. The form allows for the notation of exceptional circumstances, such as estates distributed subject to potential liabilities or detailed arrangements for outstanding claims. Missing these details can create ambiguity about the estate’s financial status and potentially expose distributees to unexpected liabilities.

Documents used along the form

When handling the closure of an unsupervised estate administration in Michigan, particularly with the PC 591 form, various other documents often accompany the process to ensure a thorough and compliant conclusion of the estate's affairs. These documents play critical roles in addressing different aspects of the estate's closure, from notifying creditors and inventorying assets to settling debts and distributing the remaining assets to the rightful heirs or beneficiaries. Here is an overview of some commonly used forms and documents alongside the PC 591 form:

- PC 574 - Notice to Creditors: This form is essential for notifying creditors of the estate's administration, providing them an opportunity to present any claims against the estate within a specified period. It helps in settling all claims before the estate is closed.

- PC 556 - Inventory: An inventory document lists all the assets belonging to the estate at the time of the decedent's death. This includes personal property, real estate, and any other assets. It serves as a record to ensure that all assets are accounted for in the estate distribution.

- PC 577 - Account of Fiduciary, Short Form: This form provides a summary of the financial transactions made by the estate's personal representative, including income received, expenses paid, and distributions to beneficiaries. It helps in tracking the administration of the estate's finances.

- PC 583 - Proof of Service: This document proves that all interested parties, including creditors, heirs, and legal representatives, have been properly notified about various proceedings and actions taken during the estate's administration, in compliance with legal requirements.

- PC 585 - Petition for Complete Estate Settlement: Though not always required, this form can be used when a personal representative seeks a formal court proceeding to approve the final settlement and distribution of the estate. It can help in resolving any disputes or objections by interested parties.

Utilizing these forms in conjunction with the PC 591 form ensures the personal representative adequately addresses all necessary procedures for closing the estate in compliance with Michigan law. It provides a structured approach to fulfilling duties, settling the estate's debts, distributing assets, and ultimately, closing the unsupervised administration through the probate court. Being thorough and using the correct forms can prevent complications and ensure that the estate is closed efficiently and without delay.

Similar forms

The Inventory Form (PC 577) in Michigan shares similarities with the PC 591 form in that both are utilized within the probate court process, involving the administration of an estate. While the PC 591 form is used for closing unsupervised administration after completing the estate's obligations, the Inventory Form is used earlier in the process to provide a detailed list of the estate's assets.

The Notice to Creditors (PC 574) resembles the PC 591 in its role within the estate administration process, specifically concerning creditors. The PC 591 form mentions the requirement of publishing notice to creditors and dealing with their claims, which directly relates to the purpose of the Notice to Creditors form, used to inform creditors of the estate's administration and to invite them to present their claims.

The Petition for Probate and/or Appointment of Personal Representative (PC 558) is similar to the PC 591 because both involve aspects of initiating and closing the probate court proceedings. While the PC 558 form is used at the beginning of the process to start probate and appoint a personal representative, the PC 591 signifies the completion of their duties and the closing of the estate.

Receipt of Distributee (PC 588) is comparable to the PC 591 form in that it also deals with the distribution phase of the estate administration. The PC 591 form includes a declaration of asset distribution to entitled persons, whereas the Receipt of Distributee form is a document that each recipient would sign to acknowledge receiving their portion of the estate.

The Statement to Close Estate (PC 592) is closely related to the PC 591 form as it also serves the purpose of closing an estate in probate court. While the PC 591 is used for closing unsupervised administration specifically, the PC 592 might be used in other contexts or specific estate closing situations, depending on the court's requirements.

The Declaration of Lasting Power of Attorney shares procedural elements with the PC 591, especially in terms of representing someone's interests. Although it's not limited to probate court and deals with broader legal authority, including health and financial decisions, both documents embody the representation and management of another's affairs.

The Application for Informal Probate and/or Appointment of Personal Representative (PC 558/PC 569), similar to the PC 591, encompasses actions taken to manage and finalize the affairs of an estate, but from the perspective of initiating the process rather than concluding it. Informal probate begins the unsupervised administration that PC 591 aims to close.

Order of Complete Estate Settlement (PC 593) parallels the PC 591 form by officially concluding aspects of the estate's administration. While PC 591 does so through a sworn statement by the personal representative, the Order of Complete Estate Settlement is a court order that may follow or include the actions stated in PC 591, providing judicial approval.

The Annual Return of Guardian on Condition of Legally Incapacitated Individual (PC 634), while not directly involved in probate estate administration, shares the concept of reporting and accountability to the court, similar to PC 591's requirement for the personal representative to report on the estate's closing.

Dos and Don'ts

Completing the PC 591 Michigan form, also known as the "Sworn Statement to Close Unsupervised Administration," is a legal procedure to conclude the duties of a personal representative in managing an estate without a court hearing. This process demands careful attention to detail. Below is a guide to assist you in accurately completing this form.

Do:

Ensure that more than five months have passed since your initial appointment as personal representative. This timeframe is mandatory before filing this sworn statement.

Verify that you have published a notice to creditors if required by law or court rule, and ensure the time allowed for presenting claims has expired.

Confirm that all estate debts, administration expenses, and taxes have been fully paid or settled.

Distribute the assets of the estate to the entitled individuals and note any deviations from the initial application in the form.

Send a copy of this sworn statement to all distributees, claimants with outstanding claims, and demandants as transparency is key.

Don't:

Dismiss the importance of providing accurate and current information regarding the interested parties and their representatives, including any changes since the initial application.

Forget to attach evidence of full payment if Michigan estate or inheritance tax was due.

Overlook the necessity to provide a detailed written account of the administration to distributees whose interests are impacted.

Fail to sign the document in front of a notary to validate the sworn statement officially. This is a critical step in the process.

Misconceptions

Understanding the PC 591 form in Michigan, which is a Sworn Statement to Close Unsupervised Administration, involves navigating through common misconceptions. While it aims to simplify the estate closure process, it's often misunderstood. Here are eight misconceptions explained:

- Anyone can file the PC 591 form: Only the appointed personal representative of the estate has the authority to file this document. It is their responsibility to ensure the estate is fully administered before filing.

- Filing automatically closes the estate: While filing the PC 591 does signal the intention to close the estate, it is not the final step. The estate is officially closed once the court issues a certificate of completion, assuming no objections are filed.

- All estates require a hearing to close: This form specifically allows for the closure of an estate without a hearing, provided all conditions are met, including the completion of estate administration tasks.

- No creditor notification is needed: The personal representative must have published notice to creditors, according to the law or court rule, and the time for presenting claims must have expired.

- Taxes are not a concern for the PC 591: The form requires either a declaration that no Michigan estate or inheritance taxes are due or evidence that any owed taxes have been paid in full.

- Assets can be distributed before filing the PC 591: The assets of the estate must be fully administered, including paying off debts and distributing assets, before the filing.

- A copy of the sworn statement doesn't need to be shared: The personal representative is required to send a copy of this sworn statement to all distributees, claimants with unresolved claims, and to all demandants to ensure transparency.

- The filing fee is negotiable or can be waived: If interested persons object to the sworn statement, they must file written objections accompanied by a $20.00 filing fee. This fee is set by the court and is not negotiable or waivable by the personal representative.

Understanding these misconceptions is crucial for personal representatives. This knowledge ensures the estate is closed correctly and reduces the risk of complications. Navigating the probate process smoothly requires a clear understanding of these requirements and obligations.

Key takeaways

Filling out and using the PC 591 Michigan form, formally known as the Sworn Statement to Close Unsupervised Administration, is a crucial step in wrapping up the probate process for an estate in an unsupervised setting. Here are four key takeaways to consider:

- Timeliness is key: More than five months must have elapsed since the original appointment of the personal representative before this sworn statement can be filed with the court. This timeline ensures that enough time has passed to address the estate's needs comprehensively.

- Notice to creditors: The personal representative must ensure that if it is required by law or court rule, a notice to creditors has been published, and the timeframe for the presentation of claims has expired. This process is essential for protecting the estate against late claims and ensuring that all creditors have been fairly addressed.

- Full administration and distribution are completed: Before filing the form, the personal representative needs to have fully administered the estate. This includes paying or settling claims, covering estate and administration expenses, paying taxes, and distributing the estate's assets to the rightful parties. Documentation or evidence of tax payments, particularly regarding Michigan estate or inheritance tax, may need to be attached.

- Communication with interested parties: The personal representative is responsible for sending a copy of this sworn statement to all distributees, claimants with unsettled claims, and to all demandants. Moreover, providing a full written account of the administration to distributees who are affected shows transparency and ensures all parties are informed. It’s a vital step for concluding the unsupervised administration process smoothly.

Last but not least, it is important to remember that interested persons have the right to object to the sworn statement by filing written objections with the probate court, accompanied by a filing fee. The statement itself does not protect the personal representative from potential actions against them or the estate's bond, emphasizing the importance of thorough and careful estate administration. Utilizing the PC 591 form accurately and effectively signifies the successful closure of the estate under Michigan law, bringing peace of mind to the personal representative and all parties involved.

Popular PDF Templates

What Reasons Can You Quit a Job and Still Get Unemployment Michigan - Interest paid on debt from railway operations and net operating income are also reported to give a comprehensive financial snapshot.

State of Michigan 2022 Tax Forms - To change your current power of attorney details with the Michigan Department of Treasury, fill out and submit form 151 accordingly.

Michigan Land Contract Form - A straightforward way to memorialize the specifics of a property transaction under a land contract.