Michigan 2196 PDF Form

In the state of Michigan, retailers and dealers who are part of the beverage sale ecosystem have the opportunity to receive compensation for handling the return of empty beverage containers. This process is governed by the Michigan Department of Treasury through Form 2196, a crucial document designed to streamline the reimbursement process from the Bottle Deposit Fund. The origin of this practice goes back to Public Act 148 of 1989, which was set up to ensure that businesses recoup some costs associated with managing these empty returnable containers. Not only does this act encourage recycling and proper waste management, but it also creates a financial incentive for retailers and dealers by allowing them to claim compensation for each container handled. The initiation of the reimbursement process requires thorough documentation and adherence to the guidelines provided by the Michigan Department of Treasury, which include reporting the actual number of containers handled in a given year without estimating or adjusting their value. Furthermore, the form elaborates that compensation will only be provided if the reported figures are backed by credible sources such as invoices or cash register receipts. Significantly, this form ties into the larger legislative framework that emphasizes environmental stewardship through the incentivization of bottle returns. It presents a fascinating intersection of environmental policy, business economics, and state governance, making the Form 2196 not just a procedural document but a testament to Michigan’s ongoing efforts to balance economic activity with ecological responsibility.

Preview - Michigan 2196 Form

Michigan Department of Treasury |

Report Year |

|

2196 (Rev. |

||

2012 |

||

|

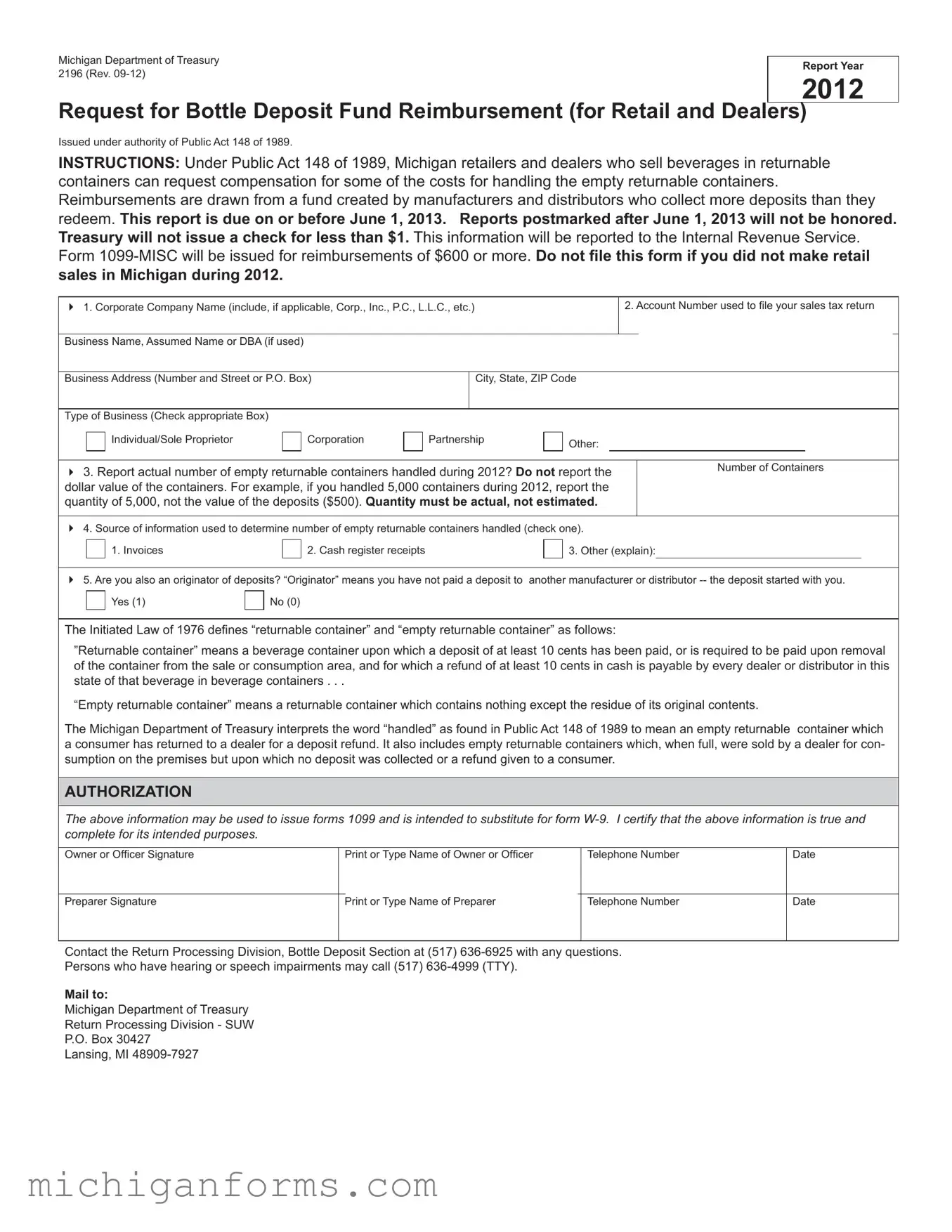

Request for Bottle Deposit Fund Reimbursement (for Retail and Dealers)

Issued under authority of Public Act 148 of 1989.

INSTRUCTIONS: Under Public Act 148 of 1989, Michigan retailers and dealers who sell beverages in returnable containers can request compensation for some of the costs for handling the empty returnable containers. Reimbursements are drawn from a fund created by manufacturers and distributors who collect more deposits than they redeem. This report is due on or before June 1, 2013. Reports postmarked after June 1, 2013 will not be honored. Treasury will not issue a check for less than $1. This information will be reported to the Internal Revenue Service. Form

1. Corporate Company Name (include, if applicable, Corp., Inc., P.C., L.L.C., etc.) |

|

|

|

|

2. Account Number used to fi le your sales tax return |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business Name, Assumed Name or DBA (if used) |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Business Address (Number and Street or P.O. Box) |

|

City, State, ZIP Code |

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Type of Business (Check appropriate Box) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

Individual/Sole Proprietor |

|

|

Corporation |

|

|

Partnership |

|

|

Other: |

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. Report actual number of empty returnable containers handled during 2012? Do not report the |

|

|

Number of Containers |

||||||||||||||||||

|

|

|

|

|

|

||||||||||||||||

dollar value of the containers. For example, if you handled 5,000 containers during 2012, report the |

|

|

|

|

|

|

|||||||||||||||

quantity of 5,000, not the value of the deposits ($500). Quantity must be actual, not estimated. |

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

4. Source of information used to determine number of empty returnable containers handled (check one). |

|

|

|

|

|

|

|||||||||||||||

|

|

1. Invoices |

|

|

2. Cash register receipts |

|

|

|

|

3. Other (explain): |

|

|

|||||||||

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

||||||||||||||||

5. Are you also an originator of deposits? “Originator” means you have not paid a deposit to |

another manufacturer or distributor |

||||||||||||||||||||

|

|

Yes (1) |

|

|

No (0) |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

The Initiated Law of 1976 defi nes “returnable container” and “empty returnable container” as follows:

”Returnable container” means a beverage container upon which a deposit of at least 10 cents has been paid, or is required to be paid upon removal of the container from the sale or consumption area, and for which a refund of at least 10 cents in cash is payable by every dealer or distributor in this state of that beverage in beverage containers . . .

“Empty returnable container” means a returnable container which contains nothing except the residue of its original contents.

The Michigan Department of Treasury interprets the word “handled” as found in Public Act 148 of 1989 to mean an empty returnable container which a consumer has returned to a dealer for a deposit refund. It also includes empty returnable containers which, when full, were sold by a dealer for con- sumption on the premises but upon which no deposit was collected or a refund given to a consumer.

AUTHORIZATION

The above information may be used to issue forms 1099 and is intended to substitute for form

Owner or Offi cer Signature |

|

Print or Type Name of Owner or Officer |

|

Telephone Number |

Date |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preparer Signature |

|

Print or Type Name of Preparer |

|

Telephone Number |

Date |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Contact the Return Processing Division, Bottle Deposit Section at (517)

Persons who have hearing or speech impairments may call (517)

Mail to:

Michigan Department of Treasury

Return Processing Division - SUW

P.O. Box 30427

Lansing, MI

Bottle Deposit Fund Reimbursement Availability

INSTRUCTIONS: Under Public Act 148 of 1989, Michigan retailers and dealers who sell beverages in returnable containers can request compensation for some of the costs for handling the empty returnable containers.

Reimbursements are drawn from a fund created by manufacturers and distributors who collect more deposits than they redeem.

The payment is based on the number of empty returnable containers handled in a calendar year. Payment amounts will be known after Treasury determines how much money is available.

To apply, you must complete and mail a Request for Bottle Deposit Fund Reimbursement (Form 2196) to Treasury. Form 2196 is due on or before June 1, 2013. Use Form 2196 or contact Return Processing Division, Bottle Deposit Section, at (517)

Treasury will begin issuing checks after August 1.

Form Characteristics

| Fact Number | Description |

|---|---|

| 1 | The Michigan Department of Treasury issued Form 2196 under the authority of Public Act 148 of 1989. |

| 2 | This form is a request for Bottle Deposit Fund Reimbursement targeted at retailers and dealers in Michigan. |

| 3 | Eligible businesses must sell beverages in returnable containers to qualify for this reimbursement. |

| 4 | Reimbursable funds originate from a pool created by manufacturers and distributors who collect more in deposits than they pay out in refunds. |

| 5 | The submission deadline for Form 2196 was on or before June 1, 2013, for the report year 2012. |

| 6 | Treasury will not issue checks for amounts less than $1, and Form 1099-MISC will be issued for reimbursements of $600 or more. |

| 7 | Retrieved information is reported to the Internal Revenue Service, aiming to substitute the need for form W-9. |

| 8 | Retailers are instructed to report the actual number of empty returnable containers handled, not the dollar value of the deposits. |

| 9 | Questions regarding the process or form can be directed to the Return Processing Division, Bottle Deposit Section at the provided phone numbers. |

Guidelines on Utilizing Michigan 2196

Filling out the Michigan 2196 form is a necessary step for retailers and dealers in Michigan who are seeking reimbursement for handling empty returnable containers. This process involves reporting the actual number of containers managed throughout the year, a requirement set by the Michigan Department of Treasury under Public Act 148 of 1989. Upon completion, the form should be mailed to the specific address provided by the Department of Treasury before the deadline to qualify for reimbursement. Below are the step-by-step instructions to accurately complete and submit the form.

- Enter the Corporate Company Name including any applicable suffixes (Corp., Inc., P.C., L.L.C., etc.) if applicable.

- Provide the Account Number you use for filing your sales tax return.

- List the Business Name, Assumed Name or DBA (Doing Business As) if used.

- Fill in the Business Address, including the number and street or P.O. Box.

- Enter the City, State, and ZIP Code for your business location.

- Select the Type of Business by checking the appropriate box: Individual/Sole Proprietor, Corporation, Partnership, or Other (with an explanation).

- Report the actual number of empty returnable containers handled during the year 2012. Mention only the quantity, without referring to their dollar value.

- Indicate the source of information used to determine the number of empty returnable containers handled by checking the appropriate box: Invoices, Cash register receipts, or Other (with an explanation required).

- Respond Yes or No to the question, "Are you also an originator of deposits?"

- The owner or officer of the company must sign the form to certify that the information provided is true and complete. Include the printed name of the owner or officer, their telephone number, and the date.

- A space is provided for the preparer's signature, printed name, and telephone number, if someone other than the owner or officer prepared the form.

Once the form is complete, mail it to the Michigan Department of Treasury Return Processing Division - SUW, P.O. Box 30427, Lansing, MI 48909-7927. It is important to adhere to the submission deadline on or before June 1, 2013, to ensure eligibility for reimbursement. Reports postmarked after this date will not be honored. The Treasury Department will start issuing checks for qualified submissions after August 1. For any questions or additional assistance, contact the Return Processing Division, Bottle Deposit Section, at the provided telephone numbers.

Crucial Points on This Form

What is the Michigan 2196 form?

The Michigan 2196 form, officially known as the Request for Bottle Deposit Fund Reimbursement, is a document that Michigan retailers and dealers fill out to seek compensation for expenses related to handling empty returnable beverage containers. This form is part of a system established under Public Act 148 of 1989, which aims to reimburse those who have incurred costs from managing these containers.

Who is eligible to file the Michigan 2196 form?

Eligibility for filing the Michigan 2196 form extends to retailers and dealers in Michigan who sell beverages in returnable containers. These entities can apply for reimbursement for the costs associated with collecting, sorting, and handling the empty containers returned by consumers.

What is the deadline for submitting the Michigan 2196 form?

The Michigan 2196 form must be submitted on or before June 1 of the year following the report year. For instance, for activities conducted in 2012, the form would be due on or before June 1, 2013. It's important to meet this deadline as late submissions will not be honored.

What type of reimbursement does the Michigan 2196 form provide?

Reimbursement under the Michigan 2196 form is derived from a fund created by manufacturers and distributors. It compensates retailers and dealers for some of the costs incurred in handling empty returnable containers. The exact amount of reimbursement depends on how much money is available in the fund and the number of empty containers handled.

How is the quantity of empty returnable containers reported?

When completing the Michigan 2196 form, retailers and dealers should report the actual number of empty returnable containers they handled during the report year. It's crucial to report the quantity of containers, not their dollar value. Accuracy is key, as estimates are not accepted.

What sources of information can be used to determine the number of containers?

In determining the number of empty returnable containers handled, retailers and dealers can rely on several sources of information, including:

- Invoices

- Cash register receipts

- Other relevant documentation, provided they offer a clear and true record of the containers handled.

Can someone file the Michigan 2196 form if they did not make retail sales in Michigan during the report year?

No, if no retail sales were made in Michigan during the report year, the entity is not eligible to file the Michigan 2196 form. The form is specifically designed for those who have engaged in selling beverages in returnable containers and handled the empty containers thereafter.

What is the minimum reimbursement amount for the Michigan 2196 form?

The Michigan Department of Treasury will not issue a reimbursement check for amounts less than $1. This minimum amount ensures that the process remains efficient and cost-effective for both the department and applicants.

Is information reported on the Michigan 2196 form shared with the IRS?

Yes, the information provided on the Michigan 2196 form will be reported to the Internal Revenue Service (IRS). For reimbursements of $600 or more, a Form 1099-MISC will be issued. This procedure underlines the importance of providing accurate and truthful information.

How can someone get more information or assistance with the Michigan 2196 form?

For more information or assistance with the Michigan 2196 form, retailers and dealers can contact the Return Processing Division, Bottle Deposit Section, at (517) 636-6925. Individuals with hearing or speech impairments can reach out via (517) 636-4999 (TTY). These contact options ensure that support is available for all applicants navigating the reimbursement process.

Common mistakes

One of the common mistakes when filling out the Michigan 2196 form is not accurately reporting the actual number of empty returnable containers handled during the specified year. Applicants should provide the exact quantity of containers, rather than the monetary value of the deposits. Providing an estimated number instead of the actual count can lead to discrepancies and may affect the reimbursement amount.

Another error often encountered is submitting the form past the due date. The form clearly states that it must be postmarked on or before June 1, 2013, to be considered valid. Late submissions result in the application not being honored, thus it’s crucial for applicants to adhere to this deadline to ensure they are eligible for reimbursement.

Applicants frequently overlook the importance of specifying the type of business in the application process. The form offers options such as Individual/Sole Proprietor, Corporation, Partnership among others. Failing to check the appropriate box may lead to processing delays as this information is critical in determining eligibility and proper categorization for the fund reimbursement.

Incorrect or incomplete business information, such as the Corporate Company Name, Business Address, and Account Number, is another common mistake. It is essential that this information aligns with the details used to file sales tax returns. Any discrepancies can complicate the validation process and potentially prevent reimbursement.

There is also a section that inquires whether the applicant is also an originator of deposits, requiring a simple "Yes" or "No" answer. Misunderstanding this question or providing an incorrect response can affect the reimbursement outcome. Applicants need to accurately assess and verify their role within the deposit cycle to answer correctly.

A final mistake is not properly authorizing the form by omitting the signature of the Owner or Officer and, if applicable, the Preparer. This form serves as a formal request and requires official authorization to process. Unsigned or improperly authorized documents are not accepted and will not be processed for reimbursement, emphasizing the need for careful review and completion.

Documents used along the form

When dealing with the Michigan Department of Treasury, especially for reimbursements regarding bottle deposits, a variety of forms and documents might be necessary in addition to the main Form 2196. These documents ensure that the process is thorough, covering all requirements for a successful submission. They play a vital role in verifying the information provided, ensuring compliance with regulations, and facilitating a smoother transaction with the Department of Treasury.

- Form 165 - Notice of Change or Discontinuance: If there have been any changes to the business details or if the business is discontinuing operations, this form must be submitted. It ensures that the Department of Treasury has the most current information about the business.

- Form 5081 - Sales, Use and Withholding Taxes Annual Return: This document is crucial for businesses in Michigan as it reports the sales, use, and withholding taxes over the year. It often accompanies requests like Form 2196 when detailing financial activities relating to sales.

- Form 160 - Combined Return for Michigan Taxes: This form is a summary of tax payments, including sales tax, which might be relevant for retailers seeking reimbursement through Form 2196. The included details help in cross-verifying the validity of the claims made on the reimbursement request.

- Form 1099-MISC: Although this form is issued by the Department of Treasury for reimbursements of $600 or more, it plays a crucial role for the recipient. It needs to be included in tax documentation for the year received, ensuring that all income is accurately reported to the IRS.

- Business Registration Documents: While not a specific form, maintaining updated business registration documents is essential. These documents prove the legitimacy of the business and its operations in Michigan, supporting documentation for Form 2196 submissions.

In conclusion, preparing a Request for Bottle Deposit Fund Reimbursement requires more than just completing Form 2196. A thoughtful compilation of supporting documents and forms like the Notice of Change or Discontinuance, Annual Sales Tax Returns, Combined Returns for Michigan Taxes, Form 1099-MISC, and updated Business Registration Documents ensure a smooth process. Each document has its role in validating the information submitted, adhering to tax regulations, and ultimately supporting the reimbursement request from the Michigan Department of Treasury.

Similar forms

The Michigan Form BC-1040, City Income Tax Return, shares similarities with the Form 2196 in that both require specific business information, such as the official business name, address, and type of business entity. These forms are utilized by entities operating within Michigan to report and potentially remit taxes or fees related to their business operations.

Form 165, Annual Return for Sales, Use and Withholding Taxes, is another document bearing resemblance to Form 2196. Similar to the 2196 form, Form 165 requires businesses to report numerical data related to financial transactions—in the case of Form 165, sales, use, and withholding tax information. Both forms necessitate accuracy in the reporting of quantities, be they the number of returnable containers or financial transactions, to calculate potential reimbursements or tax obligations.

The Unemployment Insurance Agency (UIA) 1028, Employer's Quarterly Wage/Tax Report, parallels Form 2196 through its requirement for detailed reporting of operational data. While UIA 1028 focuses on wages paid and taxes owed for employment, Form 2196 collects data on handled returnable containers. Each form serves as a mechanism for businesses to report specific types of operational data to state authorities.

Form 5094, Sales, Use and Withholding Taxes Monthly/Quarterly Return, is akin to Form 2196 as both require the provision of a tax-related account number and detailed transaction information for a given period. They are used to calculate dues to the state—whether for bottle deposit fund reimbursement or sales, use, and withholding taxes—based on reported activities.

Dos and Don'ts

Filling out the Michigan 2196 form, a Request for Bottle Deposit Fund Reimbursement, requires attention to detail and an understanding of specific guidelines. Here are key dos and don'ts to consider:

- Do ensure that you are eligible to file this form. Only Michigan retailers and dealers who have made retail sales in Michigan during the reporting year are eligible.

- Do not forget to file before the deadline. The form is due on or before June 1 of the following year. Late submissions will not be honored, so mark your calendar!

- Do report the actual number of empty returnable containers handled during the year. Estimations are not allowed; accuracy is key.

- Do not report the dollar value of the containers. The form specifically asks for the quantity of containers, not their monetary value.

- Do choose the correct source of information for determining the number of containers handled. Whether it's invoices, cash register receipts, or another method, select the one that accurately reflects your count.

- Do not file this form if you did not make any retail sales in Michigan during the report year. It is not applicable to retailers and dealers without sales in the stated period.

- Do indicate whether you are also an originator of deposits. This information is critical for the processing of your reimbursement request.

- Do not overlook the authorization section at the bottom of the form. This part requires careful reading and the appropriate signatures, certifying that the information provided is true and complete.

- Do remember that reimbursements are drawn from a specific fund and payments are based on available funds. It's important to manage expectations regarding the amount you may receive.

Adhering to these dos and don'ts helps ensure a smooth and successful request for reimbursement under Michigan's Bottle Deposit Fund Reimbursement program. Always double-check your details, submit on time, and keep accurate records for future reference.

Misconceptions

Understanding the complexities of the Michigan Department of Treasury’s Form 2196 can sometimes be challenging, leading to common misconceptions. Clarifying these misconceptions is essential for retailers and dealers seeking reimbursement for handling empty returnable containers as outlined under Public Act 148 of 1989. Here are five common misconceptions:

- Form 2196 is only for large businesses: This misconception might lead small business owners to believe they are ineligible for reimbursement. In reality, Form 2196 is designed for all Michigan retailers and dealers, regardless of size, who sell beverages in returnable containers and incur costs for handling these empty containers.

- Estimates can be used for reporting containers: The form clearly requires the reporting of actual numbers of empty returnable containers handled during the reporting period, not estimates. This ensures that reimbursement calculations are based on precise data, reflecting the actual burden handled by the retailer or dealer.

- Form 2196 is optional: While not every retailer or dealer may find it beneficial or necessary to file this form, the opportunity for reimbursement can offer significant financial relief for those who do. Viewing the form as optional overlooks the potential benefits it can provide in compensating for the costs involved in handling returnable containers.

- The reimbursement amount is predetermined: Some may assume that there is a set amount or rate for reimbursement. However, the actual reimbursement amount is determined after the Michigan Department of Treasury assesses the total funds available and the total number of containers handled by all applicants. This means the specific reimbursement amount varies year by year.

- Only physical submissions of Form 2196 are accepted: Given the digital age, this could be a natural assumption. However, the clear instructions for mailing the form to the Michigan Department of Treasury's Return Processing Division highlight a physical submission requirement. Retailers and dealers should ensure they comply with this to participate in the reimbursement program properly.

By addressing these misconceptions, retailers and dealers can better understand and navigate the process of obtaining reimbursements for the costs associated with handling returnable containers. Accurate knowledge and compliance with the submission guidelines are crucial steps towards benefiting from this program.

Key takeaways

Understanding the Michigan 2196 form is crucial for retailers and dealers who deal with returnable beverage containers. The form allows them to claim reimbursement for the costs associated with handling these containers, a unique opportunity provided by Michigan law. Here are five key takeaways to ensure proper completion and maximization of the benefits offered by this form:

- Eligibility and Purpose: The Michigan Department of Treasury issues the Form 2196 under Public Act 148 of 1989. It specifically targets Michigan retailers and dealers selling beverages in returnable containers, offering them a way to recover some costs incurred in handling these containers. This reimbursement comes from a specialized fund supported by the surplus from manufacturers and distributors who collect more in deposits than they pay out. This initiative not only eases the financial burden on retailers and dealers but also encourages the recycling of beverage containers.

- Deadline for Submission: It's important to mark your calendar for June 1, 2013, as the due date for submitting the Form 2196. Submissions postmarked after this date will not be considered. Timely submission is critical to take advantage of this reimbursement opportunity. The structured timeline ensures the orderly processing of requests and distribution of funds.

- Reimbursement Criteria: When filling out the form, retailers and dealers must report the actual number of empty returnable containers handled during the previous year, without estimating or noting the dollar value of these containers. The form emphasizes the importance of accurate, verifiable counts, using sources such as invoices or cash register receipts, to determine the number of containers. This precision is crucial for the fair distribution of the reimbursement funds.

- Tax Reporting: For reimbursements totaling $600 or more, the Michigan Department of Treasury will issue a Form 1099-MISC. This requirement underscores the taxable nature of the reimbursement and the need for recipients to consider this income in their tax planning. It reflects the intersection of environmental policy with federal tax regulations, highlighting the broader implications of the reimbursement for businesses.

- Support and Assistance: The Michigan Department of Treasury provides dedicated support for questions or concerns regarding the Form 2196. Retailers and dealers can contact the Return Processing Division, Bottle Deposit Section, for assistance. This support is an essential resource, ensuring that applicants can navigate the process smoothly and maximize their potential reimbursement. Additionally, services are available for individuals with hearing or speech impairments, ensuring that all eligible participants have the opportunity to apply.

In summary, the Form 2196 represents a targeted support measure for Michigan businesses in the beverage sales sector. By carefully adhering to the submission instructions, accurately reporting container counts, and leveraging available assistance, retailers and dealers can effectively manage the reimbursement process. This initiative not only compensates businesses for their recycling efforts but also promotes environmental sustainability through the incentivization of container return.

Popular PDF Templates

State of Michigan Tax Forms 2022 - Applications will not proceed without settlement of delinquent IFTA returns and dues, aligning with compliance stipulations on the 2823 form.

Michigan Workers Independent Contractor Worksheet - It underscores the evolution of the residual market's policies towards a more stringent classification of independent contractors.