Michigan 151 PDF Form

When residents or businesses in Michigan face tax, benefit, or debt matters with the state and prefer not to handle these issues personally, the Michigan Department of Treasury and the Bureau of Workers' & Unemployment Compensation (BW&UC) provide a solution through the Power of Attorney Authorization, known as Form 151. This form enables individuals, corporations, and other entities to appoint a representative—whether an organization, firm, or individual—to manage their state tax, benefit, or debt matters on their behalf. The form outlines a clear structure including taxpayer and representative information, the scope of authorization, and instructions on how to effectively assign or revoke powers of attorney. It also delves into specifics like the periods of representation, types of authorization (either general or limited), and the necessary steps to change or revoke previously granted authorizations. Form 151 is essential for those seeking to ensure their tax and legal matters are handled efficiently without their direct involvement, yet it requires careful completion to accurately reflect the taxpayer's intentions. Such a comprehensive tool is invaluable for managing interactions with Michigan's tax and unemployment authorities, illustrating a crucial aspect of state-level legal and financial administration.

Preview - Michigan 151 Form

Michigan Department of Treasury and Bureau of Workers' & Unemployment Compensation (BW&UC) 151 (Rev.

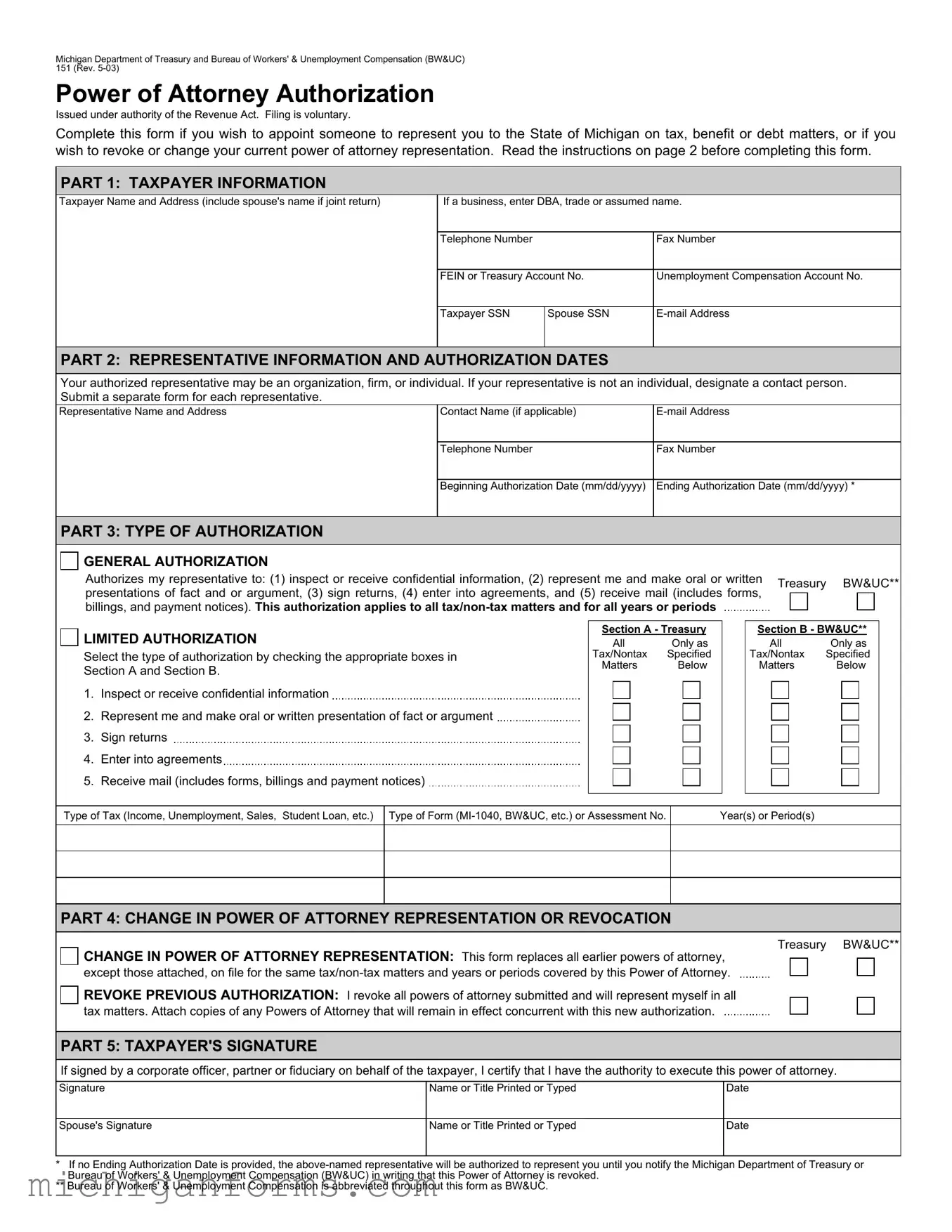

Power of Attorney Authorization

Issued under authority of the Revenue Act. Filing is voluntary.

Complete this form if you wish to appoint someone to represent you to the State of Michigan on tax, benefit or debt matters, or if you wish to revoke or change your current power of attorney representation. Read the instructions on page 2 before completing this form.

PART 1: TAXPAYER INFORMATION

Taxpayer Name and Address (include spouse's name if joint return) |

If a business, enter DBA, trade or assumed name. |

||

|

|

|

|

|

Telephone Number |

|

Fax Number |

|

|

|

|

|

FEIN or Treasury Account No. |

Unemployment Compensation Account No. |

|

|

|

|

|

|

Taxpayer SSN |

Spouse SSN |

|

|

|

|

|

PART 2: REPRESENTATIVE INFORMATION AND AUTHORIZATION DATES

Your authorized representative may be an organization, firm, or individual. If your representative is not an individual, designate a contact person. Submit a separate form for each representative.

Representative Name and Address |

Contact Name (if applicable) |

|

|

|

|

|

Telephone Number |

Fax Number |

|

|

|

|

Beginning Authorization Date (mm/dd/yyyy) |

Ending Authorization Date (mm/dd/yyyy) * |

|

|

|

PART 3: TYPE OF AUTHORIZATION

GENERAL AUTHORIZATION

Authorizes my representative to: (1) inspect or receive confidential information, (2) represent me and make oral or written Treasury BW&UC** presentations of fact and or argument, (3) sign returns, (4) enter into agreements, and (5) receive mail (includes forms,

billings, and payment notices). This authorization applies to all

|

|

LIMITED AUTHORIZATION |

Section A - Treasury |

|

Section B - BW&UC** |

|

||||||||||||||

|

|

|

|

|||||||||||||||||

|

|

|

All |

|

Only as |

|

All |

Only as |

|

|||||||||||

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

Select the type of authorization by checking the appropriate boxes in |

Tax/Nontax |

Specified |

|

Tax/Nontax |

Specified |

|

||||||||||||

|

|

Section A and Section B. |

Matters |

|

Below |

|

Matters |

Below |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

1. |

Inspect or receive confidential information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

2. |

Represent me and make oral or written presentation of fact or argument |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

3. |

Sign returns |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

4. |

Enter into agreements |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

5. |

Receive mail (includes forms, billings and payment notices) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Type of Tax (Income, Unemployment, Sales, Student Loan, etc.) |

Type of Form |

No. |

|

|

|

|

Year(s) or Period(s) |

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PART 4: CHANGE IN POWER OF ATTORNEY REPRESENTATION OR REVOCATION

Treasury BW&UC**

CHANGE IN POWER OF ATTORNEY REPRESENTATION: This form replaces all earlier powers of attorney, except those attached, on file for the same

REVOKE PREVIOUS AUTHORIZATION: I revoke all powers of attorney submitted and will represent myself in all tax matters. Attach copies of any Powers of Attorney that will remain in effect concurrent with this new authorization.

REVOKE PREVIOUS AUTHORIZATION: I revoke all powers of attorney submitted and will represent myself in all tax matters. Attach copies of any Powers of Attorney that will remain in effect concurrent with this new authorization.

PART 5: TAXPAYER'S SIGNATURE

If signed by a corporate officer, partner or fiduciary on behalf of the taxpayer, I certify that I have the authority to execute this power of attorney.

Signature |

Name or Title Printed or Typed |

Date |

|

|

|

Spouse's Signature |

Name or Title Printed or Typed |

Date |

|

|

|

*If no Ending Authorization Date is provided, the

** Bureau of Workers' & Unemployment Compensation is abbreviated throughout this form as BW&UC.

Instructions for Power of Attorney Authorization (Form 151)

Complete and file a Power of Attorney Authorization (Form 151) if you wish to appoint an individual, firm, or organization as your representative in tax or debt matters before the State of Michigan. Failure to complete this form will prohibit Treasury or the Bureau of Workers’ & Unemployment Compensation (BW&UC) from discussing or releasing your tax return/tax return information with or to another person including your spouse.

PART 1: TAXPAYER INFORMATION

Enter the taxpayer’s name, address, telephone number, fax number, and

PART 2: REPRESENTATIVE INFORMATION AND AUTHORIZATION DATES

You must submit a separate form for each representative. Enter the authorized representative’s telephone number, fax number, and

PART 3: TYPE OF AUTHORIZATION

Check the GeneralAuthorization box to allow your representative to act on your behalf to do all of the following: (1) inspect and receive confidential information, (2) represent you and make oral or written presentations of act and/or argument, (3) sign returns,

(4)enter into agreements, and (5) receive all (includes forms, billings, and payment notices. This authorization applies to all

You may restrict your representative’s authorization to act on your behalf by checking the Limited Authorization box, and checking the appropriate boxes in Section A and/or B. To limit the authorization for specific tax matters, check the appropriate “Only as Specified Below” boxes, and indicate the type of tax, type of form, and years/periods for which you are granting authorization in the space provided.

Check this box if your representative is authorized to:

1.Inspect or receive confidential information

2.Represent you and make oral or written presentation of fact or argument.

3.Sign tax returns.

4.Enter into agreements (such as payment plans).

5.Receive mail.

PART 4: CHANGE IN POWER OF ATTORNEY REPRESENTATION OR REVOCATION

Unless otherwise specified, this Power of Attorney Authorization replaces or revokes any previous power of attorney authorizations on file with the Michigan Department of Treasury or the Bureau of Worker’s & Unemployment Compensation for the same tax matters identified on this form.

You must identify any previous authorizations that are to remain in effect, and attach a copy of the authorizations to this form when filed.

PART 5: TAXPAYER SIGNATURE

You and your spouse, if a joint return, must sign and date the form.

FILING

Except as noted below, mail this form to the Registration Section. Treasury will forward your form to BW&UC.

Customer Contact Center

Registration Section

Michigan Department of Treasury

P.O. Box 30477

Lansing, MI

If the Michigan Accounts Receivable Collection System (MARCS) has requested you to file this form, mail your completed form and any attachments to:

MARCS

P.O. Box 30158

Lansing, MI

If a district office representative has requested you to file this form, mail it to that representative.

If the Treasury Collection Division has requested you to file this form, mail it to:

Collection Division

Michigan Department of Treasury

P.O. Box 30199

Lansing, MI 48909

If BW&UC has asked you to file this form, mail it to:

BW&UC Tax Office

P.O. Box 8068

Royal Oak, MI

Or fax to:

If you are an individual taxpayer (not representing a business), mail this form to:

Customer Contact Center Individual Correspondence Section Michigan Department of Treasury Lansing, MI 48922

Form Characteristics

| Fact Name | Detail |

|---|---|

| Form Identification | Michigan Department of Treasury and Bureau of Workers' & Unemployment Compensation (BW&UC) 151 (Rev. 5-03) |

| Purpose | Power of Attorney Authorization |

| Authority | Issued under the authority of the Revenue Act |

| Voluntariness of Filing | Filing is voluntary |

| Who Should Complete | Anyone wishing to appoint a representative for tax, benefit, or debt matters with the State of Michigan or to change/revoke current representation |

| Instructions | Provided on page 2 of the form |

| Part 1 | Taxpayer Information including personal, business (if applicable), and contact details |

| Part 2 | Representative Information and Authorization Dates, requiring separate form for each representative |

| Part 3 | Type of Authorization - General or Limited, specifying the scope of the representative's authority |

| Part 4 | Changes in Power of Attorney Representation or Revocation, indicating an update or cancellation of previous authorizations |

| Part 5 | Taxpayer's Signature, affirming the information and choices made in the form |

| Filing Directions | Instructions for where and how to file, dependent on the specific department or section addressing the taxpayer's matters |

Guidelines on Utilizing Michigan 151

When it's necessary to allow someone else to handle your tax or debt matters with the State of Michigan, submitting the Michigan 151 form is crucial. This document, also known as the Power of Attorney Authorization, sets the stage for a designated representative to legally act on your behalf in discussions or negotiations with the Michigan Department of Treasury and the Bureau of Workers' & Unemployment Compensation (BW&UC). Completing this form properly is essential for a smooth process. Below are the defined steps to fill out the Michigan 151 form accurately.

- Start with PART 1: TAXPAYER INFORMATION. Fill in your name, address, and if applicable, include your spouse's name for a joint return. Businesses should insert their DBA, trade, or assumed name. Provide your telephone and fax numbers, email address (if available), Social Security number(s), Federal Employer Identification Number (FEIN), or Treasury Account Number. State unemployment matters require entering the Unemployment Compensation Account No.

- Move to PART 2: REPRESENTATIVE INFORMATION AND AUTHORIZATION DATES. Each representative requires a separate form. Insert the representative's name, address, and if it's not an individual, the name of the contact person. Add their telephone and fax numbers, along with an email address. Specify the period for which this authorization is effective by mentioning the start and end dates.

- In PART 3: TYPE OF AUTHORIZATION, determine the extent of the authorization. By checking the General Authorization box, you permit your representative to handle a broad range of actions on your behalf. For more specific limitations, opt for Limited Authorization, detailing the specifics like type of tax, type of form, and the applicable years or periods.

- PART 4: CHANGE IN POWER OF ATTORNEY REPRESENTATION OR REVOCATION is where you indicate if this form is replacing or revoking any previous power of attorney submissions. If you are retaining any previously granted powers, attach copies of those forms.

- PART 5: TAXPAYER'S SIGNATURE requires your signature and, if filing jointly, your spouse's signature along with the date. Corporate officers, partners, or fiduciaries should state their title next to the signature confirming their authority to submit this form.

Once the form is filled out, you must send it to the appropriate address based on your specific situation. The Michigan Department of Treasury or the Bureau of Workers' & Unemployment Compensation (BW&UC) classify where to mail or fax your form based on various factors like individual taxpayer status or specific requests from MARCS, district office representatives, or the Treasury Collection Division. Ensuring your form reaches the correct department is pivotal for a timely and effective processing of your Power of Attorney Authorization.

Crucial Points on This Form

What is the Michigan 151 form used for?

The Michigan 151 form, also known as the Power of Attorney Authorization, is used to appoint someone to represent you in matters related to taxes, benefits, or debts with the State of Michigan. It can also be used to revoke or change a current power of attorney representation.

Who can be appointed as a representative on the Michigan 151 form?

On the Michigan 151 form, you can appoint an organization, firm, or individual as your representative. If the representative is not an individual, you must designate a specific contact person within that organization or firm.

Is filing the Michigan 151 form mandatory?

Filing the Michigan 151 form is voluntary. However, not completing this form will prevent the Treasury or the Bureau of Workers’ & Unemployment Compensation from discussing or releasing your tax return or tax information to anyone else, including your spouse.

What information is required on the Michigan 151 form?

The following information is required when completing the Michigan 151 form:

- Taxpayer information including name, address, telephone number, fax number, and email address.

- Representative’s information including name, address, contact name (if applicable), telephone number, fax number, and email address.

- Type of authorization being granted - General or Limited.

- Details on the change in power of attorney representation or revocation, if applicable.

How can I specify the authorization type on the form?

There are two types of authorization you can specify on the form:

- General Authorization allows the representative to perform a wide range of activities on your behalf, including inspecting/receiving confidential information, making representations, signing returns, entering into agreements, and receiving mail related to tax matters.

- Limited Authorization restricts the representative’s activities to specific tax matters, forms, or years you specify on the form.

What happens if I don’t provide an ending authorization date?

If no ending authorization date is provided, your representative will continue to be authorized until you notify the Michigan Department of Treasury or the Bureau of Workers' & Unemployment Compensation in writing that you wish to revoke the Power of Attorney.

Can the Michigan 151 form replace previous powers of attorney?

Yes, unless otherwise specified, filing the Michigan 151 form will replace any previous powers of attorney on file for the same tax/non-tax matters and years or periods covered. If you wish any previous authorizations to remain in effect, you need to attach a copy of those authorizations to this form.

Who needs to sign the Michigan 151 form?

The taxpayer, and the spouse if it's a joint matter, must sign and date the form. If signed by a corporate officer, partner, or fiduciary on behalf of the taxpayer, it certifies that the person signing has the authority to execute this power of attorney.

Where do I mail the completed Michigan 151 form?

Where you mail the completed form depends on who has requested you to file it. Generally, it is mailed to the Registration Section at the Michigan Department of Treasury. If requested by specific departments like MARCS or a Treasury district office, you should mail it to their respective addresses which are detailed in the form instructions.

Common mistakes

Filling out the Michigan 151 form requires attention to detail and a clear understanding of the instructions provided. A common mistake is incorrectly entering taxpayer information in Part 1. Mistakes here can range from providing an outdated address to misspelling names or entering incorrect Social Security Numbers or Federal Employer Identification Numbers. Such errors can lead to processing delays and miscommunication regarding tax, benefit, or debt matters with the Michigan Department of Treasury and Bureau of Workers' & Unemployment Compensation (BW&UC).

In Part 2, where representative information and authorization dates are filled out, it’s often seen that applicants neglect to provide complete details of their representative, including their e-mail address and fax number. Specifying a contact person when the representative is not an individual is also a step that is frequently overlooked. This results in unclear representation authorizations and can hinder the representative's ability to act on the taxpayer's behalf effectively.

The choice between General Authorization and Limited Authorization in Part 3 is another critical decision area fraught with errors. Some individuals mistakenly assume that checking the General Authorization box is always the best option, not realizing that they can limit their representative’s powers for specific tax/nontax matters by selecting Limited Authorization and providing the necessary details. This imprecision can give representatives broader access than intended.

Another error made is not specifying the type of tax, form, or the year(s) or period(s) when opting for Limited Authorization. This oversight can lead to a lack of clarity about which matters the representative is authorized to handle, potentially leaving some issues unaddressed or giving the representative unintended authorization scope.

Part 4, which addresses changes in Power of Attorney representation or revocation, is also a section where misunderstandings occur. Users often fail to realize that this form, unless other powers of attorney are attached and specified, replaces all earlier powers of attorney for the same matters and periods. Forgetting to attach or specify which previous authorizations should remain effective can unintentionally nullify previous arrangements.

A frequent oversight in Part 5 involves the taxpayer’s signature. It’s not uncommon for taxpayers to forget to sign the form, or in the case of a joint representation, for one spouse to sign but not the other. Without the required signatures, the form is not valid and will not be processed, leading to delays in representation.

Lastly, a significant error involves the mailing process of the completed form. Taxpayers often send the form to the wrong address or omit necessary attachments. The Michigan 151 form instructions specify different mailing addresses depending on the taxpayer’s specific circumstances and the department requesting the form. Sending the form to the incorrect address can result in processing delays or the form not being processed at all.

Documents used along the form

The Michigan 151 form, serving as a vital document for granting power of attorney in tax, benefit, or debt matters to a representative in Michigan, often necessitates complementary forms and documents for a thorough legal procedure. These additional documents ensure transparent, comprehensive, and specific designations of authority and information sharing between a taxpayer and their appointed representative.

- Form 2848, Power of Attorney and Declaration of Representative: This federal form is similar to Michigan's Form 151 but is used for authorizing representation before the IRS. Individuals and businesses utilize it for tax matters that require federal attention, granting a chosen representative the ability to receive confidential tax information and make decisions on the taxpayer's behalf.

- Form 8821, Tax Information Authorization: While this document does not grant the broad representative powers of Form 151 or 2848, it allows a designated person or organization to review and receive confidential tax information from the IRS or state tax authorities. It is crucial for situations where a taxpayer needs someone to access their tax records without making decisions or negotiating with tax agencies.

- MICH-1040, Individual Income Tax Return: Taxpayers often file their annual state tax returns using this form. When a representative is acting on behalf of an individual in affairs related to state taxes, having this form filed correctly is essential. The appointed power of attorney may need access to this information for discussions or disputes with the Michigan Department of Treasury.

- Business Tax Registration Form: For businesses operating in Michigan, this document is necessary for obtaining a tax ID and registering for applicable state taxes. Representatives designated through Form 151 might need to file or amend these registrations if they manage the business's tax accounts.

In conjunction with the Michigan 151 form, these documents create a framework for both individuals and businesses to manage their tax and legal representations effectively. They ensure that all parties have the necessary authority and information to act in the best interests of the taxpayer, whether dealing with routine filings or more complex legal negotiations.

Similar forms

The Michigan 151 form, known for providing a method to authorize representatives in handling tax, benefit, or debt matters, possesses characteristics similar to various other legal and administrative documents that facilitate representation or information authorization. These similarities include the structure of designating representatives, specifying the scope of authority, and identifying particular matters or periods concerned. Below are documents that share similarities with the Michigan 151 form:

- IRS Form 2848 (Power of Attorney and Declaration of Representative): This form enables individuals or entities to appoint representatives for tax purposes, similar to the Michigan 151 form but on a federal level. Both forms require detailed information about the representative and the specific powers granted.

- Durable Power of Attorney for Health Care: This document permits an individual to appoint someone else to make healthcare decisions on their behalf if they become unable to do so. While it covers health decisions instead of tax matters, the fundamental concept of appointing and designating the extent of a representative’s authority mirrors that of the Michigan 151 form.

- Financial Power of Attorney: This authorizes a representative to handle an individual's financial affairs. Like the Michigan 151, it necessitates specifying which actions the representative can perform, although it focuses on broader financial matters rather than specifically on tax-related issues.

- Form SS-4 (Application for Employer Identification Number): While primarily an application form, it includes sections for third-party designees who are authorized to act on behalf of the entity in dealing with the IRS, sharing the element of third-party representation with the Michigan 151 form.

- State Tax Power of Attorney Forms: Similar to the Michigan 151 form but for other states, these documents grant representatives the power to handle tax matters on behalf of an individual or business with state tax agencies.

- Real Estate Power of Attorney: This legal document allows an individual to designate another person to manage real estate affairs. Its similarity lies in the delegation of specific responsibilities and the detailed enumeration of authorized actions, akin to the tax representation focus of the Michigan 151 form.

- Vehicle Power of Attorney: This document grants a representative the authority to handle matters related to the ownership or sale of a vehicle. It parallels the Michigan 151 form in giving someone else the legal authority to act in specific scenarios.

- Advance Directive: Though typically related to health care decisions, this document shares the principle of pre-appointing representatives to act on one's behalf, highlighting the overarching theme of designated representation found in the Michigan 151 form.

- Unemployment Benefits Authorization Form: Some states have specific forms that allow individuals to authorize representatives to assist with or manage their unemployment claims, reflecting the unemployment compensation aspect of the Michigan 151 form.

Each document, while unique in its jurisdiction, purpose, or specific use, shares the fundamental characteristic of enabling an individual or entity to formally designate others to act on their behalf, specifying the extent and limits of the authority given. This principle is crucial for ensuring that the appointed representatives exercise their powers within the bounds of the grantor's intentions and legal requirements.

Dos and Don'ts

Filling out the Michigan 151 form, which is crucial for appointing a representative for tax, benefit, or debt matters in the State of Michigan, requires attention to detail and a thorough understanding of your rights and responsibilities. Below are several do's and don'ts to guide you through the process.

- Do read the instructions on page 2 carefully before starting to fill out the form to ensure you understand each part and its requirements.

- Do complete all required fields in Part 1 with accurate taxpayer information, including your name, address, and Social Security number or Federal Employer Identification Number (FEIN), as applicable.

- Do provide clear and detailed information about the representative in Part 2, including their name, contact information, and the dates their authorization begins and ends.

- Do decide between General Authorization and Limited Authorization in Part 3 by considering the level of access and decision-making power you want to grant to your representative.

- Do ensure that both you and your spouse (if applicable) sign and date the form in Part 5 to validate the Power of Attorney Authorization.

- Don't leave out any representative information, including email addresses and phone numbers, to avoid any delays or issues in communication with the Michigan Department of Treasury or Bureau of Workers' & Unemployment Compensation (BW&UC).

- Don't forget to specify the type of tax, type of form, and years or periods if you choose Limited Authorization to ensure clarity regarding the scope of your representative's powers.

By following these guidelines, you can accurately complete the Michigan 151 form, ensuring that your appointed representative has the correct authorization to manage your tax, benefit, or debt matters with the State of Michigan. Remember, completing this form correctly is essential for both your financial security and compliance with state regulations.

Misconceptions

There are several misconceptions about the Michigan Department of Treasury and Bureau of Workers' & Unemployment Compensation (BW&UC) 151 form, commonly known as the Power of Attorney Authorization. Understanding these misconceptions is crucial for accurate completion and submission of the form.

One form fits all: Some people believe that a single Michigan 151 form can cover multiple representatives. However, a separate form is required for each representative you wish to authorize. This ensures clear authority and representation for each appointed individual or organization.

Duration of authorization is indefinite: There's a misconception that once authorized, the representative has indefinite power unless the taxpayer revokes it. In reality, the form requires specification of both beginning and ending authorization dates, unless intentionally left open-ended by the taxpayer, in which case authorization continues until formally revoked.

Automatic inclusion of tax matters: Many believe that completing the form automatically authorizes the representative for all tax matters. The form, however, allows for both general and limited authorization. Taxpayers can specify which tax matters, forms, and periods the authorization covers under the limited authorization section.

Spousal representation without specification: It's incorrectly assumed that if one spouse completes the form, it automatically grants authorization for the representative to act on behalf of both spouses in joint tax matters. Each spouse must sign the form, and if appointing the same representative, their details must also be included on the form.

Power of Attorney does not need updating: Some think that once a Power of Attorney form is filed, it doesn't need to be updated unless the taxpayer wants to change representatives. This ignores the form's requirement to report changes in representation or to revoke a previous authorization, ensuring the Treasury and BW&UC records are current.

Informal revocation is sufficient: A common misunderstanding is that a Power of Attorney can be revoked verbally or through informal notification. To formally revoke a previous authorization, taxpayers must indicate their intention on the form and provide any existing powers of attorney that will remain effective alongside the new or revoking submission.

Correcting these misconceptions ensures that the Power of Attorney Authorization form is properly completed and processed, facilitating accurate and authorized representation before the State of Michigan on tax, benefit, or debt matters.

Key takeaways

Filling out and using the Michigan 151 form is an important process for taxpayers who wish to appoint a representative for their tax, benefit, or debt matters with the state. Here are four key takeaways to ensure the process is completed smoothly:

- Accurate Information is Crucial: Part 1 of the form requires detailed taxpayer information. It is important to provide accurate details including the taxpayer's name, address, telephone and fax numbers, e-mail address, Social Security number (SSN), Federal Employer Identification Number (FEIN), and Unemployment Compensation Account Number. If the taxpayer is a business, the DBA, trade, or assumed name must be included. Ensuring this information is accurate and complete is essential for the form's acceptance.

- Separate Forms for Each Representative: If appointing more than one representative, a separate Michigan 151 form must be filled out for each. Part 2 of the form collects the representative’s information, including name, address, telephone and fax numbers, and e-mail address. A contact person must be designated if the representative is an organization or firm. This section also requires specifying the start and end date of the authorization.

- Clarifying the Scope of Authorization: The form offers two types of authorization - General and Limited. General authorization grants the representative broad powers across all tax/non-tax matters and for all years or periods. In contrast, Limited authorization restricts the representative’s powers to specific tax matters, forms, and time periods, as explicitly stated on the form. Choosing the correct type of authorization is critical to align with the taxpayer's needs and intentions.

- Revocation and Replacement of Previous Powers: Filing the Michigan 151 form can serve to replace or revoke any previous power of attorney authorizations on file for the same matters. It is important to attach copies of any powers of attorney that need to remain in effect alongside the new form. Part 4 of the form is dedicated to this aspect, ensuring that taxpayers can easily manage their representation preferences.

Understanding these key aspects of the Michigan 151 form helps taxpayers efficiently navigate the process of assigning a representative for their dealings with the Michigan Department of Treasury and the Bureau of Workers' & Unemployment Compensation (BW&UC). Proper completion and submission of this form is a necessary step for those wishing to have representation in tax-related matters.

Popular PDF Templates

What Is a Sales Tax Permit - Information on Michigan's Corporate Income Tax (CIT) for entities is thoroughly explained.

What Reasons Can You Quit a Job and Still Get Unemployment Michigan - Companies must submit this form to report their assets and operations for the preceding year, ensuring accurate taxation.