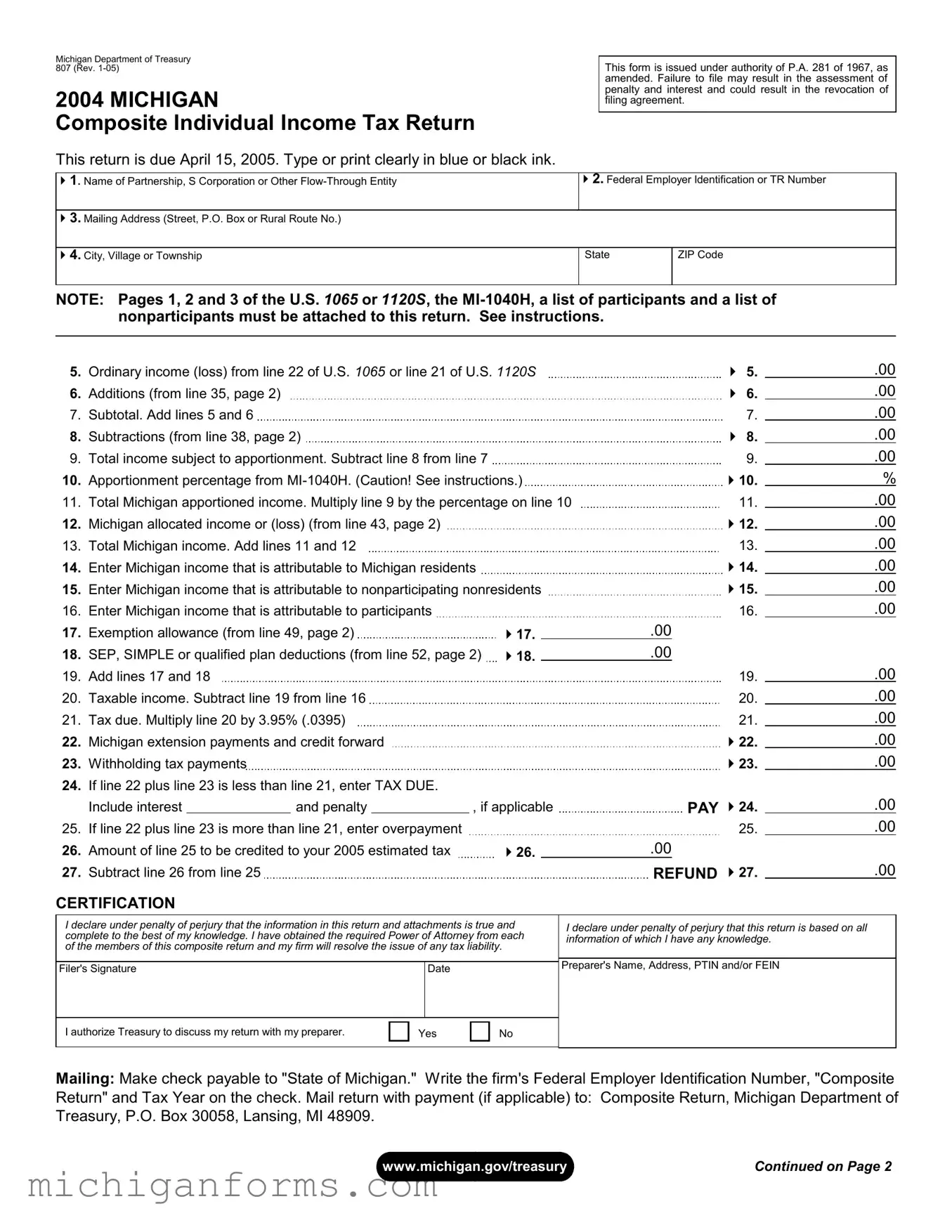

Michigan 807 PDF Form

When dealing with the intricacies of tax obligations for partnerships, S corporations, and other flow-through entities in Michigan, the Michigan Department of Treasury 807 form comes into play as a critical document. This form, designated for the 2004 tax year and due by April 15, 2005, is a composite individual income tax return designed under the authority of P.A. 281 of 1967, as amended. It's vital for these entities to file this form accurately and punctually to avoid penalties, interest, and potential revocation of their filing agreement. The form requires detailed information about the entity, including its name, federal employer identification or TR number, and mailing address. Additionally, it mandates the attachment of U.S. 1065 or 1120S forms, the MI-1040H, and lists of both participants and nonparticipants to provide a comprehensive overview of the entity's income and apportionment. The form serves as a declaration of income, losses, and tax dues, inclusive of specifics on additions, subtractions, allocated income, exemption allowances, and deductions relating to SEP, SIMPLE, or qualified plans. Entities must navigate through sections detailing income adjustments, apportionment calculations, and ultimately tax liabilities or overpayments, ensuring a meticulous approach to fulfill their tax responsibilities while adhering to Michigan's legal requirements.

Preview - Michigan 807 Form

Michigan Department of Treasury 807 (Rev.

2004 MICHIGAN

Composite Individual Income Tax Return

This return is due April 15, 2005. Type or print clearly in blue or black ink.

This form is issued under authority of P.A. 281 of 1967, as amended. Failure to file may result in the assessment of penalty and interest and could result in the revocation of filing agreement.

1. Name of Partnership, S Corporation or Other |

2. Federal Employer Identification or TR Number |

|

|

|

|

3. Mailing Address (Street, P.O. Box or Rural Route No.) |

|

|

|

|

|

4. City, Village or Township |

State |

ZIP Code |

|

|

|

NOTE: Pages 1, 2 and 3 of the U.S. 1065 or 1120S, the

5. |

Ordinary income (loss) from line 22 of U.S. 1065 or line 21 of U.S. 1120S |

|

5. |

.00 |

||

6. |

Additions (from line 35, page 2) |

|

|

|

6. |

.00 |

7. |

Subtotal. Add lines 5 and 6 |

|

|

7. |

.00 |

|

8. |

Subtractions (from line 38, page 2) |

|

|

|

8. |

.00 |

9. |

Total income subject to apportionment. Subtract line 8 from line 7 |

|

|

9. |

.00 |

|

10. |

Apportionment percentage from |

|

10. |

% |

||

11. |

Total Michigan apportioned income. Multiply line 9 by the percentage on line 10 |

11. |

.00 |

|||

12. |

Michigan allocated income or (loss) (from line 43, page 2) |

|

|

|

12. |

.00 |

13. |

Total Michigan income. Add lines 11 and 12 |

|

|

13. |

.00 |

|

14. |

Enter Michigan income that is attributable to Michigan residents |

|

|

|

14. |

.00 |

15. |

Enter Michigan income that is attributable to nonparticipating nonresidents |

|

15. |

.00 |

||

16. |

Enter Michigan income that is attributable to participants |

|

|

16. |

.00 |

|

17. |

Exemption allowance (from line 49, page 2) |

17. |

|

.00 |

|

|

18. |

SEP, SIMPLE or qualified plan deductions (from line 52, page 2) |

18. |

|

.00 |

|

|

|

19. |

.00 |

||||

19. |

Add lines 17 and 18 |

|

|

|||

20. |

Taxable income. Subtract line 19 from line 16 |

|

|

20. |

.00 |

|

21. |

Tax due. Multiply line 20 by 3.95% (.0395) |

|

|

21. |

.00 |

|

22. |

Michigan extension payments and credit forward |

|

|

|

22. |

.00 |

23. |

Withholding tax payments |

|

|

|

23. |

.00 |

24.If line 22 plus line 23 is less than line 21, enter TAX DUE.

|

Include interest |

|

and penalty |

|

, if applicable |

|

PAY 24. |

.00 |

|

|

|

|

|

.00 |

|||||

25. |

If line 22 plus line 23 is more than line 21, enter overpayment |

|

|

25. |

|||||

26. |

Amount of line 25 to be credited to your 2005 estimated tax |

26. |

|

.00 |

|

|

|||

27. |

Subtract line 26 from line 25 |

|

|

|

|

REFUND 27. |

.00 |

||

|

|

|

|

|

|||||

CERTIFICATION

I declare under penalty of perjury that the information in this return and attachments is true and |

I declare under penalty of perjury that this return is based on all |

||||||

complete to the best of my knowledge. I have obtained the required Power of Attorney from each |

|||||||

information of which I have any knowledge. |

|||||||

of the members of this composite return and my firm will resolve the issue of any tax liability. |

|||||||

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preparer's Name, Address, PTIN and/or FEIN |

|

Filer's Signature |

|

|

Date |

|

|

||

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

I authorize Treasury to discuss my return with my preparer. |

|

Yes |

|

No |

|

||

|

|

|

|||||

|

|

|

|

|

|

|

|

Mailing: Make check payable to "State of Michigan." Write the firm's Federal Employer Identification Number, "Composite

Return" and Tax Year on the check. Mail return with payment (if applicable) to: Composite Return, Michigan Department of Treasury, P.O. Box 30058, Lansing, MI 48909.

www.michigan.gov/treasury |

Continued on Page 2 |

2004 807, Page 2

Name of Partnership, S Corporation or Other Flow Through Entity |

Federal Employer Identification or TR Number |

|

|

|

ADDITIONS (see instructions) |

|

28. |

Net income (loss) from rental real estate activities |

28. |

29. |

Net income (loss) from other rental activities |

29. |

30. |

Portfolio Income (loss) (see instructions): |

|

|

a. Interest income |

30a. |

|

b. Dividend income |

30b. |

|

c. Royalty income |

30c. |

|

d. Net |

30d. |

|

e. Net |

30e. |

|

f. Other portfolio income |

30f. |

31. |

Net gain (loss) under Section 1231 |

31. |

32. |

Other income from U.S. Schedule K |

32. |

33. |

State or local taxes measured by income |

33. |

34. |

Other miscellaneous additions (attach schedule) |

34. |

35. |

Total additions. Add lines 28 through 34. Enter here and on line 6 |

35. |

|

SUBTRACTIONS (see instructions) |

|

36. |

Income (loss) from other partnerships, S corp. and fiduciaries included in ordinary income |

36. |

37. |

Other miscellaneous subtractions (attach schedule) |

37. |

38. |

Total subtractions. Add lines 36 and 37. Enter here and on line 8 |

38. |

|

MICHIGAN ALLOCATED INCOME OR (LOSS) |

|

39. |

Guaranteed payments to participants for services performed in Michigan |

39. |

40. |

Income attributable to other Michigan partnerships, S corporations or fiduciaries |

40. |

41. |

Net Michigan capital gains (losses) (from U.S. Schedule D) |

41. |

42. |

Other Michigan allocated income (loss) (see instructions) |

42. |

43. |

Total Michigan allocated income (loss). |

|

|

Add lines 39 through 42. Enter here and on line 12 |

43. |

|

EXEMPTION ALLOWANCE |

|

44. |

Number of participants included in this agreement |

44. |

45. |

Line 44 times $3,100 exemption allowance |

45. |

46. |

Total Michigan income from line 13 |

46. |

47. |

Total distributive income (Total Distributive Income from Distributive Income Worksheet) |

47. |

48. |

Percent of income attributable to Michigan. Divide line 46 by line 47. |

|

|

(May not exceed 100%.) |

48. |

49. |

Apportioned exemption allowance. Multiply line 45 by the percentage on line 48 |

|

|

Enter here and on line 17 |

49. |

|

SEP, SIMPLE OR QUALIFIED PLAN SUBTRACTIONS |

|

50. |

SEP, SIMPLE or qualified plan subtractions for participants (attach schedule) |

50. |

51. |

Enter the percent of income attributable to Michigan from line 48 |

51. |

52. |

SEP, SIMPLE or qualified plan subtractions attributable to Michigan |

|

|

Multiply line 50 by the percentage on line 51. Enter here and on line 18 |

52. |

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

%

.00

.00

%

.00

2004 807, PAGE 3

Instructions for Form 807, Michigan Composite Individual Income Tax Return

GENERAL INSTRUCTIONS

Who may file a return

A

Participation Requirements

A member may not participate in this composite return in any of the following cases:

•If he or she is claiming a city income tax credit, public contribution credit, community foundation credit, homeless shelter/food bank credit, college tuition credit or Michigan Historic Preservation Tax Credit.

•If he or she was a Michigan resident

•If he or she wishes to claim more than one Michigan exemption.

Due date of return

The composite return for any tax periods ending in 2004 is due April 15, 2005. The returns for any periods ending in 2005 will be due April 15, 2006.

If the firm cannot file by the due date, a request for an extension can be filed before the original due date. See “Requesting an Extension” on this page.

Withholding tax payments

Composite filers are required to make withholding tax payments on behalf of

all nonresident members (both participating and nonparticipating). The payment of withholding is due quarterly on April 20, July 20, and October 20 of the taxable year and January 20 of the succeeding year. The payment of withholding taxes is remitted on the payment voucher Form 160, Combined Return for Michigan Taxes.

Requesting an extension

The firm may request an extension of time to file by sending payment of the estimated annual liability to Treasury with a copy of an approved federal extension. Any extension allowed by the

Internal Revenue Service for filing the firm’s federal return automatically extends the due date of the composite return to the same extended due date.

If the firm does not apply for a federal extension, request an Application for Extension of Time to File Michigan Tax Returns (Form 4). When completing the extension form, check “Fiduciary Tax” in box 1, use the firm’s name and federal employer identification number (FEIN) and write “composite return” on the form. Follow these special instructions to make sure your account is credited properly.

Payment of the estimated annual liability

must be made with the extension application. When you file your composite return, attach a copy of your extension application to it. Obtain Form

from www.michigan.gov/treasury, Fiduciary Forms. Download a copy of the quarterly forms and complete one quarterly form. Use the name of the firm and the firm’s FEIN or the recipients Social Security number (SSN). Check the box labeled “CF” at the top of the voucher. Do not use the other three quarterly estimate forms.

Mailing refunds, assessments and correspondence

By signing the Michigan Composite Income Tax Return (Form 807), the signing partner or officer declares that the firm has power of attorney from each participant to file a composite return on his or her behalf. Treasury will mail refund

checks, assessments and all correspondence to the firm at the address indicated on the return. The firm must agree to be responsible for the payment of any additional tax, interest and penalties as finally determined. Issues involving the tax liability reported on a composite return will be resolved with the firm. In unusual circumstances, the department may contact the participants.

Attachments

Attach the following items to the composite return:

•A copy of pages 1, 2 and 3 of the U.S. 1065 or U.S. 1120S .

•A Michigan Schedule of Apportion- ment (Form

•All required forms

•Two schedules (one for participants and one for nonparticipants) listing each partner’s, shareholder’s or member's name, address, SSN and respective share of Michigan income and/or loss. If the participating member is another

•A statement signed by an authorized officer or general partner certifying that each participant has been informed of the terms and conditions of this program.

Lines not listed are explained on the form.

Line 10: Enter the apportionment percentage from Form

use the Single Business Tax apportionment percentage from Form

Line 13: The amount on this line should equal the total of lines 14, 15 and 16.

Line 21: Multiply the amount on line 20 by 3.95 percent (.0395).

Line 23: Enter the amount of withholding tax payments made on behalf of participating members.

The amount of withholding is calculated and remitted on a quarterly basis by multiplying the share of taxable income allocable to each member, adjusted for the allowable exemption amount for a quarter, times the income tax rate (4.0 percent through June 30, 2004 and 3.9 percent beginning July 1, 2004).

A

2004 807, PAGE 4

nonresident

Line 24: If line 22 plus line 23 is less than line 21, enter the balance of the tax due. This is the tax owed with the return. Enter any applicable penalties and interest in the spaces provided. Add tax, penalty and interest together and enter the total on this line. If balance due is less than $1, no payment is required. Make checks payable to “State of Michigan.” Write the firm’s FEIN, “Composite Return,” and the tax year on the front of the check. To ensure accurate processing of your return, send one check for each return type.

Line 27: Refund. Subtract line 26 from line 25. This is the refund. Treasury will not refund amounts less than $1.

Mail your completed return with payment (if applicable) to:

Composite Return

Michigan Department of Treasury

P.O. Box 30058

Lansing, MI 48909

Additions

Distributive Income Worksheet

Column A refers to Distributive Income categories from Schedule(s) K. Column B and C refer to lines on the U.S. 1065 Schedule K and U.S. 1120S Schedule K. Column D is the list of amounts that are added to arrive at total distributive income that is reported on Form 807, line 47.

A |

B |

|

C |

D |

U.S. 1065 |

|

U.S. 1120S |

Distributive Income |

|

Distributive Income Categories |

|

|||

Schedule K |

|

Schedule K |

Amounts |

|

|

|

|||

Ordinary income (loss) from trade or business |

1 |

|

1 |

|

activity |

|

|

||

|

|

|

|

|

Net income (loss) from rental real estate |

2 |

|

2 |

|

activity |

|

|

||

|

|

|

|

|

Net income (loss) from other rental activity |

3c |

|

3c |

|

|

|

|

|

|

Portfolio income (loss): |

|

|

|

|

Interest income |

5 |

|

4 |

|

|

|

|

|

|

Dividend income |

6a and 6b |

|

5a and 5b |

|

|

|

|

|

|

Royalty income |

7 |

|

6 |

|

|

|

|

|

|

Net |

8 |

|

7 |

|

|

|

|

|

|

Net |

9a |

|

8a |

|

|

|

|

|

|

Guaranteed payments |

4 |

|

|

|

|

|

|

|

|

Net gain (loss) under section 1231 |

10 |

|

9 |

|

|

|

|

|

|

Other income (loss) |

11 |

|

10 |

|

|

|

|

|

|

TOTAL DISTRIBUTIVE INCOME |

|

|

|

|

Add all amounts in Column D and carry total to Form 807, line 47. |

|

|

||

Lines 28 through 32: Enter income from lines 2, 3c, 4, 5a, 5b, 6, 7, 8a, 9 and 10 of 1120S Schedule K and from lines 2, 3c, 5, 6a, 6b, 7, 8, 9a, 10 and 11 of U.S. 1065 Schedule K. Guaranteed payments, income attributable to other Michigan fiduciaries or

Line 33: Enter the amount of state and local income taxes that was used to determine ordinary income on line 22 of the U.S. 1065 or line 21 of the U.S. 1120S.

Line 34: Enter other additions to income, such as gross interest and dividends from obligations or securities of states and their political subdivisions other than Michigan.

Subtractions

Note: Charitable contributions and other amounts reported as itemized deductions on U.S. SCHEDULE A are not allowable subtractions in determining Michigan taxable income.

Line 36: Enter income (loss) from other fiduciaries or other

income. Attach a schedule showing the location of companies and amount of income attributable to each.

Line 37: Enter amounts such as interest from U.S. obligations that are included in line 30a, and other deductions for AGI (above the line) that were not included in determining ordinary income. This includes section 179 depreciation and amounts included on line 12[d][2] of U.S. 1120S Schedule K and on line 13[d][2] of U.S. 1065 Schedule K. Attach a schedule of all subtractions.

Michigan allocated income or loss

Line 39: Enter the portion of guaranteed payments attributable to services performed in Michigan by the nonresident participants.

Line 40: Enter income from other fiduciaries or other

Line 41: Enter gains/losses from the sale of real or personal property located in Michigan not subject to apportionment.

Line 42: Enter any other income (loss) allocated to Michigan. Include any Michigan net operating loss deduction (NOLD). Partnerships may include the Section 179 expenses on property located in Michigan as a deduction here. Attach schedules.

Exemption Allowance

Line 47: Enter the total distributive income as determined using the worksheet on this page.

Line 48: Compute the percentage of income attributable to Michigan by dividing total Michigan income (line 46) by the total distributive income (line 47). This figure may not exceed 100 percent.

SEP, SIMPLE or qualified plan subtractions

SEP - Simplified Employee Pensions

SIMPLE - Savings Incentive Match Plan for Employees

Line 50: Figure the portion of SEP, SIMPLE or qualified plan subtractions which is attributable to the participants. Attach a schedule showing calculations.

Form Characteristics

| Fact Number | Description |

|---|---|

| 1 | The Michigan Department of Treasury 807 form is for the 2004 Composite Individual Income Tax Return for partnerships, S corporations, or other flow-through entities. |

| 2 | This form was due by April 15, 2005, requiring completion in blue or black ink. |

| 3 | It is issued under the authority of P.A. 281 of 1967, as amended. |

| 4 | Failure to file may result in penalties and interest charges, and could lead to the revocation of the filing agreement. |

| 5 | A flow-through entity doing business in Michigan and having two or more nonresident members must agree to comply with specific Michigan Department of Treasury rules. |

| 6 | The form requires attachments, including the first three pages of the U.S. 1065 or 1120S, the MI-1040H, and lists of participants and nonparticipants. |

| 7 | Participating members must not claim specific credits or have been full- or part-year Michigan residents, among other conditions. |

| 8 | Withholding tax payments are required for nonresident members, with due dates outlined in the instructions. |

| 9 | An extension can be requested by sending an estimated annual liability payment to the Treasury with a copy of an approved federal extension before the original due date. |

Guidelines on Utilizing Michigan 807

Filing the Michigan 807 form is a crucial step for certain businesses operating within the state. This form is specifically designed for partnerships, S corporations, and other flow-through entities that need to report composite individual income tax returns. It serves as a consolidated method for these entities to file on behalf of their nonresident members, simplifying the tax process. Understanding how to fill out this form accurately is essential to comply with Michigan's tax requirements and avoid potential penalties. Below, you'll find a step-by-step guide that outlines the necessary steps to complete the form accurately. By following these instructions, entities can ensure they meet their tax obligations efficiently.

- Type or print clearly in blue or black ink the Name of Partnership, S Corporation, or Other Flow-Through Entity in the designated space.

- Enter the entity's Federal Employer Identification or TR Number.

- Provide the Mailing Address (including Street, P.O. Box or Rural Route No.), City, Village or Township, State, and ZIP Code.

- Calculate and enter the Ordinary income (loss) from line 22 of U.S. 1065 or line 21 of U.S. 1120S.

- List any Additions from line 35, page 2, and enter the total.

- Add lines 5 and 6 to get the Subtotal.

- Detail any Subtractions from line 38, page 2, and subtract this from the subtotal to find the Total income subject to apportionment.

- Enter the Apportionment percentage from MI-1040H. Be cautious and see instructions to ensure accuracy.

- Calculate the Total Michigan apportioned income by multiplying line 9 by the percentage on line 10.

- Enter Michigan allocated income or (loss) from line 43, page 2.

- Add lines 11 and 12 to get the Total Michigan income.

- Enter Michigan income that is attributable to Michigan residents, nonparticipating nonresidents, and participants in lines 14, 15, and 16, respectively.

- Calculate the Exemption allowance from line 49, page 2, and SEP, SIMPLE or qualified plan deductions from line 52, page 2. Combine these for the total in line 19.

- Subtract line 19 from line 16 to find the Taxable income.

- Multiply the taxable income by 3.95% (.0395) to calculate the Tax due.

- Enter any Michigan extension payments and credit forward plus Withholding tax payments.

- If applicable, calculate the TAX DUE or OVERPAYMENT following the instructions provided on the form.

- The responsible individual should sign and date the form, certifying its accuracy under penalty of perjury.

- Finally, mail the return with any applicable payment or attachments to the specified address on the form.

Once the Michigan 807 form has been submitted, the Department of Treasury will process the information. Entities should ensure all accompanying documents, as outlined in the form's instructions, are attached. This includes pages 1, 2, and 3 of the U.S. 1065 or 1120S, the MI-1040H, and lists of participants and nonparticipants, among others. Properly completing and submitting this form is vital for compliance with Michigan’s tax regulations. If there are further questions or if additional assistance is needed, contacting a tax professional or the Michigan Department of Treasury directly is advisable.

Crucial Points on This Form

What is the Michigan 807 form?

The Michigan 807 form is a Composite Individual Income Tax Return used by flow-through entities like partnerships, S corporations, and limited liability companies. These entities use this form to file income tax for their nonresident members collectively.

Who needs to file the Michigan 807 form?

Flow-through entities that operate in Michigan and have two or more nonresident members, such as partners or shareholders, are required to file this form. It is also important that both the entity and its members agree to follow the rules set by the Michigan Department of Treasury.

What is the due date for filing the Michigan 807 form?

For tax periods ending in 2004, the due date is April 15, 2005. Returns for periods ending in 2005 are due by April 15, 2006. If an extension is needed, it must be filed before the original due date.

How can an extension be requested for filing this form?

An extension can be requested by sending an estimated annual liability payment to the Treasury along with a copy of an approved federal extension, or by applying for a Michigan-specific extension using Form 4.

What attachments are required with the Michigan 807 form?

- A copy of pages 1, 2, and 3 of the U.S. 1065 or U.S. 1120S

- A Michigan Schedule of Apportionment (Form MI-1040H)

- All required MI-NR-K1 forms for each member

- Two schedules listing each member's details and share of Michigan income or loss

- A statement signed by an authorized officer certifying participant awareness

What are some key lines on the Michigan 807 form that require special attention?

- Line 10: Apportionment percentage from Form MI-1040H

- Line 13: Total Michigan income, sum of lines 11 and 12

- Line 21: Tax due calculation

- Line 23: Withholding tax payments for participating members

How is the tax due calculated on the Michigan 807 form?

The tax due is calculated by multiplying the income subject to tax, shown on line 20, by the tax rate of 3.95% (.0395).

What if the calculated tax is less than the withholding and payments made?

If the total tax is less than the amount already paid through withholdings and payments (lines 22 plus 23), then line 24 will show a TAX DUE, which should include any applicable interest and penalties.

Where should the Michigan 807 form be mailed?

The completed form, along with any payment if applicable, should be mailed to: Composite Return, Michigan Department of Treasury, P.O. Box 30058, Lansing, MI 48909.

Common mistakes

When filling out the Michigan 807 form, a common mistake is using the wrong ink color. The form specifically requires blue or black ink, but this detail is often overlooked. Ensuring that the form is filled out in the correct ink color is crucial for readability and processing accuracy.

Another frequent error involves the entity’s name and identification numbers. Some filers mistakenly enter incorrect or incomplete information for the name of the partnership, S Corporation, or other flow-through entity, and its Federal Employer Identification or TR Number. It is essential to review these entries carefully to avoid processing delays caused by identification errors.

Additionally, the attachment of necessary documents is often neglected. The form instructions clearly state that copies of pages 1, 2, and 3 of the U.S. 1065 or 1120S, the MI-1040H, a list of participants, and a list of nonparticipants must be attached. Failure to include these attachments can result in an incomplete submission, potentially leading to the assessment of penalty and interest.

Errors in the calculation of Michigan allocated income or loss on lines 39 through 42 also pose problems. Accurate allocation of guaranteed payments, other Michigan partnerships, S corporations, or fiduciaries, and Michigan capital gains or losses requires attention to detail and a thorough understanding of the source of income. Inaccuracies in this section may significantly affect the tax liability.

The calculation of the exemption allowance and SEP, SIMPLE, or qualified plan deductions are other areas where mistakes are common. On lines 17 and 18, filers often miscalculate these amounts, which can lead to an incorrect reporting of taxable income. It is important to follow the instructions carefully and ensure that the right percentage and amounts are applied.

Lastly, overlooking the tax due or overpayment sections (lines 21, 24, and 25) is a critical mistake. These lines require careful calculation and verification of withheld payments and estimated tax payments to accurately determine if there is tax due or an overpayment. An error here could affect the taxpayer’s financial responsibilities or delay potential refunds.

Documents used along the form

When handling Michigan Composite Individual Income Tax Returns, several documents often accompany the Michigan Department of Treasury 807 form, each serving a specific purpose in the composite filing process. Understanding these documents can streamline compliance and ensure accuracy in reporting.

- U.S. 1065 or U.S. 1120S – These forms are the backbone of the composite return, providing the initial income information. The U.S. 1065 form is for partnerships, while the U.S. 1120S form is for S Corporations. Pages 1, 2, and 3 of these documents must be attached to the Michigan 807 form to indicate the ordinary income or loss and other financial details.

- Michigan Schedule of Apportionment (Form MI-1040H) – This form calculates the apportionment percentage used to determine the portion of total income that is subject to Michigan tax. It is crucial for entities operating both within and outside Michigan.

- Form MI-NR-K1 – Required for each non-resident member of the composite return, this form details the share of Michigan income, deductions, and credits allocated to each member, ensuring proper income reporting.

- Participant and Nonparticipant Schedules – Lists that identify each member's share of the income or loss, along with their personal details. One schedule is for those participating in the composite return, and another is for those who are not, aiding in the precise allocation of income and responsibility.

- Power of Attorney Documentation – A signed statement from an authorized officer or general partner certifying that the entity has obtained the necessary power of attorney from each member participating in the composite return. This documentation is crucial for fulfilling the representation requirement.

These documents collectively support the Michigan 807 form, helping to clarify the income attributes and tax responsibilities of each entity member. Ensuring these are correctly filled out and submitted together with the 807 form can mitigate errors and facilitate a smoother processing of the composite tax return.

Similar forms

U.S. Form 1065 (Partnership Tax Return): Similar to the Michigan 807 Form, U.S. Form 1065 is used by partnerships to report their income, gains, losses, deductions, and credits to the IRS. Both forms require the breakdown of ordinary income and adjustments, albeit serving different tax jurisdictions (federal vs. state).

U.S. Form 1120S (S Corporation Tax Return): This form, much like the Michigan 807, is designed for S corporations to report income, losses, and dividends. Both forms share the need for an attachment detailing the income subject to apportionment and allocations to specific jurisdictions.

Form MI-1040H (Michigan Schedule of Apportionment): Directly referenced in the Michigan 807 form, this document is crucial for calculating the apportionment percentage of Michigan income, highlighting their interconnected roles in tax calculation and reporting.

Form 160 (Michigan Withholding Tax Payment): Similar in its use for tax compliance, Form 160 is used for remitting withholding tax payments. Michigan 807 composite filers also address withholding tax obligations, underlining the duty to manage taxes on behalf of members.

U.S. Schedule K-1 (Partner's Share of Income, Deductions, Credits, etc.): This form serves a role similar to portions of the Michigan 807 that require details on members’ shares of income or loss. It underlines the need to report individual allocations within composite entities.

Form 4 (Application for Extension of Time to File Michigan Tax Returns): Mentioned in the context of the Michigan 807, this application for extension shares the purpose of providing taxpayers extra time, illustrating procedural parallels in tax administration.

Form MI-1041ES (Estimated Income Tax Voucher for Fiduciaries): Though used for fiduciaries, it shares with the Michigan 807 form the concept of estimated tax payments, emphasizing forward-looking financial responsibility in tax matters.

Form 8832 (Entity Classification Election): While not directly linked, its purpose to classify businesses for federal tax treatment affects how entities might complete forms like Michigan 807, impacting their state tax obligations based on their chosen federal classification.

MI-NR-K1 (Michigan Schedule K-1 for Non-Residents): This form's specificity for non-resident income parallels the Michigan 807's section on non-participating nonresidents, allocating income to Michigan sources for tax purposes.

Form 7004 (Application for Automatic Extension of Time To File Certain Business Income Tax, Information, and Other Returns): While federal in scope, its function mirrors that of Michigan tax forms like the 807 or Form 4, providing necessary extensions and illustrating the broader tax filing system’s flexibility.

Dos and Don'ts

When preparing the Michigan 807 form, the Composite Individual Income Tax Return, it's crucial to follow guidelines to ensure accuracy and compliance with state tax laws. Below are practices to adopt and avoid for a smooth filing process:

Do:- Use blue or black ink: For clarity and legibility, always fill out the form using blue or black ink or type the information.

- Include necessary attachments: Ensure that pages 1, 2, and 3 of the U.S. 1065 or 1120S, Form MI-1040H, and lists of participants and nonparticipants are attached.

- Clearly detail Michigan income and allocations: Accurately report Michigan apportioned and allocated income to reflect the correct taxable income.

- Provide accurate participant lists: Attach detailed lists of participants and nonparticipants, including names, addresses, and Social Security numbers or FEINs.

- Apply the correct tax rates: Use the current year's tax rate when calculating tax due to ensure the correct amount is reported.

- Sign and date the form: Ensure that the form is signed and dated by the preparer and filer to validate the information provided.

- Check for overpayments or due tax: Accurately calculate whether there’s a tax due or an overpayment to avoid future discrepancies.

- Request an extension if needed: If you cannot meet the filing deadline, request an extension before the due date to avoid penalties.

- Include the appropriate payment: If there is tax due, include payment with the form and ensure the check is properly labeled with "State of Michigan" and the necessary identification numbers.

- Omit required information: Failing to provide complete information, including attachments, can lead to the rejection of the form or the assessment of penalties.

- Use incorrect identifiers: Avoid inaccuracies with the Federal Employer Identification or TR Number, which are crucial for processing.

- Ignore instructions for specific lines: Each line on the form has specific instructions, especially regarding apportionment and allocations; overlooking these can result in errors.

- Miscalculate the exemption allowance or deductions: Ensure the exemption allowance and any SEP, SIMPLE, or qualified plan deductions are correctly calculated and attributed to Michigan.

- Forget to account for withholding tax payments: Remember to include withholding tax payments made on behalf of nonresident members to avoid underpayment issues.

- Overlook the certification statement: The certification confirms the truthfulness of the information provided; overlooking this statement can have legal implications.

- Misplace the submission address: Make sure returns are sent to the correct address to avoid processing delays.

- Misinterpret the extension request process: An extension for filing doesn’t alleviate the obligation to estimate and pay any owed tax by the original due date.

- Fail to communicate with participants: It’s essential that participants are informed of their inclusion in the composite return and understand the implications.

Misconceptions

When discussing the Michigan 807 form, commonly used for Composite Individual Income Tax Returns by flow-through entities, it's crucial to address prevalent misunderstandings. This form is integral for entities such as partnerships, S corporations, and limited liability companies doing business in Michigan. Here, we address eight common misconceptions about the form and its requirements.

Only Michigan-based entities need to file: A crucial misunderstanding is thinking that only entities physically based in Michigan must file the Michigan 807 form. In reality, any flow-through entity that conducts business in Michigan and has two or more nonresident members must file, regardless of where it is based.

All members can participate in the composite return: Not all members of a flow-through entity are eligible to participate in the composite return. There are specific exclusions, such as individuals claiming various Michigan credits or nonresidents wanting to claim more than one Michigan exemption.

Filing the Composite Return is optional: While it might seem optional, filing this composite return is a requirement for eligible entities that opt for this filing method. This process simplifies the tax filing and payment process for nonresident members by allowing the entity to pay the tax collectively.

Extensions are automatically granted: To extend the filing due date, an entity must either have an approved federal extension or request a Michigan extension. Merely expecting an automatic extension could lead to penalties for late filing.

Withholding taxes are optional: Flow-through entities must withhold Michigan income tax on behalf of their nonresident members. This is not an optional process; it's a requirement, with payments due quarterly.

Any type of income is eligible for the composite return: Not all income qualifies for the composite return. Specific income types, such as from rental real estate activities or other Michigan sources, must be appropriately reported and might have unique requirements.

Penalties and interest are not a concern: Failing to file or incorrectly filing the Michigan 807 form can result in penalties, interest, and in severe cases, revocation of the filing agreement. Being diligent in fulfilling these obligations is crucial.

All information stays confidential: By signing the Michigan Composite Income Tax Return, the entity gives the Michigan Department of Treasury the right to contact individual members if necessary, and this also means that certain information will be shared with the entity for the purposes of handling tax liabilities and correspondences.

Understanding these core aspects of the Michigan 807 form can significantly streamline the tax filing process for flow-through entities and their members. Entities should ensure compliance by clearly understanding their obligations, the scope of income that must be reported, and the specific requirements for withholding and paying taxes on behalf of their members.

Key takeaways

- Understanding the eligibility for filing a Michigan 807 form is crucial. This form is designated for flow-through entities such as partnerships, S corporations, and limited liability companies that operate within Michigan and have nonresident members. It aims to simplify the state income tax filing process by allowing these entities to file a composite return on behalf of their nonresident members, under specific conditions.

- It's imperative to recognize the significance of adherence to deadlines when dealing with the Michigan 807 form. The form is due annually on April 15th, following the end of the tax year. For entities unable to meet this deadline, Michigan law allows the filing of an extension request. This request, however, must be accompanied by the estimated tax due to avoid penalties and interest for late payment.

- Making accurate withholding tax payments for nonresident members is a mandatory requirement for entities filing the Michigan 807 form. These payments should reflect the taxable income allocated to nonresident members and are due quarterly. Failure to comply with this requirement may lead to assessments of penalty and interest, emphasizing the need for entities to meticulously calculate and timely remit withholding taxes.

- Entities using the Michigan 807 form must include specific attachments along with their filing. These attachments include copies of relevant pages from the U.S. 1065 or 1120S forms, a Michigan Schedule of Apportionment, forms MI-NR-K1 for each member, and lists detailing participants and nonparticipants with their respective shares of Michigan income or loss. Such documentation is vital for validating the accuracy of the composite return and ensuring compliance with Michigan tax laws.

- The designation of a representative with power of attorney to act on behalf of all members under the composite return arrangement is a critical aspect. By signing Form 807, the entity affirms its responsibility for managing any tax liabilities, including additional tax, interest, and penalties, as assessed by the Michigan Department of Treasury. This highlights the importance of having a clear agreement among members regarding the delegation of authority and responsibility for managing tax affairs.

Popular PDF Templates

State of Michigan Forms - Guidance on specifying the type of ownership for the nursery stock business, including options such as corporation, sole ownership, and partnership.

Electronic Certificate of Origin - An authoritative form in Michigan, detailing the inception and make of a vehicle.