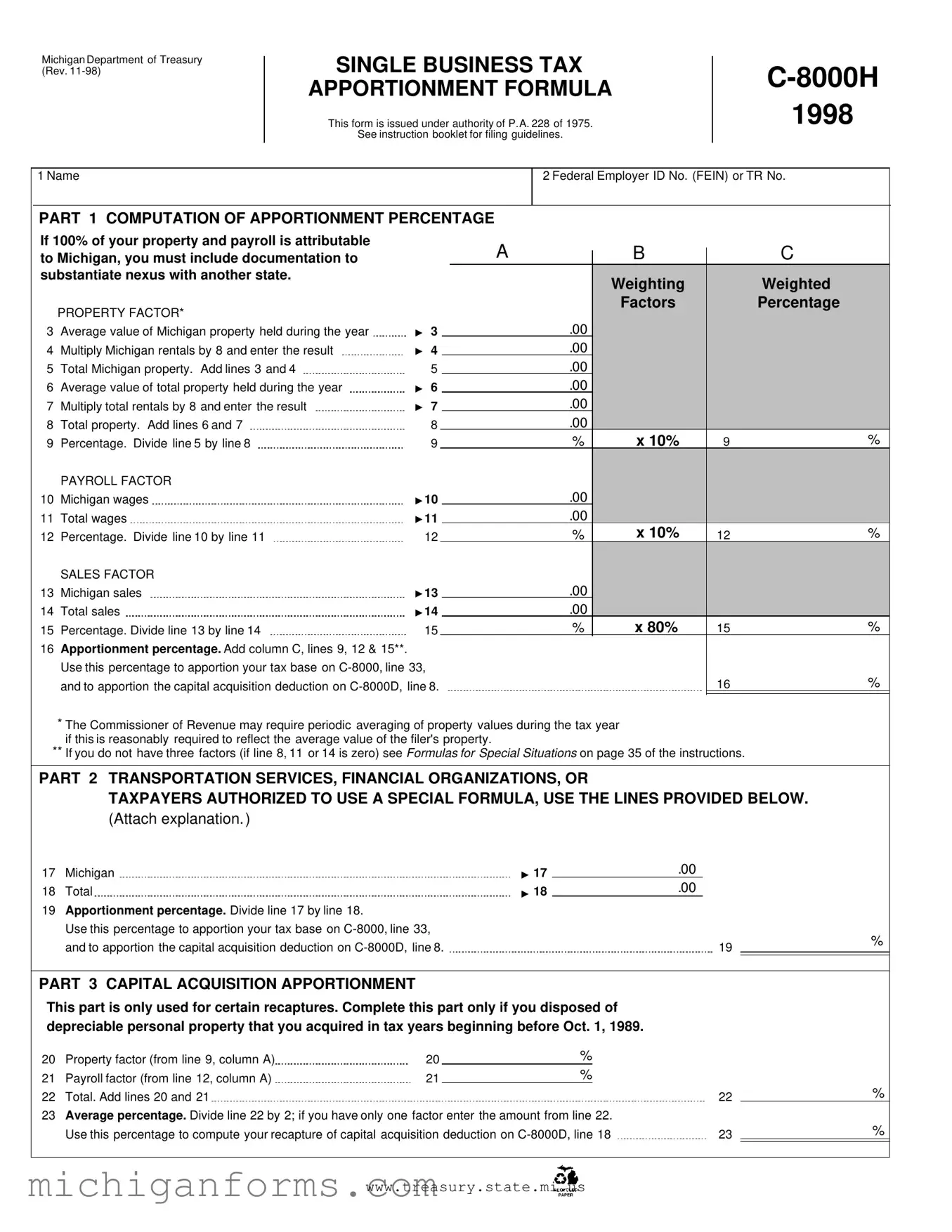

Michigan C 8000H PDF Form

Navigating the complexities of state taxation forms is crucial for businesses seeking compliance and favorable tax treatment. Among these, the Michigan Department of Treasury's C 8000H form plays a pivotal role for businesses operating within the state. Issued under the authority of P.A. 228 of 1975, this Single Business Tax Apportionment Formula is designed to guide businesses in accurately calculating their tax obligations based on property, payroll, and sales within Michigan as well as other states. This detailed form not only asks for basic information such as the business name and Federal Employer Identification Number (FEIN) but also delves into the intricacies of calculating an apportionment percentage—a figure essential for determining the portion of total business activity subject to Michigan taxes. Critical sections of the form include computations for the value of property held, payroll expenses, and sales made within Michigan, offering a framework for a weighted average that reflects a business's operational footprint. Furthermore, special considerations and formulas are provided for businesses involved in transportation services, financial organizations, or those eligible to use a unique formula, ensuring a tailored approach to various business models. Notably, the form also addresses the capital acquisition apportionment for older investments, reminding filers of the ongoing impacts of past transactions on current tax liabilities.

Preview - Michigan C 8000H Form

Michigan Department of Treasury (Rev.

SINGLE BUSINESS TAX APPORTIONMENT FORMULA

This form is issued under authority of P.A. 228 of 1975.

See instruction booklet for filing guidelines.

1998

1 Name

2 Federal Employer ID No. (FEIN) or TR No.

PART 1 COMPUTATION OF APPORTIONMENT PERCENTAGE

If 100% of your property and payroll is attributable |

|

|

|

|

A |

|

B |

|

C |

|

to Michigan, you must include documentation to |

|

|

|

|

|

|

||||

substantiate nexus with another state. |

|

|

|

|

|

|

Weighting |

|

Weighted |

|

|

|

|

|

|

|

|

|

|

||

|

PROPERTY FACTOR* |

|

|

|

|

|

|

Factors |

|

Percentage |

|

|

|

|

|

|

|

|

|

|

|

3 |

Average value of Michigan property held during the year |

▼ |

3 |

|

|

|

.00 |

|

|

|

4 |

Multiply Michigan rentals by 8 and enter the result |

▼ |

4 |

|

|

|

.00 |

|

|

|

5 |

Total Michigan property. Add lines 3 and 4 |

|

5 |

|

|

|

.00 |

|

|

|

6 |

Average value of total property held during the year |

▼ |

6 |

|

|

|

.00 |

|

|

|

7 |

Multiply total rentals by 8 and enter the result |

▼ |

7 |

|

|

|

.00 |

|

|

|

8 |

Total property. Add lines 6 and 7 |

|

8 |

|

|

|

.00 |

|

|

|

9 |

Percentage. Divide line 5 by line 8 |

|

9 |

|

|

|

% |

x 10% |

9 |

% |

|

PAYROLL FACTOR |

|

|

|

|

|

|

|

|

|

10 |

Michigan wages |

▼ |

10 |

|

|

|

.00 |

|

|

|

11 |

Total wages |

▼ |

11 |

|

|

|

.00 |

|

|

|

12 |

Percentage. Divide line 10 by line 11 |

|

12 |

|

|

|

% |

x 10% |

12 |

% |

|

SALES FACTOR |

|

|

|

|

|

|

|

|

|

13 |

Michigan sales |

▼ |

13 |

|

|

|

.00 |

|

|

|

14 |

Total sales |

▼ |

14 |

|

|

|

.00 |

|

|

|

15 |

Percentage. Divide line 13 by line 14 |

|

15 |

|

|

|

% |

x 80% |

15 |

% |

16 |

Apportionment percentage. Add column C, lines 9, 12 & 15**. |

|

|

|

|

|

|

|

|

|

|

Use this percentage to apportion your tax base on |

|

|

|

|

|||||

|

and to apportion the capital acquisition deduction on |

|

|

16 |

% |

|||||

|

|

|

|

|

|

|

|

|

|

|

*The Commissioner of Revenue may require periodic averaging of property values during the tax year if this is reasonably required to reflect the average value of the filer's property.

**If you do not have three factors (if line 8, 11 or 14 is zero) see Formulas for Special Situations on page 35 of the instructions.

PART 2 TRANSPORTATION SERVICES, FINANCIAL ORGANIZATIONS, OR

TAXPAYERS AUTHORIZED TO USE A SPECIAL FORMULA, USE THE LINES PROVIDED BELOW.

(Attach explanation. )

17 Michigan

▼

17

.00

18Total

19Apportionment percentage. Divide line 17 by line 18.

Use this percentage to apportion your tax base on

▼

18

.00

19 |

% |

|

PART 3 CAPITAL ACQUISITION APPORTIONMENT

This part is only used for certain recaptures. Complete this part only if you disposed of depreciable personal property that you acquired in tax years beginning before Oct. 1, 1989.

20 |

Property factor (from line 9, column A) |

20 |

% |

|

|

|

21 |

Payroll factor (from line 12, column A) |

21 |

% |

|

|

|

22 |

Total. Add lines 20 and 21 |

|

|

|

22 |

% |

23 |

Average percentage. Divide line 22 by 2; if you have only one factor enter the amount from line 22. |

|

|

|||

|

Use this percentage to compute your recapture of capital acquisition deduction on |

23 |

% |

|||

www.treasury.state.mi.us

Form Characteristics

| Fact Name | Description |

|---|---|

| Issuing Authority | Michigan Department of Treasury |

| Revision Date | November 1998 |

| Form Purpose | SINGLE BUSINESS TAX APPORTIONMENT FORMULA |

| Legal Basis | Authority of P.A. 228 of 1975 |

| Instruction Availability | Instruction booklet available for filing guidelines |

| Nexus Documentation Requirement | Documentation required if 100% of property & payroll attributable to Michigan to substantiate nexus with another state |

Guidelines on Utilizing Michigan C 8000H

Filling out the Michigan Department of Treasury Single Business Tax Apportionment Formula, known as form C-8000H, requires careful attention to detail. This document is designed to calculate the apportionment percentage for tax obligations based on property, payroll, and sales in Michigan versus total amounts. It's critical for businesses that have a physical presence or economic nexus within the state and elsewhere. By following the prescribed steps, taxpayers can ensure accurate computation and compliance with state tax regulations.

- Start by entering your business name in the field designated as "1 Name".

- Input your Federal Employer Identification Number (FEIN) or TR Number in the space labeled "2 Federal Employer ID No. (FEIN) or TR No."

- Under the section titled "PART 1 COMPUTATION OF APPORTIONMENT PERCENTAGE", calculate the average value of Michigan property held throughout the year and fill this amount in at "3".

- Multiply your Michigan rentals by 8 and enter this result in the field marked "4".

- Add the amounts from lines 3 and 4, and place the total in line "5".

- Determine the average value of all property held during the year and record this figure at "6".

- Similar to step 4, multiply your total rentals by 8 and record this number at "7".

- Sum the figures in lines 6 and 7, and write the total in line "8".

- To find the property factor percentage, divide the number in line 5 by the number in line 8 and enter the result in line "9", then multiply this figure by 10%.

- For the payroll factor, report Michigan wages at line "10" and total wages at line "11".

- Divide line 10 by line 11, and input the resulting percentage at line "12", subsequently multiplying this figure by 10%.

- Enter Michigan sales in line "13" and total sales in line "14".

- To calculate the sales factor percentage, divide line 13 by line 14, record the percentage in line "15", and then multiply by 80%.

- Add the weighted factors from column C, lines 9, 12, and 15 to find the apportionment percentage. Enter this total percentage in line "16".

- If applicable, transportation services, financial organizations, or those authorized to use a special formula should report Michigan figures in line "17" and total figures in line "18", then calculate the apportionment percentage and fill in line "19".

- Part 3 is for the recapture of capital acquisition deduction. Report the property factor from line 9, column A at "20".

- Enter the payroll factor from line 12, column A in line "21".

- Add lines 20 and 21 for the total, recording this in line "22".

- Average the percentage from line 22 by dividing by 2, or enter the line 22 amount if only one factor is present, and report this in line "23".

After completing the form, review your entries for accuracy and ensure that any required documentation is included, especially if 100% of your property and payroll is attributable to Michigan but nexus with another state must be substantiated. Compliance with Michigan's tax laws hinges on the precision and veracity of the information provided on the C-8000H form.

Crucial Points on This Form

What is the purpose of the Michigan C 8000H form?

The Michigan C 8000H form is a crucial document for businesses operating within the state of Michigan. Its primary role is to calculate the apportionment percentage for the Single Business Tax (SBT). This percentage determines how much of a business's tax base is subject to Michigan's taxes, based on the proportion of their business activities (property, payroll, and sales) that occur within the state. It is designed to ensure that businesses pay taxes fairly, relative to their operations in Michigan versus other states.

How does a business complete the Apportionment Percentage computation on the form?

To complete the Apportionment Percentage section, a business should follow these steps:

- Calculate the average value of Michigan property held during the year and enter this on line 3. Multiply Michigan rentals by 8 and add this to line 4, then sum these figures on line 5.

- Perform a similar calculation for total property (both within and outside of Michigan) and enter this on line 8.

- Divide the Michigan property total by the overall property total to find the Property Factor percentage, and enter this on line 9.

- Calculate the Payroll and Sales factors by dividing Michigan wages and sales by the total wages and sales, entering these percentages on lines 12 and 15, respectively.

- Add the weighted percentages from lines 9, 12, and 15 to find the overall apportionment percentage, which is used to determine the portion of business income subject to Michigan tax.

This process ensures that the tax burden is allocated based on where the company’s business activities are conducted.

What if a business does not have all three factors for the Apportionment Percentage?

If a business does not have all three factors (Property, Payroll, and Sales), the Michigan Department of Treasury provides alternative formulas for special situations, as referenced on page 35 of the instruction booklet. In such cases, a business might only have one or two of the factors due to the nature of its operations. Depending on the particular situation, the business may be authorized to use a special formula that best reflects its activity pattern. For instance, a company with no physical presence in Michigan but with sales to Michigan customers might only utilize the Sales Factor. This flexibility ensures that the apportionment calculation fairly represents the business's involvement in the state.

Can transportation services, financial organizations, or other special entities use a different formula?

Yes, certain entities such as transportation services, financial organizations, or taxpayers authorized to use a special formula have dedicated lines (17-19) in Part 2 of the form for this purpose. These entities often have unique operational structures or regulatory considerations that necessitate a different approach to calculating their apportionment percentage. They must attach an explanation of why the standard formula is not applicable and detail the special formula used. This accommodates the diverse range of business operations in Michigan and ensures that each is taxed in a manner that reflects its actual economic presence in the state.

Common mistakes

Filling out the Michigan C 8000H form, a crucial document for calculating the Single Business Tax apportionment formula, requires attention to detail and an understanding of your business activities within and outside Michigan. Common mistakes can lead to errors that may affect your tax liabilities. It is essential to take these errors into account to ensure accurate reporting and compliance with the Michigan Department of Treasury requirements.

One prevalent mistake is not providing documentation to support the nexus with another state when 100% of property and payroll are attributable to Michigan. This oversight can question the legitimacy of your apportionment claims and potentially delay the processing of your form. Ensuring all necessary documentation is attached is key to substantiating your business activities across state lines.

Another common error is inaccurately calculating the average value of Michigan property held during the year. This calculation forms the basis of the property factor and requires careful consideration of all property values throughout the tax period. Misinterpretations of what constitutes 'property' or miscalculations in determining the average can skew the results significantly.

Similarly, improperly multiplying Michigan rentals by 8 as instructed in the form can distort the total Michigan property value. This step is crucial for businesses that lease property, as it impacts the property factor's outcome. Overlooking or misunderstanding this multiplication can lead to underestimating or overestimating the property factor.

Incorrectly totaling the Michigan property by failing to add lines 3 and 4 accurately is another mistake that can impact the apportionment percentage. This simple arithmetic error can result in reporting a skewed property factor, which in turn, affects the overall apportionment calculation.

Miscalculating the payroll and sales factors by not properly dividing Michigan wages and sales by the total wages and sales respectively is a frequent error. These factors influence the apportionment calculation significantly, and inaccuracies here can lead to incorrect tax obligations.

Not adjusting the apportionment percentage by adding the weighted factors correctly in the computation of the apportionment percentage can cause issues with the tax base reported on the C-8000 form. This summation step is crucial for determining the correct tax liability.

For businesses that are part of special categories, such as transportation services or financial organizations, failing to use the lines provided for special formulas or not attaching an explanation of the formula used can be a critical oversight. The state requires specific information for these entities, and omitting this information can lead to incorrect apportionment calculations.

Finally, a common mistake is not completing Part 3 for capital acquisition apportionment when applicable. This section is essential for businesses that disposed of depreciable personal property acquired before October 1, 1989. Neglecting this part can lead to errors in recapturing the capital acquisition deduction, impacting the overall tax calculation.

Avoiding these mistakes requires a thorough review of the instructions provided by the Michigan Department of Treasury and a precise application of the guidelines. Accurate completion of the Michigan C 8000H form is vital for proper tax reporting and compliance.

Documents used along the form

When businesses in Michigan navigate the complexities of taxes, the Michigan Department of Treasury’s C-8000H form, a crucial document for computing the Single Business Tax Apportionment Formula, often comes into play. Along with this essential form, there are several other important documents and forms that businesses might need to accurately fulfill their tax obligations and ensure compliance with state regulations.

- C-8000: This is the primary Single Business Tax Return form. Businesses use it to calculate and report their total tax liability. It serves as the core document where the apportionment percentage calculated on the C-8000H form is applied to determine the tax base.

- C-8000D: Capital Acquisition Deduction Schedule. This particular document is utilized to apportion the capital acquisition deduction. The apportionment percentage computed in the C-8000H form, specifically for capital acquisitions, is essential for accurately completing this schedule.

- Form 4567: Business Tax Annual Return. Although focusing on different aspects of business taxation, Form 4567 is often submitted alongside the C-8000 series by companies operating within Michigan. It covers a broader spectrum of business tax liabilities beyond the Single Business Tax, offering a comprehensive view of a business’s annual tax responsibilities.

- Form 4891: Michigan Corporate Income Tax Annual Return. This document is required for corporations to report their income tax. For corporations that also need to complete the C-8000H, both forms work in tandem to ensure that all pertinent information regarding the business's earnings and apportionments are correctly reported to the Michigan Department of Treasury.

Together, these documents form a cohesive framework for businesses to report various aspects of their finances and operations to the Michigan Department of Treasury. Accurate completion and submission of these forms are paramount for businesses to remain compliant, optimize their tax obligations, and avoid potential penalties. The interconnection between these forms underscores the importance of a thorough understanding of each document’s requirements and implications for Michigan’s tax landscape.

Similar forms

The Michigan C 8000H form is a detailed document tailored to help businesses compute their tax apportionment percentage in the state. It takes into account various factors such as property, payroll, and sales to determine the appropriate tax obligations. There are several other forms that, while serving different purposes, share similarities in structure or function with the Michigan C 8000H form. Here are five such documents:

- IRS Form 1120: The U.S. Corporation Income Tax Return, known as Form 1120, is used by corporations to report their income, gains, losses, deductions, and credits to the Internal Revenue Service. Like the Michigan C 8000H, it requires detailed financial information to calculate the owed taxes, although on a federal level. Both forms take into account the apportionment of income based on various operational factors.

- Form 1065: This is the Return of Partnership Income form used by partnerships for tax reporting. Similar to the C 8000H, Form 1065 requires detailed apportionment of income, deductions, and credits amongst partners. Both documents are necessary for accurate tax obligations calculations based on the entity’s operational statistics.

- Form Schedules K-1: Issued in conjunction with Form 1065, the Schedules K-1 document outlines an individual partner’s share of a partnership's earnings, deductions, and credits. It parallels the C 8000H in its aim to distinctly allocate portions of income or deductions based on ownership or entitlement principles.

- California Form 568: This form is the Limited Liability Company Return of Income in California, which, akin to the Michigan C 8000H, involves allocating income across various factors for state tax purposes. Both forms are designed for specific entity structures and require detailed financial calculations to comply with state tax laws.

- New York CT-3: The General Business Corporation Franchise Tax Return, or CT-3, is a form used by corporations in New York State. While serving a similar purpose to the Michigan C 8000H in determining tax obligations, it focuses on New York businesses and includes calculations for apportionment based on property, payroll, and sales, much like its Michigan counterpart.

Each of these documents, while tailored to different entities or jurisdictions, shares the common goal of ensuring businesses accurately report and apportion their income for tax purposes, underscoring the importance of proper financial documentation in the compliance landscape.

Dos and Don'ts

When completing the Michigan C 8000H form, there are several important guidelines to follow to ensure the process is done accurately and in compliance with state regulations. Below are lists of things you should and shouldn't do.

Things you should do:

- Review the instruction booklet before filling out the form to understand all requirements and guidelines.

- Ensure that all information is accurate and complete, especially the name and Federal Employer ID No. (FEIN) or TR No.

- Include documentation if 100% of your property and payroll is attributable to Michigan but you have nexus with another state.

- Accurately calculate the apportionment percentage, using the formulas provided for property, payroll, and sales factors.

- If applicable, complete Part 2 for transportation services, financial organizations, or if authorized to use a special formula, and attach any required explanations.

- For disposals of depreciable personal property acquired before Oct. 1, 1989, make sure to fill out Part 3 for capital acquisition apportionment.

Things you shouldn't do:

- Avoid guessing on figures or making estimations without proper basis or documentation.

- Do not leave any required fields incomplete. If a section does not apply, make sure to denote that it is not applicable in a manner consistent with form instructions.

- Avoid ignoring the special instructions on page 35 regarding formulas for special situations if you do not have three factors.

- Do not miscalculate the weighting factors or percentages; double-check all math.

- Refrain from submitting outdated information or using data from the wrong tax year.

- Do not forget to attach any required explanations for Parts 2 and 3, if these sections are applicable to your situation.

Misconceptions

When navigating the intricacies of the Michigan Department of Treasury's C-8000H form, several misconceptions can lead to confusion and potential errors in tax reporting. Below are some common misunderstandings and the facts to set them straight.

- Misconception #1: The form is optional for businesses operating in Michigan.

Fact: The C-8000H form is mandatory for businesses that need to apportion their tax base due to operations in multiple states, ensuring the correct tax amount is calculated for Michigan.

- Misconception #2: All sections of the form must be completed by all filers.

Fact: Certain sections of the C-8000H form are only applicable to specific business scenarios, such as those offering transportation services or financial organizations. Most businesses will not use every section.

- Misconception #3: The form does not require detailed documentation.

Fact: Adequate documentation is crucial, especially if 100% of property and payroll are attributed to Michigan but the business has nexus with another state, to substantiate the apportionment calculation.

- Misconception #4: Sales outside of Michigan do not affect the form.

Fact: Sales outside of Michigan play a critical role in the sales factor of the apportionment percentage, significantly impacting the overall tax liability to the state.

- Misconception #5: The form applies the same factors for all businesses.

Fact: The weighting of property, payroll, and sales factors can vary significantly between businesses, especially with the Commissioner of Revenue's authority to require different averaging methods for property values.

- Misconception #6: The capital acquisition deduction is straightforward to calculate.

Fact: The calculation for the capital acquisition deduction can be complex, requiring careful apportionment, especially for property acquired before October 1, 1989, and later disposed of.

- Misconception #7: The apportionment percentage relies solely on in-state activities.

Fact: The apportionment percentage considers both in-state and out-of-state activities to accurately reflect the business's operations and applicable tax obligations.

- Misconception #8: Only tangible property counts towards the property factor.

Fact: Both tangible property (like real estate and physical assets) and certain intangible properties, like rentals multiplied by eight, contribute to the property factor's calculation.

- Misconception #9: Any discrepancy in the form is easily corrected after filing.

Fact: Discrepancies or errors in the C-8000H form can lead to audits, potential fines, and a lengthy correction process, emphasizing the need for accuracy and thoroughness in the initial filing.

Understanding these nuances is critical for businesses to comply with Michigan's tax requirements accurately. Misinterpretations can lead to mistakes in tax filings, possibly resulting in avoidable penalties and interest on owed taxes.

Key takeaways

When filling out and using the Michigan C 8000H form, it's important to understand several key points to ensure accurate completion and compliance with relevant state tax laws. Below are six takeaways that can help guide you through this process:

- Form Purpose: The Michigan C 8000H form is designed for the apportionment of the Single Business Tax. Appropriate use of this form is necessary for businesses operating both within and outside Michigan to calculate their tax obligations based on property, payroll, and sales factors.

- Documentation Requirements: If 100% of a business's property and payroll are attributable to Michigan, documentation to substantiate a nexus with another state must be included. This is crucial for businesses that may be primarily based in Michigan but have operations or sales outside the state.

- Apportionment Percentage Calculation: The form requires the computation of an apportionment percentage based on property, payroll, and sales factors within Michigan compared to total figures. These percentages are then weighted and summed to determine the overall apportionment percentage for tax purposes.

- Special Formulas and Exceptions: For transportation services, financial organizations, or taxpayers authorized to use a special formula, dedicated lines are provided in Part 2 of the form. An attached explanation for applying a special formula is necessary for these cases.

- Capital Acquisition Apportionment: Part 3 of the form deals with the apportionment of certain recaptures related to the disposal of depreciable personal property acquired before October 1, 1989. This section is only applicable under specific circumstances, highlighting the importance of understanding the nuances of one's tax liabilities.

- Comprehensive Instructions: The form mentions an instruction booklet that provides filing guidelines, indicating that there are detailed instructions available. It’s advisable for taxpayers to review this booklet carefully to ensure compliance and accuracy when completing and submitting the form.

Understanding these key aspects of the Michigan C 8000H form can significantly assist businesses in the accurate reporting and apportionment of their tax obligations to the Michigan Department of Treasury, fostering compliance and potentially optimizing tax liabilities.

Popular PDF Templates

State of Michigan Tax Forms - Mi 5081 allows businesses to claim various exemptions and deductions, like resale and agricultural production.

State of Michigan Forms - Directions on the procedural aspect of submitting the application form, highlighting the importance of including all requested details and fees.