Michigan 2766 PDF Form

In the realm of property transfers within Michigan, the Michigan Department of Treasury's L-4260, form 2766, stands as a crucial document. Mandated by P.A. 415 of 1994, its completion is obligatory for the new owners of both real estate and certain types of personal property, even in the absence of a deed recording. This Property Transfer Affidavit serves a pivotal role by ensuring that the transfer of ownership is officially recorded with the local assessor's office within a strict 45-day window following the transaction. Detailed within this form are segments that capture a comprehensive range of data, from the property's street address and county to the transfer date, buyer and seller information, as well as the purchase price. It goes beyond basic details by delving into optional items which, if provided, can streamline the process by precluding further queries. Special attention is also given to exemptions aimed at preventing the uncapping of property taxes under specific conditions, emphasizing the form's role in the nuanced territory of property tax regulation. Included within are certifications to uphold the accuracy of the information provided, underscoring the legal responsibilities entailed in such transfers. The penalties for non-compliance—ranging from additional taxes to monetary fines—highlight the importance of adhering to the stipulations laid out in the legislation, making form 2766 a cornerstone in the transfer and assessment of property within Michigan.

Preview - Michigan 2766 Form

Michigan Department of Treasury |

|

2766 (Rev. |

|

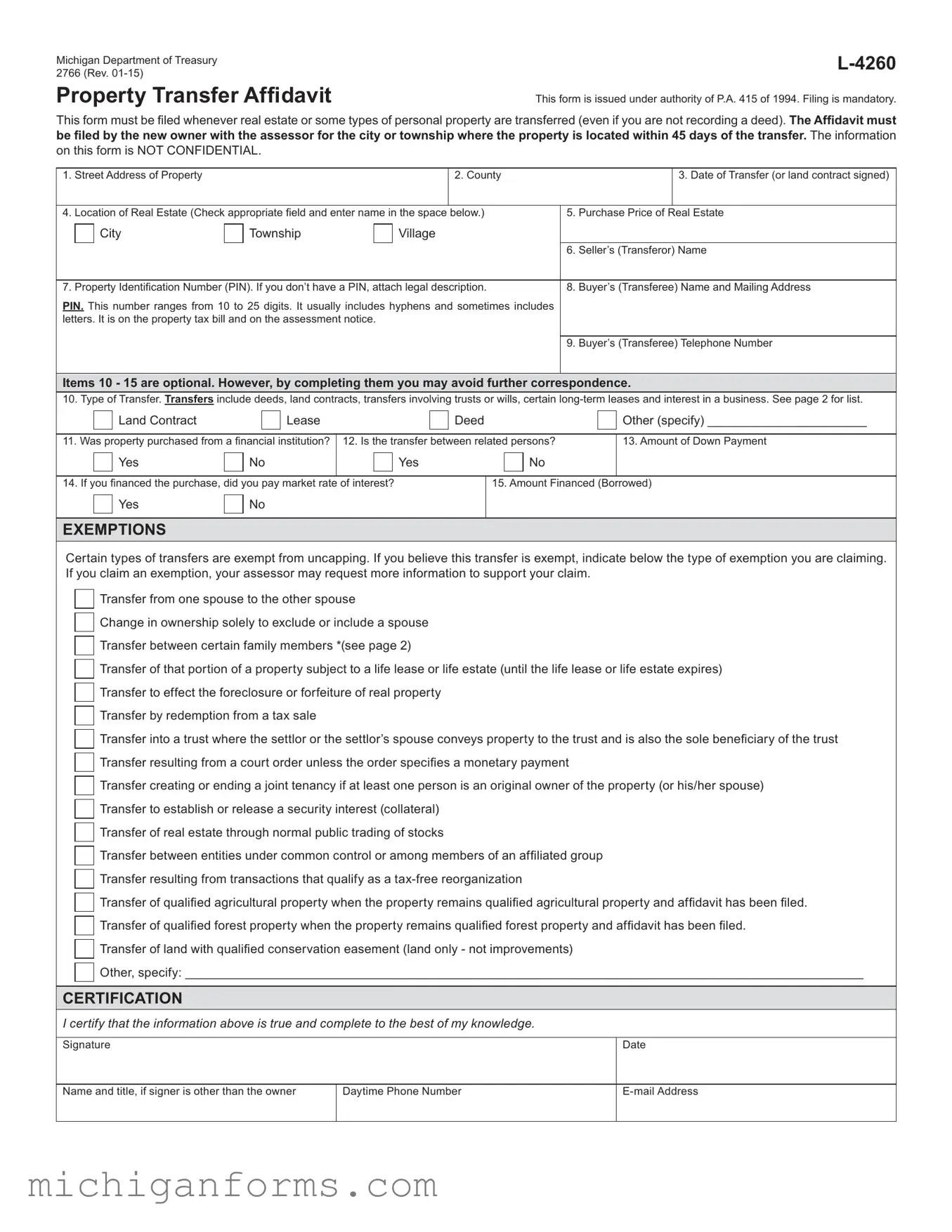

Property Transfer Afidavit

This form is issued under authority of P.A. 415 of 1994. Filing is mandatory.

This form must be iled whenever real estate or some types of personal property are transferred (even if you are not recording a deed). The Afidavit must be iled by the new owner with the assessor for the city or township where the property is located within 45 days of the transfer. The information

on this form is NOT CONFIDENTIAL.

1. |

Street Address of Property |

|

|

|

|

2. County |

|

|

3. Date of Transfer (or land contract signed) |

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Location of Real Estate (Check appropriate ield and enter name in the space |

below.) |

5. |

Purchase Price of Real Estate |

||||||

|

|

City |

|

Township |

|

Village |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

6. |

Seller’s (Transferor) Name |

|

|

|

|

|

|

|

|

|

|

|

|

7. |

Property Identiication Number (PIN). If you don’t have a PIN, attach legal description. |

8. |

Buyer’s (Transferee) Name and Mailing Address |

|||||||

PIN. This number ranges from 10 to 25 digits. It usually includes hyphens and sometimes includes |

|

|

|

|||||||

letters. It is on the property tax bill and on the assessment notice. |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. |

Buyer’s (Transferee) Telephone Number |

|

|

|

|

|

|

|

|

|

|

|

|

Items 10 - 15 are optional. However, by completing them you may avoid further correspondence.

10.Type of Transfer. TRANSFERS include deeds, land contracts, transfers involving trusts or wills, certain

|

|

Land Contract |

|

|

|

Lease |

|

|

|

|

Deed |

|

Other (specify) _______________________ |

|||

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

||||||||||||

11. Was property purchased from a inancial institution? |

12. Is the transfer between related persons? |

|

13. Amount of Down Payment |

|||||||||||||

|

|

Yes |

|

No |

|

|

Yes |

|

|

|

|

No |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

14. If you inanced the purchase, did you pay market rate |

of interest? |

|

|

15. Amount Financed (Borrowed) |

||||||||||||

|

|

Yes |

|

No |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EXEMPTIONS

Certain types of transfers are exempt from uncapping. If you believe this transfer is exempt, indicate below the type of exemption you are claiming. If you claim an exemption, your assessor may request more information to support your claim.

Transfer from one spouse to the other spouse

Change in ownership solely to exclude or include a spouse

Transfer between certain family members *(see page 2)

Transfer of that portion of a property subject to a life lease or life estate (until the life lease or life estate expires)

Transfer to effect the foreclosure or forfeiture of real property

Transfer by redemption from a tax sale

Transfer into a trust where the settlor or the settlor’s spouse conveys property to the trust and is also the sole beneiciary of the trust Transfer resulting from a court order unless the order speciies a monetary payment

Transfer creating or ending a joint tenancy if at least one person is an original owner of the property (or his/her spouse)

Transfer to establish or release a security interest (collateral)

Transfer of real estate through normal public trading of stocks

Transfer between entities under common control or among members of an afiliated group Transfer resulting from transactions that qualify as a

Transfer of qualiied agricultural property when the property remains qualiied agricultural property and afidavit has been iled. Transfer of qualiied forest property when the property remains qualiied forest property and afidavit has been iled.

Transfer of land with qualiied conservation easement (land only - not improvements)

Other, specify: __________________________________________________________________________________________________

CERTIFICATION

I certify that the information above is true and complete to the best of my knowledge.

Signature

Date

Name and title, if signer is other than the owner

Daytime Phone Number

2766, Page 2

Instructions:

This form must be iled when there is a transfer of real property or one of the following types of personal property:

•Buildings on leased land.

•Leasehold improvements, as deined in MCL Section 211.8(h).

•Leasehold estates, as deined in MCL Section 211.8(i) and (j).

Transfer of ownership means the conveyance of title to or a present interest in property, including the beneicial use of the property. For complete descriptions of qualifying transfers, please refer to MCL Section

Excerpts from Michigan Compiled Laws (MCL), Chapter 211

*Section 211.27a(7)(t): Beginning December 31, 2014, a transfer of residential real property if the transferee is the transferor’s or the transferor’s spouse’s mother, father, brother, sister, son, daughter, adopted son, adopted daughter, grandson, or granddaughter and the residential real property is not used for any commercial purpose following the conveyance. Upon request by the department of treasury or the assessor, the transferee shall furnish proof within 30 days that the transferee meets the requirements of this subparagraph. If a transferee fails to comply with a request by the department of treasury or assessor under this subparagraph, that transferee is subject to a ine of $200.00.

Section 211.27a(10): “... the buyer, grantee, or other transferee of the property shall notify the appropriate assessing ofice in the local unit of government in which the property is located of the transfer of ownership of the property within 45 days of the transfer of ownership, on a form prescribed by the state tax commission that states the parties to the transfer, the date of the transfer, the actual consideration for the transfer, and the property’s parcel identiication number or legal description.”

Section 211.27(5): “Except as otherwise provided in subsection (6), the purchase price paid in a transfer of property

is not the presumptive true cash value of the property transferred. In determining the true cash value of transferred property, an assessing oficer shall assess that property using the same valuation method used to value all other property of that same classiication in the assessing jurisdiction.”

Penalties:

Section 211.27b(1): “If the buyer, grantee, or other transferee in the immediately preceding transfer of ownership of property does not notify the appropriate assessing ofice as required by section 27a(10), the property’s taxable value shall be adjusted under section 27a(3) and all of the following shall be levied:

(a)Any additional taxes that would have been levied if the transfer of ownership had been recorded as required under this act from the date of transfer.

(b)Interest and penalty from the date the tax would have been originally levied.

(c)For property classiied under section 34c as either industrial real property or commercial real property, a penalty in the following amount:

(i)Except as otherwise provided in subparagraph (ii), if the sale price of the property transferred is $100,000,000.00 or less, $20.00 per day for each separate failure beginning after the 45 days have elapsed, up to a maximum of $1,000.00.

(ii)If the sale price of the property transferred is more than $100,000,000.00, $20,000.00 after the 45 days have elapsed.

(d)For real property other than real property classiied under section 34c as industrial real property or commercial real property, a penalty of $5.00 per day for each separate failure beginning after the 45 days have elapsed, up to a maximum of $200.00.

Form Characteristics

| Fact | Detail |

|---|---|

| Governing Law | Issued under Public Act 415 of 1994 |

| Mandatory Filing | Filing of this form is required whenever real estate or certain types of personal property are transferred. |

| Filing Deadline | The affidavit must be filed within 45 days of the property transfer. |

| Filing Location | Must be filed with the assessor for the city or township where the property is located. |

| Confidentiality | The information provided on this form is not confidential. |

| Exemptions | Includes certain types of transfers that are exempt from uncapping of the property's taxable value. |

| Penalties for Non-Compliance | Includes additional taxes, interest, penalties, and specific fines for failure to file within the prescribed timeframe. |

| Legal Requirement for Notification | The transfer of ownership must be reported to the appropriate assessing office within 45 days on a state-prescribed form. |

Guidelines on Utilizing Michigan 2766

Filling out the Michigan 2766 form, officially known as the Property Transfer Affidavit, is a necessary step when real estate or certain types of personal property are transferred. This mandatory document helps ensure that property records accurately reflect current ownership and assists in the proper assessment of property taxes. It needs to be submitted to the local city or township assessor within 45 days of the property transfer. Here are the steps to complete this form correctly to avoid potential fines and ensure a smooth transition of property ownership.

- Begin by entering the Street Address of the Property in the first field provided.

- Fill in the County where the property is located.

- Provide the Date of Transfer (or when the land contract was signed), ensuring accuracy as this will be cross-referenced with records.

- Under Location of Real Estate, check the appropriate field (City, Township, Village) and then enter the name of the location in the space provided.

- Enter the Purchase Price of Real Estate as this information is used in assessing property taxes.

- List the Seller’s (Transferor) Name for record.

- Provide the Property Identification Number (PIN). If this is not known, attach a legal description of the property. The PIN is crucial for identifying the property in municipal records.

- Fill in the Buyer’s (Transferee) Name and Mailing Address. This is essential for all future correspondences and tax billings related to the property.

- Include the Buyer’s (Transferee) Telephone Number, facilitating easy contact by the assessor's office if needed.

- Items 10 - 15 are optional but completing them can prevent future requests for information. They include details about the type of transfer, financial questions related to the purchase, and any exemptions you believe apply to the transfer. Closely review these options and fill in as needed, ensuring to specify any other type of transfer or exemption not listed.

- Finally, certify that all information provided is true and complete to the best of your knowledge by signing and dating the document. Include your name and title if signing on behalf of a company or organization and provide a daytime phone number and email for any follow-up communication.

Once the form is completed, submit it to the assessor's office of the city or township where the property is located. Doing this within the mandated 45-day window is crucial to avoid penalties and ensure that property tax assessments reflect the new ownership accurately. Remember to keep a copy of the submitted form for your records.

Crucial Points on This Form

What is the Michigan 2766 form?

The Michigan 2766 form, also known as the Property Transfer Affidavit, is a document required by the Michigan Department of Treasury. It is used to report the transfer of real estate or certain types of personal property. This affidavit must be filed by the new owner with the assessor of the city or township where the property is located, within 45 days of the transfer.

When is filing the Michigan 2766 form mandatory?

Filing the Michigan 2766 form is mandatory whenever there is a transfer of ownership in real estate or certain kinds of personal property, regardless of whether a deed is recorded.

Where should I file the Michigan 2766 form?

The completed form must be filed with the assessor's office in the city or township where the property is located.

What information do I need to complete the form?

To complete the form, you'll need the following information:

- Street Address of Property

- County

- Date of Transfer

- Location of Real Estate

- Purchase Price of Real Estate

- Seller's and Buyer's Names and Addresses

- Property Identification Number (PIN)

- Type of Transfer

- Other relevant transaction details

What types of transfers does the Michigan 2766 form cover?

This form covers various types of transfers, including:

- Deeds

- Land contracts

- Transfers involving trusts or wills

- Certain long-term leases

- Interest in a business

Are there any exemptions to this form?

Yes, certain types of transfers are exempt from uncapping. Exemptions include transfers between family members, transfers to or from trusts under specific conditions, and transfers resulting from court orders without monetary payment, among others. If you believe your transfer qualifies for an exemption, it should be indicated on the form, and the assessor may request additional information to verify the claim.

What happens if I don't file the form within 45 days?

If the form is not filed within 45 days of the transfer, the property's taxable value may be adjusted. Penalties include additional taxes that would have been levied, interest, and fines that vary based on property classification and the sale price of the property transferred.

Can I find the Property Identification Number (PIN) on the form?

The Property Identification Number (PIN) is not found on the form itself. It usually ranges from 10 to 25 digits, can include hyphens and sometimes letters, and is found on the property tax bill and the assessment notice. If you don't have a PIN, you must attach the legal description of the property.

How can I know if my property transfer requires filing this affidavit?

If there's a change in ownership of real property or certain personal property types as defined in the Michigan Compiled Laws, you are required to file this affidavit. If in doubt, consult the local assessor's office in the city or township where the property is located or seek legal advice to determine your obligation.

Common mistakes

When people fill out the Michigan 2766 form, often required for transferring property ownership, several common mistakes can complicate the process. One typical error involves inaccurately reporting the property's street address. This detail is crucial for ensuring the transfer is recorded against the correct property. Inaccuracies can lead to significant delays and confusion in the property's official records, affecting future transactions.

Another common mistake is incorrectly entering the Property Identification Number (PIN). This number, crucial for identifying the property in county records, can be complex, with a mix of up to 25 digits, letters, and hyphens. Misreporting the PIN can misdirect the property transfer documents, potentially affecting the ownership records. It's essential to double-check this number on official documents, such as the property tax bill or assessment notice, to ensure accuracy.

Incorrectly stating the date of transfer is another frequent issue on the form. This date should reflect when the property ownership officially changed hands, such as when a deed is signed or a land contract is executed. Providing the wrong date can affect the timeliness of the filing and may lead to penalties for filing outside the mandated 45-day window. This accuracy ensures the transfer is documented in a timely manner, aligning with legal requirements.

Lastly, people often overlook the importance of thoroughly completing optional items 10 through 15. Although labeled as optional, filling out these sections can significantly streamline the process by reducing the need for further correspondence. These details provide additional context about the transfer, helping to clarify the nature of the transaction and any financial arrangements involved. Taking the time to provide this information can expedite the property's official transfer record.

Documents used along the form

When navigating property transfers in Michigan, it's crucial to complement the Michigan Department of Treasury 2766 (L-4260) Property Transfer Affidavit with several key forms and documents. Each plays a vital role in ensuring compliance with legal requirements and smoothing the transaction process.

- Deed of Sale: This document officially records the sale and transfer of property ownership. It includes details about the buyer, seller, and the property itself.

- Title Insurance Policy: Offers protection against future claims or unforeseen liens on the property. It assures the buyer of clear ownership.

- Property Tax Statements: Reflecting the current standing of property taxes, these statements are vital for understanding the financial obligations that come with the property.

- Mortgage Documents: If the property purchase is being financed, these documents outline the terms of the mortgage, including interest rates, repayment schedule, and the rights of the lender.

- Closing Disclosure: A detailed breakdown of all the financial transactions and costs involved in the property transfer, including fees, taxes, and other charges.

- Home Inspection Reports: Provide detailed information on the condition of the property, including potential issues that could affect its value or future use.

- Title Search and Abstract: A comprehensive record of the property’s history, confirming the legal ownership and revealing any easements, restrictions, or other important details.

- Land Contract: If the property is being bought through a land contract, this document outlines the agreement between the seller and buyer, including payment terms, interest, and conditions of the sale.

Together, these documents ensure a transparent and lawful transfer of property, safeguarding the interests of all parties involved. It's advisable to consult with a legal professional to navigate the complexities of property transfers and to ensure that all necessary paperwork is properly completed and filed.

Similar forms

Real Estate Transfer Declaration (Illinois PTAX-203): Like Michigan's Form 2766, the PTAX-203 must be filed whenever a real estate transaction occurs, providing details of the transaction to the relevant local government. Both forms collect information about the property, sale price, and parties involved to ensure proper assessment and taxation.

Uniform Conveyancing Blanks (Minnesota): Similar to Form 2766, these documents are used in Minnesota for the transfer of real property. They include a variety of forms that detail the transfer of ownership, covering many of the same points such as buyer and seller information, property details, and the nature of the transaction.

Grant Deed (California): Although more specific as a deed type, California's Grant Deed shares similarities with Form 2766 in that it is involved in the process of transferring ownership of real estate. It requires disclosure of the grantor (seller), grantee (buyer), and legal description of the property, which aligns with the information collected in Michigan's property transfer affidavit.

Statement of Value (Pennsylvania REV-183): This form is required for real estate transactions in Pennsylvania, particularly when a deed is filed without the full sale price or when certain exemptions are claimed. Like the 2766 form, the Statement of Value provides a means to assess the property's value for taxation, requiring similar details about the transaction and the property itself.

General Warranty Deed Forms (Multiple States): General Warranty Deeds, while varying by state, serve the function of transferring property ownership with a guarantee against any liens or encumbrances. They necessitate detailed information about the transfer similar to Form 2766, including the identities of the buyer and seller, property description, and the transfer's terms, underscoring the transparency and accountability in property transactions.

Dos and Don'ts

When filling out the Michigan 2766 form, a Property Transfer Affidavit, there are key dos and don'ts to ensure the process is completed correctly and efficiently. This step is crucial whenever real estate or certain types of personal property are transferred. Here's a quick guide on what to do and what not to do.

Things You Should Do:

- Provide accurate information for all required fields: Ensure you fill in every mandatory field with correct information, including the street address of the property, the county, the date of transfer, and purchase price, among others.

- Include the Property Identification Number (PIN): This is a critical piece of information that uniquely identifies the property. It's found on the property tax bill or the assessment notice and is essential for processing the affidavit.

- Report any applicable exemptions: If your property transfer qualifies for exemptions from uncapping, correctly indicate the type of exemption you are claiming. This could save you from unnecessary taxation or correspondence.

- Sign and date the form: A signed and dated form is considered valid and complete. Ensure that the person with the authority to sign, whether the owner or a legally designated individual, does so before submission.

Things You Shouldn't Do:

- Delay filing the form: The affidavit must be filed within 45 days of the property transfer. Submitting the form late could result in penalties, including additional taxes, interest, and fines.

- Leave sections incomplete: Even though items 10 to 15 are optional, filling them out can prevent further communication needs and clarify any doubts right from the outset.

- Forget to include a legal description if the PIN is unavailable: If for some reason the Property Identification Number is not available, attach a legal description of the property to ensure there are no delays or confusions in the filing process.

- Assume information is confidential: Understand that the information provided on the form is not confidential. Being transparent and providing accurate information is vital as this documentation becomes part of public records.

Being attentive to these guidelines can help smooth the process of transferring property and ensure compliance with Michigan's Department of Treasury requirements.

Misconceptions

There are several misconceptions about the Michigan 2766 form, commonly known as the Property Transfer Affidavit. Understanding these can help individuals navigate the complexities of property transfer with greater confidence.

- Misconception 1: The form is optional.

This is incorrect. Whenever there is a transfer of real estate or certain types of personal property, the Michigan 2766 form must be filed. This requirement ensures that the assessor's records are up-to-date, reflecting the current property owner.

- Misconception 2: The information provided on the form is confidential.

The information on the Property Transfer Affidavit is not confidential. It is accessible by the public, which means that the details you provide can be reviewed by anyone seeking information about the property transfer.

- Misconception 3: Only transfers of real estate need to be reported.

In addition to real estate transactions, the transfer of certain personal property types must also be reported using this form. This includes buildings on leased land, leasehold improvements, and leasehold estates, among others.

- Misconception 4: The form must be filed with the state tax commission.

The completed affidavit should be filed with the assessor of the city or township where the property is located, not with the state tax commission. This ensures that local records accurately reflect the property's ownership.

- Misconception 5: There is no deadline for filing.

The correct procedure requires filing the form within 45 days of the property transfer. Failing to meet this deadline can result in penalties, including additional taxes, interest, and penalties.

- Misconception 6: All property transfers result in a taxable value uncapping.

There are exemptions to this rule. Certain types of property transfers, such as those between family members or into a trust where the settlor is the sole beneficiary, may not trigger a taxable value reassessment.

- Misconception 7: The purchase price must always be disclosed.

While the purchase price is a critical piece of information on the form, there are specific situations where a property's purchase price doesn't determine its true cash value for assessment purposes.

- Misconception 8: Penalties for late filing are negligible.

The penalties for late filing can be substantial, including additional taxes, interest, and a daily penalty until the affidavit is filed, especially for properties with a transfer price over $100,000,000.

- Misconception 9: The form is only for buyer's use.

While it is the new owner's responsibility to file the form, both the buyer and seller should be aware of its requirements and ensure that it is completed accurately to avoid potential disputes or penalties.

- Misconception 10: Any mistakes on the form are inconsequential.

Errors can have significant implications, including incorrect assessment of the property's taxable value. It's crucial to provide accurate and complete information to avoid legal and financial repercussions.

Clearing up these misconceptions can lead to a smoother property transfer process and help new owners comply with Michigan's legal requirements, ensuring that all parties involved are well-informed and protected.

Key takeaways

Filing the Michigan 2766 form, officially known as the Property Transfer Affidavit, is a mandatory step following the acquisition of real estate or certain types of personal property. It is vital for the new owner to understand the implications and requirements to ensure compliance with state laws. Here are seven key takeaways regarding the completion and utilization of this form:

- The Michigan 2766 form must be filed with the assessor of the city or township where the property is located within 45 days of the property transfer.

- It is important to note that the information provided on this form is not confidential, which means it is accessible to the public.

- The form requires detailed information about the transaction, including the street address of the property, the county, date of transfer, purchase price, and the parties involved in the transfer.

- A Property Identification Number (PIN) is crucial for the form's completion. If the PIN is not available, a legal description of the property must be attached.

- Optional sections are included to help avoid further correspondence; however, completing items 10 through 15 can streamline the process and provide additional clarity on the nature of the transfer.

- Understanding the exemptions is crucial; certain types of transfers are exempt from uncapping, which can affect the property’s taxable value. Proper identification of an exempt transfer can save the new owner from unnecessary adjustments.

- Failure to file the form or incorrect filings can result in penalties, including additional taxes, interest, and fines. The severity of these penalties can vary based on the property's classification and the sale price.

Accurate completion and timely submission of the Michigan 2766 form are integral to maintaining compliance with state tax laws and avoiding penalties. New property owners or transferees should carefully review all provided instructions and seek clarification on any points of uncertainty to ensure proper filing.

Popular PDF Templates

5080 Form 2024 - Mandates taxpayer or official representative certification, underscoring the legal responsibility for accuracy.

Uia 1733 - Form UIA 1015-C explores worker benefits and tax responsibilities, which are indicators of employment nature.