Michigan 2271 PDF Form

In Michigan, concessionaires and vendors participating in events are governed by a precise tax reporting obligation, detailed in the Michigan Department of Treasury 2271 form. This form, a crucial document for operating within legal boundaries, mandates the reporting and payment of sales, use, and withholding taxes derived from sales at events. Specifically designed to simplify compliance, this formcovers diverse aspects such as the collection of a 6% sales tax on all tangible personal property sold, the remittance of use tax for goods used in the vendor's business, and the withholding of income tax for employees. Calculations are streamlined through explicit instructions for reporting gross sales, taxable sales, and taxes due, including considerations for late payment penalties and interest. Additionally, the form provides guidance on the rounding of sales tax amounts, direct percentage computation for withholding, and detailed payment instructions, including a specific address for mailing and a requirement for timely submission to avoid estimated tax assessments. The introduction of such a form underscores Michigan's commitment to ensuring tax compliance while offering a structured yet comprehensive approach for vendors to follow, aiming to ease the administrative burden and facilitate the understanding of tax obligations linked to event sales.

Preview - Michigan 2271 Form

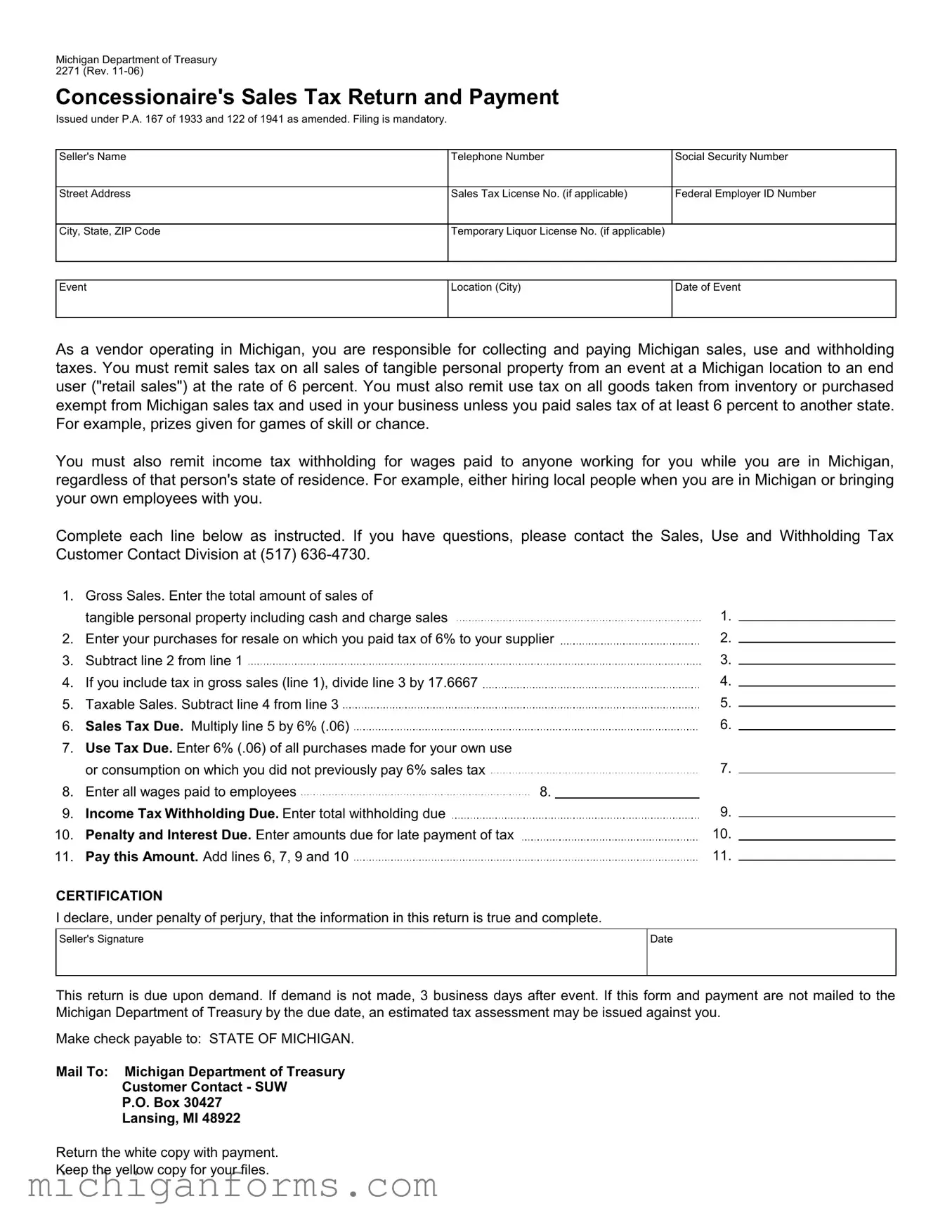

Michigan Department of Treasury 2271 (Rev.

Concessionaire's Sales Tax Return and Payment

Issued under P.A. 167 of 1933 and 122 of 1941 as amended. Filing is mandatory.

Seller's Name |

Telephone Number |

Social Security Number |

|

|

|

Street Address |

Sales Tax License No. (if applicable) |

Federal Employer ID Number |

|

|

|

City, State, ZIP Code |

Temporary Liquor License No. (if applicable) |

|

|

|

|

Event

Location (City)

Date of Event

As a vendor operating in Michigan, you are responsible for collecting and paying Michigan sales, use and withholding taxes. You must remit sales tax on all sales of tangible personal property from an event at a Michigan location to an end user ("retail sales") at the rate of 6 percent. You must also remit use tax on all goods taken from inventory or purchased exempt from Michigan sales tax and used in your business unless you paid sales tax of at least 6 percent to another state. For example, prizes given for games of skill or chance.

You must also remit income tax withholding for wages paid to anyone working for you while you are in Michigan, regardless of that person's state of residence. For example, either hiring local people when you are in Michigan or bringing your own employees with you.

Complete each line below as instructed. If you have questions, please contact the Sales, Use and Withholding Tax Customer Contact Division at (517)

1.Gross Sales. Enter the total amount of sales of

tangible personal property including cash and charge sales

2.Enter your purchases for resale on which you paid tax of 6% to your supplier

3.Subtract line 2 from line 1

4.If you include tax in gross sales (line 1), divide line 3 by 17.6667

5.Taxable Sales. Subtract line 4 from line 3

6.Sales Tax Due. Multiply line 5 by 6% (.06)

7.Use Tax Due. Enter 6% (.06) of all purchases made for your own use or consumption on which you did not previously pay 6% sales tax

8. Enter all wages paid to employees |

8. |

9.Income Tax Withholding Due. Enter total withholding due

10.Penalty and Interest Due. Enter amounts due for late payment of tax

11.Pay this Amount. Add lines 6, 7, 9 and 10

CERTIFICATION

I declare, under penalty of perjury, that the information in this return is true and complete.

1.

2.

3.

4.

5.

6.

7.

9.

10.

11.

Seller's Signature

Date

This return is due upon demand. If demand is not made, 3 business days after event. If this form and payment are not mailed to the Michigan Department of Treasury by the due date, an estimated tax assessment may be issued against you.

Make check payable to: STATE OF MICHIGAN.

Mail To: Michigan Department of Treasury

Customer Contact - SUW

P.O. Box 30427

Lansing, MI 48922

Return the white copy with payment.

Keep the yellow copy for your files.

Sales Tax Collection

Retailers are required to remit a 6% sales tax on their taxable retail sales to the State of Michigan. Effective January 1, 2006, a retailer must calculate the amount of sales tax to collect by using the following rounding formula.

To determine the amount of tax to remit, compute the tax to the third decimal place and round up to a whole cent when the third decimal place is greater than four, or down to a whole cent when the third decimal point is four or less.

How to Compute Withholding

To calculate tax amounts to withhold, employers may use a direct percentage computation (example shown below) or use the Michigan Income Tax Withholding Table. This table is found in Form 446, Michigan Income Tax Withholding Guide. Additional information regarding sales, use and withholding taxes, as well as Form 446 and the income tax withholding tables, is available by visiting the Michigan Treasury Web site www.michigan.gov/businesstaxes.

|

2007 |

2006 |

Payroll Period |

Allowance per Exemption |

Allowance per Exemption |

Per Day |

9.32 |

$9.04 |

Weekly |

65.38 |

$63.46 |

Withholding Formula

[Compensation - (allowance per exemption x number of exemptions)] x Calendar Year's Withholding Tax Rate. Example: An employee with 3 exemptions earns $600/week in 2007 - the 2007 withholding tax rate is 3.9%.

The Direct Percentage Calculation is:

[$600 - ($65.38 x 3)] x 3.9% = Amount to withhold [$600 - $196.14] x .039 = $15.75

How to Compute Penalty and Interest

If a return is not filed or tax is not paid within three days of your event, you must include penalty and interest with your payment. Penalty is 5% of the tax due. Penalty increases by an additional 5% per month or fraction thereof, after the second month, to a maximum of 25%. Interest is charged daily using the average prime rate, plus 1 percent.

You may refer to our Web site for current interest rate information, or help in calculating late payment fees.

www.michigan.gov/treasury

Form Characteristics

| Fact Name | Description |

|---|---|

| Form Reference | Michigan Department of Treasury 2271 (Rev. 11-06) |

| Governing Laws | Issued under P.A. 167 of 1933 and 122 of 1941 as amended. |

| Filing Requirement | Filing is mandatory for concessionaires operating in Michigan. |

| Tax Responsibility | Concessionaires must remit sales tax on all retail sales and use tax on goods used in business at a rate of 6%. |

| Income Tax Withholding | Income tax withholding is required for wages paid to employees during the event in Michigan. |

| Payment Calculation | Sales tax is calculated using a specific rounding formula detailed in the form instructions. |

| Penalty and Interest | Penalty and interest are due for late payment or filing, calculated from three days after the event. |

| Payment and Mailing Information | Payments are made payable to STATE OF MICHIGAN and mailed to Michigan Department of Treasury indicated address. |

Guidelines on Utilizing Michigan 2271

After a successful event in Michigan, it's essential to settle your financial obligations with the state. This includes the remittance of sales, use, and withholding taxes generated from sales at your event. The Michigan Department of Treasury 2271 form is specifically designed for concessionaires and vendors to declare and pay these taxes efficiently. Filling out this form is a straightforward process but requires accuracy to ensure compliance with state tax laws. The following steps will guide you through completing the form properly. Remember, timely submission of this form, along with the correct payment, helps avoid penalties and interest charges for late remittance.

- Enter your Seller's Name, Telephone Number, and Social Security Number or Federal Employer ID Number in the designated spaces.

- Provide your Street Address, including City, State, ZIP Code, and, if applicable, your Sales Tax License No. and Temporary Liquor License No..

- Specify the Event Location (City) and the Date of Event.

- For Gross Sales, enter the total amount of tangible personal property sales, inclusive of cash and charge sales.

- Input the amount for purchases made for resale on which you paid a 6% tax to your supplier.

- Subtract the amount in step 5 from the amount in step 4 to find the difference.

- If your gross sales include tax, divide the result from step 6 by 17.6667 to adjust your taxable sales.

- Determine your Taxable Sales by subtracting the result of step 7 from the result of step 6.

- Calculate Sales Tax Due by multiplying your taxable sales (from step 8) by 6% (0.06).

- Enter the Use Tax Due, which is 6% (0.06) of all purchases made for your own use or consumption on which you did not previously pay a 6% sales tax.

- Record the total amount of wages paid to employees.

- Calculate and enter Income Tax Withholding Due for all employees.

- If applicable, include any Penalty and Interest Due for late payment.

- Add the amounts from steps 9, 10, and 12, plus any penalties, to determine the total payment due. Enter this in the Pay this Amount line.

- Complete the CERTIFICATION section by providing the seller's signature and date.

- Review the form for completeness and accuracy before mailing it with the payment to the Michigan Department of Treasury at the address provided.

Ensure that you mail the white copy of the form with your payment and keep the yellow copy for your records. Adhering to the post-event deadline of three business days is crucial to avoid potential assessments or penalties. By following these steps carefully, you can fulfill your tax responsibilities to the State of Michigan in a timely and efficient manner, thus ensuring your compliance and enabling a smoother post-event financial closure.

Crucial Points on This Form

What is the Michigan 2271 form?

The Michigan 2271 form is a document issued by the Michigan Department of Treasury for concessionaires to report and pay sales tax. It serves vendors operating in Michigan, ensuring they comply with the state laws regarding the collection and payment of sales, use, and withholding taxes on tangible personal property sold or used within the state at events. This form is pivotal for concessionaires to fulfill their tax responsibilities, including remitting sales tax on retail sales, use tax on goods used in the business, and income tax withholding for employees working in Michigan.

How do I complete the Michigan 2271 form?

Completing the Michigan 2271 form involves several steps:

- Enter the total gross sales of tangible personal property, including both cash and charge sales.

- Indicate your purchases for resale on which you paid a 6% tax to your supplier.

- Calculate the taxable sales by subtracting your taxed purchases (line 2) from your gross sales (line 1).

- If you include tax in your gross sales, adjust the taxable sales amount accordingly.

- Determine the sales tax due by applying the 6% rate to your taxable sales.

- Compute the use tax due on goods used in your business and not previously taxed.

- List the wages paid to employees and calculate the income tax withholding due.

- Add any penalties and interest due for late payment, then total the amounts to find the payable sum.

When is the Michigan 2271 form due?

For the Michigan 2271 form, the due date is inherently prompt—typically within 3 business days following the event you hosted. Failure to submit this form and the corresponding payment to the Michigan Department of Treasury by the specified deadline can lead to an estimated tax assessment issued against the vendor. Thus, timely compliance is crucial to avoid any unnecessary penalties or interest charges.

What are the consequences of not filing the Michigan 2271 form on time?

Not filing the Michigan 2271 form within the required timeframe can result in:

- A penalty of 5% of the tax due, which can increase by an additional 5% for each month or part of a month the payment is overdue, to a maximum of 25%.

- Interest charges on the overdue tax, calculated daily based on the average prime rate plus 1 percent.

- Possible issuance of an estimated tax assessment by the Michigan Department of Treasury.

How is the sales tax calculated on the Michigan 2271 form?

Sales tax calculation, as per the Michigan 2271 form, requires multiplying the taxable sales by the state sales tax rate of 6%. Taxable sales are derived after adjusting gross sales for tax-included pricing and subtracting relevant tax-paid purchases for resale. The tax amount should be computed to the third decimal place, rounded up if the third decimal is over four, or down if four or less, ensuring accuracy in the tax collected and remitted to the treasury.

Where do I mail the completed Michigan 2271 form and payment?

Once filled out, the Michigan 2271 form, along with the corresponding payment, should be mailed to the Michigan Department of Treasury at the following address:

- Michigan Department of Treasury

- Customer Contact - SUW

- P.O. Box 30427

- Lansing, MI 48922

Common mistakes

One common mistake people make when completing the Michigan 2271 form is inaccurately reporting gross sales. It's crucial to include the total amount of tangible personal property sales, encompassing both cash and charge sales. Overlooking certain transactions or not understanding what constitutes gross sales can lead to errors in calculation further down the form.

Another error occurs when individuals fail to properly record their purchases for resale on which they have paid a 6% sales tax. This oversight can result in an incorrect calculation of taxable sales, as these purchases should be subtracted from the gross sales to determine the correct taxable amount. Ensuring accurate reporting here helps to avoid overpaying taxes.

Incorrectly handling the inclusion of tax in gross sales is yet another frequent mistake. If the tax is included in the reported gross sales, there's a specific division required by the form that some might miss or miscalculate. The step involves dividing line 3 by 17.6667 to accurately extract the tax amount included, a critical step for the precise determination of taxable sales.

Many vendors also stumble when calculating the sales tax due. This calculation requires multiplying the taxable sales by 6%. Errors in previous steps or simple mathematical mistakes can lead to inaccurate tax amounts being reported, which may result in penalties or the need to file amended returns.

Identifying purchases that should be reported under use tax due can sometimes be confusing. This section requires vendors to report 6% of purchases for their own use on which no sales tax was paid. Overlooking items or misunderstanding what qualifies can lead subscribers to either over-report or under-report this figure. It's critical to consider all goods taken from inventory or purchased exempt from Michigan sales tax used in the business.

Another common error is related to reporting wages paid to employees and the consequent income tax withholding due. Vendors must ensure all wages paid to employees during the event are reported accurately to calculate the withholding tax correctly. Mistakes here can affect not only tax calculations but also compliance with employment tax regulations.

Perhaps one of the more technical oversights involves failing to correctly compute penalty and interest for late submissions. If the return and payment are not submitted within the prescribed timeframe, additional penalties and interest are due. Misunderstanding the calculation or unawareness of the tight deadline following the event can lead to unexpected fees.

Failing to sign the certification part or providing incomplete identification details including Seller's Name, Telephone Number, Social Security Number or Federal Employer ID Number, can render the submission invalid or incomplete. The Michigan Department of Treasury requires this information for processing and verification purposes.

Underestimating the importance of retaining the copy of the form designated for the vendor's records is also a mistake. Keeping accurate records is essential for financial management and future reference, especially in cases where the submission might be queried or in the event of an audit.

Last but not least, vendors sometimes make the mistake of not consulting with the Sales, Use and Withholding Tax Customer Contact Division if they encounter any uncertainties or questions. Leveraging available resources can prevent many of the mistakes mentioned and ensure compliance with Michigan tax laws.

Documents used along the form

In the realm of business operations within Michigan, particularly for event vendors and concessionaires, the submission of the Michigan Department of Treasury 2271 form for Concessionaire's Sales Tax Return and Payment is just one part of a thorough compliance process. Alongside this form, a variety of additional documents play a critical role in ensuring full adherence to tax regulations. Understanding these documents and their functions is vital for businesses aiming to operate seamlessly and avoid potential legal complications.

- Form 160 - Combined Return for Michigan Taxes: A comprehensive return form used by businesses to report and pay sales tax, use tax, and withholding tax. This form centralizes tax reporting for convenience.

- Form 5080 - Sales, Use and Withholding Taxes Monthly/Quarterly Return: Necessary for businesses to file and remit sales, use, and withholding taxes on a monthly or quarterly basis, depending on their tax liability.

- Form 5094 - Sales, Use and Withholding Taxes Annual Return: Used by businesses to summarize and report the sales, use, and withholding taxes for the entire year.

- Form 165 - Notice of Change or Discontinuance: Businesses must submit this form if they make any changes to their account information or if they discontinue their operations.

- Form 3372 - Michigan Sales and Use Tax Certificate of Exemption: This document allows businesses to purchase goods without paying sales tax, claiming that the goods will be resold or are for exempt purposes.

- Form 446 - Michigan Income Tax Withholding Guide: Provides information on withholding rates and contains the withholding tax tables required to calculate the correct amount of income tax to withhold from employee wages.

- W-9 Form - Request for Taxpayer Identification Number and Certification: Required to gather information from vendors or contractors to report income paid to them during the fiscal year.

- UIA 1028 - Employer's Quarterly Wage/Tax Report: Utilized to report wages paid to employees, this form is necessary for calculating unemployment insurance obligations.

- Form 518 - Registration for Michigan Taxes: Businesses must complete this form to register for sales tax, use tax, and other taxes. It's a preliminary step before conducting business in Michigan.

- Form 4594 - Voluntary Disclosure Request: For businesses that have not complied with tax obligations, this form allows them to voluntarily disclose their tax liabilities in exchange for certain waivers and agreements from the state.

These documents complement the Michigan 2271 form in the tax reporting and payment process, aiding businesses in maintaining compliance with Michigan's dynamic tax laws. Businesses must stay informed and prepared to handle their tax responsibilities efficiently, using these forms as tools to navigate the complexities of Michigan’s tax system. Through diligence and attention to detail, businesses can ensure they meet all their tax obligations, thus maintaining good standing with the Michigan Department of Treasury.

Similar forms

The New York State Sales Tax Return possesses similarities to the Michigan 2271 form, as it is also a document that businesses must submit to declare their collected sales tax from retail sales. Much like the Michigan form, it mandates the reporting of gross sales, taxable sales, and the calculation of sales tax due based on specific tax rates. Furthermore, both forms serve the primary purpose of ensuring that the correct amount of sales tax is collected and remitted to the state government, adhering to the laws governing sales tax collection and remission.

The California Use Tax Return shares a commonality with the 2271 form by requiring businesses to report and remit use tax on items bought for business use without paying state sales tax. Both documents emphasize the responsibility of businesses to accurately account for and pay taxes on goods consumed in the business operation that were not subject to sales tax at the point of purchase, emphasizing the state’s effort to tax goods and services used within its boundaries fairly.

The Florida Annual Resale Certificate for Sales Tax is akin to Michigan's 2271 form in that it involves the process of tax collection and remittance by businesses. However, the Florida form is used specifically for businesses to obtain a certificate that allows them to buy goods for resale without paying sales tax at the point of purchase. Both forms underscore the tax obligations of businesses and the state's role in regulating and enforcing tax collection, while also providing mechanisms for businesses to comply with tax laws efficiently.

The IRS Form 941, Employer’s Quarterly Federal Tax Return, although it concerns federal taxation, relates to the Michigan 2271 form through its requirement for businesses to report and pay taxes collected, in this case, federal withholding taxes, Social Security, and Medicare taxes on behalf of their employees. Similar to the Michigan 2271, Form 941 is key in ensuring that employers fulfill their tax responsibilities, specifically in relation to employee wages and withholdings, highlighting the broader responsibility of businesses in tax collection and remittance.

The Illinois Business Registration Application resonates with aspects of the Michigan 2271 form through its focus on the registration and subsequent tax obligations of businesses operating within the state. Like Michigan’s form, it is a prerequisite for conducting business activities, especially those subject to state tax laws. Both documents are instrumental in the initial and ongoing regulatory compliance of businesses, addressing the collection and remittance of various taxes as mandated by state law.

Dos and Don'ts

When you are tasked with completing the Michigan 2271 form for Concessionaire's Sales Tax Return and Payment, it is crucial to follow specific guidelines to ensure accuracy and compliance with state requirements. Below, find curated insights on what should and shouldn't be done during the process.

Do's:

- Ensure that all the information provided, including gross sales, taxable sales, and deductions, is accurate to prevent any discrepancies.

- Calculate the sales tax due by accurately multiplying the taxable sales by 6% to determine the amount owed to the state.

- Include the total wages paid to employees and accurately calculate the income tax withholding due.

- Use the direct percentage calculation method or the Michigan Income Tax Withholding Table for precise deduction figures.

- Compute penalty and interest correctly if the return or tax payment is delayed beyond three days after the event.

- Sign the certification section to attest to the accuracy and completeness of the information under penalty of perjury.

- Mail the completed form, along with the correct payment, to the Michigan Department of Treasury by the specified deadline.

Don'ts:

- Do not leave any required sections incomplete, as this could result in processing delays or incorrect tax calculations.

- Avoid guessing amounts or making estimations without concrete data to support your figures.

- Do not overlook the necessity to subtract your purchases for resale (on which tax was already paid) from your gross sales to determine taxable sales.

- Avoid including incorrect payment amounts; ensure that all calculations for sales tax, use tax, income tax withholding, penalty, and interest are correct.

- Refrain from missing the filing deadline; submitting your form and payment late can lead to penalties and interest charges.

- Do not forget to keep a copy of the form for your records; maintaining accurate and accessible records is crucial.

- Avoid making the payment to an incorrect payee; make the check payable specifically to the STATE OF MICHIGAN as instructed.

Adhering to these guidelines will help ensure that the form is completed accurately and efficiently, fulfilling your tax obligations without unnecessary complications.

Misconceptions

Understanding the Michigan 2271 form involves navigating through some common misconceptions. It's important to clarify these misunderstandings to ensure compliance and avoid unnecessary penalties. Here are six common misconceptions about the Michigan 2271 form:

- All sales are subject to sales tax: It's a common misconception that every sale at an event in Michigan is subject to sales tax. In reality, only sales of tangible personal property to an end-user are taxable. Sales for resale, where the purchaser plans to sell the item to someone else, are not subject to sales tax if properly documented.

- Use tax applies only to inventory items: Some believe that use tax is charged solely on inventory items taken for personal use. However, use tax also applies to all goods purchased tax-exempt for business use, not just inventory items. This encompasses any item bought without paying Michigan sales tax and used within the business.

- Out-of-state employees are exempt from income tax withholding: There's a misconception that if an employee lives out of state, Michigan income tax withholding does not apply to wages earned while working in Michigan. Regardless of where an employee resides, income earned in Michigan is subject to Michigan income tax withholding.

- The form is due only if demanded by the Treasury: While the form mentions that it's due upon demand or three business days after the event if no demand is made, some might think it's okay to wait for a demand. The correct understanding should be that the form and payment are expected shortly after the event, irrespective of an explicit demand from the Michigan Department of Treasury.

- Penalties are flat: The idea that penalties for late payment are a flat rate is incorrect. Initially, the penalty is 5% of the unpaid tax, which increases by an additional 5% per month or part of a month after the second month, up to a maximum of 25%. Interest also accrues daily, making it important to pay on time.

- Sales tax is always a simple 6% calculation: Though it's true that Michigan imposes a 6% sales tax, calculating the exact tax to remit isn't always straightforward. If tax is included in the gross sales price, one must follow specific calculations to determine the taxable amount. Retailers must also use a rounding formula to compute the tax amount correctly when preparing their sales tax return.

It's crucial for vendors operating in Michigan to understand these nuances of the Michigan 2271 form to ensure they comply with state tax laws. Misunderstandings can lead to errors in tax filing and potentially costly penalties. Always refer to the Michigan Department of Treasury or a tax professional if you're unsure about how to complete the form correctly.

Key takeaways

The Michigan 2271 form is a critical document for vendors operating in Michigan, ensuring compliance with the state's tax collection requirements. This form covers several types of taxes including sales, use, and withholding taxes that are applicable to transactions and employment within Michigan. Below are eight key takeaways to assist in accurately completing and utilizing the form.

- The form must be used by vendors to report and pay sales tax at a 6% rate on all sales of tangible personal property to end users in Michigan.

- Vendors are also responsible for remitting use tax on goods used in their business that were taken from inventory or purchased tax-exempt, unless a sales tax of at least 6% was paid to another state.

- In addition to sales and use taxes, the Michigan 2271 form requires vendors to withhold income tax for employees working in Michigan, irrespective of the employee's state of residence.

- Accuracy is paramount when filling out the form. Sellers should meticulously calculate gross sales, taxable sales, and applicable taxes due, including sales, use, and withholding taxes.

- Penalties and interest are due for late submissions, calculated as a percentage of the tax due and accrued over time. Vendors should strive to submit the form and any payments within three business days post-event to avoid these charges.

- Vendor compliance is affirmed through a certification process, requiring a declaration under penalty of perjury that the information provided on the form is true and complete.

- Payments and completed forms should be directed to the Michigan Department of Treasury by the specified due date to avoid estimated tax assessments that could be levied against the vendor for non-compliance.

- Additional resources, such as the Michigan Income Tax Withholding Guide and detailed instructions on how to calculate withholding taxes and penalties, are available on the Michigan Treasury website.

In summary, the Michigan 2271 form is an essential tool for vendors to ensure adherence to Michigan's tax laws. Proper completion and timely submission of this form, along with the necessary payments, safeguard vendors from penalties and interest charges. This adherence supports the operational integrity of businesses within Michigan, contributing to a fair and equitable tax system.

Popular PDF Templates

Request and Order to Seize Property Michigan - It mandates law enforcement to endorse the form with the date and time of order receipt for procedural integrity.

Michigan Real Estate Forms - Utilize this document for claiming refunds on transfers involving mineral rights and interests, emphasizing the unique nature of such property.