3372 Michigan PDF Form

In an environment where every penny counts, understanding and correctly applying for tax exemptions can significantly impact a business’s bottom line. The Michigan Sales and Use Tax Certificate of Exemption, known formally as Form 3372, plays a critical role for businesses operating within Michigan. This form allows businesses to claim exemptions from sales and use tax on eligible transactions, covering a wide array of situations from one-time purchases to recurring business relationships. With its clear structure, the form demands meticulous completion across four comprehensive sections, including the type of purchase, specific items covered by the certificate, the basis for the exemption claim, and, finally, a certification section where the purchaser attests to the accuracy and validity of their claim under penalty of perjury. Each section serves as a pillar, upholding the integrity and purpose of the form – to facilitate tax compliance while recognizing valid exemption statuses. Not only does this form require the purchaser to declare the nature of the exempt purchase, but it also imposes a significant responsibility to provide accurate information or face possible penalties, including tax repayment with interest and potential fines. Additionally, it serves as a reminder of the importance of keeping detailed records, as all claims made using this certificate are subject to audit by the Michigan Department of Treasury. Thus, Form 3372 is not merely a procedural document but a critical tool for businesses seeking to navigate the complexities of Michigan’s tax landscape efficiently and effectively.

Preview - 3372 Michigan Form

Michigan Department of Treasury 3372 (Rev.

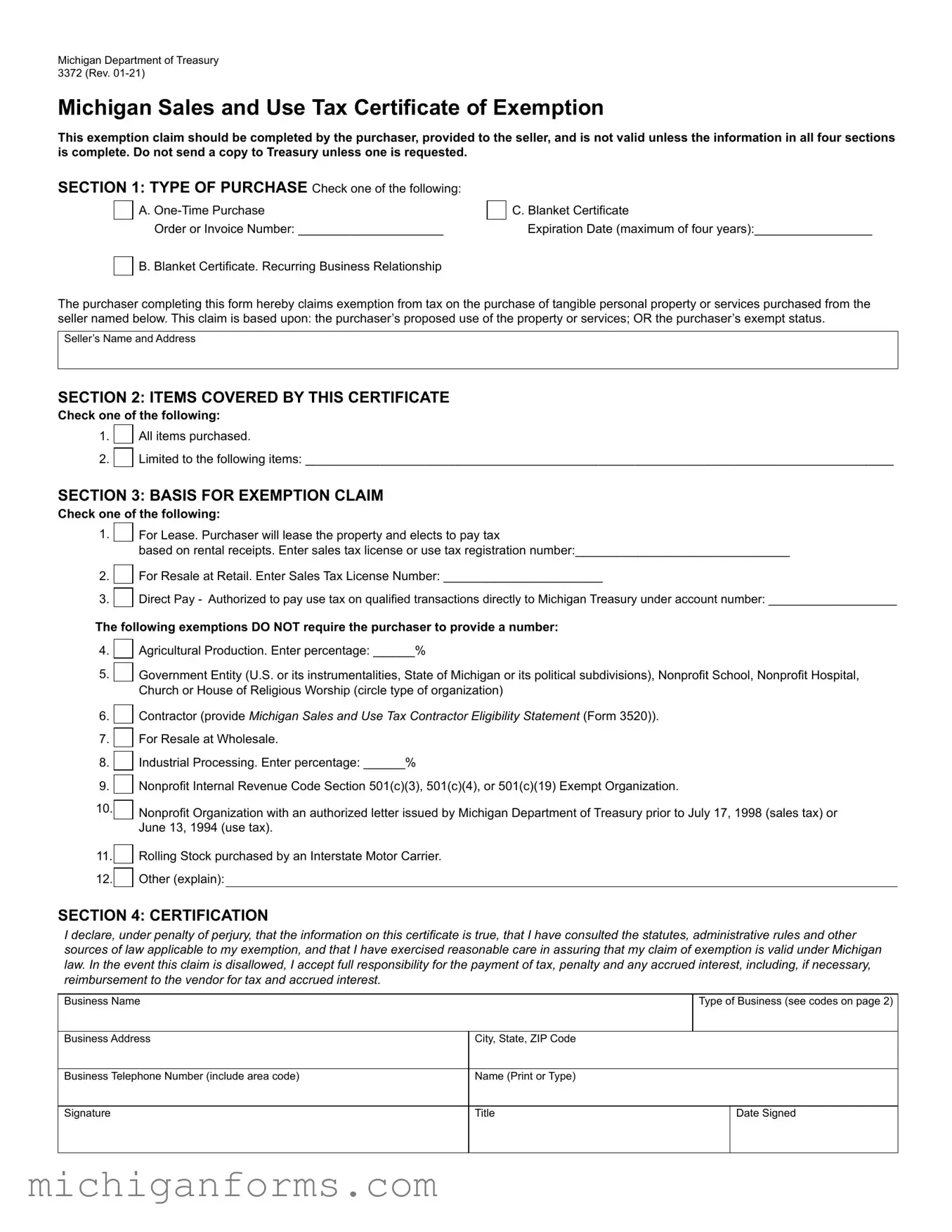

Michigan Sales and Use Tax Certificate of Exemption

This exemption claim should be completed by the purchaser, provided to the seller, and is not valid unless the information in all four sections is complete. Do not send a copy to Treasury unless one is requested.

SECTION 1: TYPE OF PURCHASE Check one of the following:

A.

Order or Invoice Number: _____________________

B. Blanket Certificate. Recurring Business Relationship

C. Blanket Certificate

Expiration Date (maximum of four years):_________________

The purchaser completing this form hereby claims exemption from tax on the purchase of tangible personal property or services purchased from the seller named below. This claim is based upon: the purchaser’s proposed use of the property or services; OR the purchaser’s exempt status.

Seller’s Name and Address

SECTION 2: ITEMS COVERED BY THIS CERTIFICATE

Check one of the following:

1. |

|

All items purchased. |

2. |

|

Limited to the following items: _____________________________________________________________________________________ |

|

SECTION 3: BASIS FOR EXEMPTION CLAIM

Check one of the following:

1.

2.

3.

For Lease. Purchaser will lease the property and elects to pay tax

based on rental receipts. Enter sales tax license or use tax registration number:_______________________________

For Resale at Retail. Enter Sales Tax License Number: _______________________

Direct Pay - Authorized to pay use tax on qualified transactions directly to Michigan Treasury under account number: ___________________

The following exemptions DO NOT require the purchaser to provide a number:

4. |

|

Agricultural Production. Enter percentage: ______% |

|

5. |

|

Government Entity (U.S. or its instrumentalities, State of Michigan or its political subdivisions), Nonprofit School, Nonprofit Hospital, |

|

|

|||

|

|

Church or House of Religious Worship (circle type of organization) |

|

6. |

|

Contractor (provide Michigan Sales and Use Tax Contractor Eligibility Statement (Form 3520)). |

|

|

|||

7. |

|

For Resale at Wholesale. |

|

|

|||

8. |

|

Industrial Processing. Enter percentage: ______% |

|

|

|||

9. |

|

Nonprofit Internal Revenue Code Section 501(c)(3), 501(c)(4), or 501(c)(19) Exempt Organization. |

|

|

|||

10. |

|

Nonprofit Organization with an authorized letter issued by Michigan Department of Treasury prior to July 17, 1998 (sales tax) or |

|

|

|||

|

|

June 13, 1994 (use tax). |

|

11. |

|

Rolling Stock purchased by an Interstate Motor Carrier. |

|

|

|||

12. |

|

Other (explain): |

|

|

|||

SECTION 4: CERTIFICATION

I declare, under penalty of perjury, that the information on this certificate is true, that I have consulted the statutes, administrative rules and other sources of law applicable to my exemption, and that I have exercised reasonable care in assuring that my claim of exemption is valid under Michigan law. In the event this claim is disallowed, I accept full responsibility for the payment of tax, penalty and any accrued interest, including, if necessary, reimbursement to the vendor for tax and accrued interest.

Business Name |

|

Type of Business (see codes on page 2) |

|

|

|

|

|

Business Address |

City, State, ZIP Code |

|

|

|

|

|

|

Business Telephone Number (include area code) |

Name (Print or Type) |

|

|

|

|

|

|

Signature |

Title |

|

Date Signed |

|

|

|

|

3372, Page 2

Instructions for completing Michigan Sales and Use Tax Certificate of Exemption (Form 3372)

Purchasers may use this form to claim exemption from Michigan sales and use tax on qualified transactions. All fields must be completed; however, if provided to the purchaser in electronic format, a signature is not required. All claims are subject to audit. The purchaser must ensure eligibility of the exemption claimed; a purchaser who improperly claims an exemption is liable for tax, penalty, and interest, with limited exceptions.

Sellers: Michigan does not issue “tax exempt numbers” and a seller is not permitted to rely on a number in lieu of a valid exemption

claim. Sellers are required to maintain proper records of exempt sales, including exemption forms or the same information in another format. Records may be kept electronically. If the exemption certificate is received in electronic format, a signature is not required. A

seller who does not comply with these requirements may be liable for tax, penalty, and interest. See Revenue Administrative Bulletin

SECTION 1:

A)Choose

B)Choose “Blanket Certificate” if there is a “recurring business relationship.” This exists when a period of not more than 12 months elapses between sales transactions between the seller and purchaser. Parties do not need to renew this blanket exemption claim as long as the recurring business relationship exists.

C)Choose “Blanket Certificate” and enter the expiration date (maximum four years) when there may be a period of more than 12 months between sales transactions. This option is best when purchaser and seller anticipate more than one exempt transaction before the expiration date but do not have or may not maintain a recurring business relationship.

SECTION 2:

Place a check in the box for “All items purchased” or choose “Limited to” and list the items that are covered by the exemption claim.

SECTION 3:

Check the box that applies and, if applicable, provide the required information. The exemptions listed are the most common. If the exemption you are claiming is not listed, check “Other” and enter the qualifying exemption.

SECTION 4:

Purchaser must complete Section 4. A signature is only required if a paper form is used; in that case, the purchaser should sign and provide their title (for example, Purchasing Manager, President, Owner). For Type of Business, enter the number from the following list that best describes the purchaser’s business.

01 |

Accommodations |

10 |

Utilities |

02 |

Agricultural |

11 |

Wholesale |

03 |

Construction |

12 |

Advertising, newspaper |

04 |

Manufacturing |

13 |

|

05 |

Government |

14 |

|

06 |

Rental or leasing |

15 |

|

07 |

Retail |

16 |

Other (enter code and write in business type) |

08 |

Church |

|

|

09 |

Transportation |

|

|

Form Characteristics

| Fact Number | Description |

|---|---|

| 1 | The form is designated for the Michigan Department of Treasury 3372 (Rev. 01-21). |

| 2 | It is utilized to claim exemption from Michigan sales and use tax. |

| 3 | Completion and provision to the seller by the purchaser are mandatory; it is not valid unless fully completed. |

| 4 | Sending a copy to the Treasury is not required unless specifically requested. |

| 5 | Eligibility for exemption can be based on the purchaser’s use of the property or services, or the purchaser's exempt status. |

| 6 | There are options for one-time purchase or blanket certificate, with or without an expiration date. |

| 7 | It covers a variety of exemption reasons, including for resale, agricultural production, government entities, and nonprofit organizations. |

| 8 | Records of exempt sales must be properly maintained by the seller, whether in paper or electronic format. |

| 9 | Governing laws include Michigan sales and use tax laws, alongside Revenue Administrative Bulletin 2016-14 regarding exemption claims and record-keeping. |

Guidelines on Utilizing 3372 Michigan

Filling out the Michigan Department of Treasury 3372, the Sales and Use Tax Certificate of Exemption, is a crucial step for businesses and individuals looking to claim exemption from tax on eligible transactions. This document must be completed with great attention to detail to ensure accuracy and compliance with Michigan laws. Each section of the form requires specific information that substantiates the exemption claim, making it imperative that the purchaser carefully reviews and understands the requirements before submission. Below are the step-by-step instructions to accurately fill out the form.

- Section 1: Type of Purchase

- Choose “One-Time Purchase” and enter the invoice number if the certificate covers a single transaction.

- Select “Blanket Certificate” if there’s a recurring business relationship, defined as sales transactions not exceeding 12 months apart.

- If choosing “Blanket Certificate” for purchases expected over a period longer than 12 months, enter the expiration date, up to a maximum of four years.

- Section 2: Items Covered by This Certificate

- Mark the checkbox for “All items purchased” if the certificate applies to all transactions.

- If the exemption only covers certain items, select “Limited to” and clearly list those items.

- Section 3: Basis for Exemption Claim

- Check the appropriate box that represents the basis of your exemption claim. Provide any additional requested information, such as license numbers or percentages.

- If the specific exemption basis is not listed, choose “Other” and provide a detailed explanation of the qualifying exemption.

- Section 4: Certification

- Though a signature is not required for electronic submissions, ensure that all other information, including the business’s name, address, telephone number, and the type of business, is accurately filled.

- If submitting a paper form, sign and date the certificate and provide your title.

Once the form is fully completed, it should be provided to the seller, not sent to the Treasury unless requested. This certificate plays a vital role in documenting tax-exempt transactions and should be retained by the seller for record-keeping purposes. Accuracy is key, as any incorrect claims may result in the purchaser being responsible for tax, penalty, and interest. Understanding and properly applying the guidelines for filling out the Michigan 3372 form not only simplifies the process but also ensures compliance with Michigan tax laws.

Crucial Points on This Form

What is the Michigan Form 3372 used for?

The Michigan Form 3372, known as the Michigan Sales and Use Tax Certificate of Exemption, is a document that allows purchasers to claim exemption from sales and use tax on eligible transactions in Michigan. This form is completed by the purchaser and provided to the seller to document the tax-exempt purchase of tangible personal property or services. It is crucial for both purchasing and selling parties as it outlines the basis for the exemption claim, ensuring compliance with Michigan tax law.

How do I complete the Michigan Form 3372?

To accurately complete the Michigan Form 3372, follow these steps:

- Section 1: Type of Purchase - Indicate whether the form covers a one-time purchase or if it is a blanket certificate for recurring transactions. If it’s a blanket certificate, include the expiration date.

- Section 2: Items Covered by This Certificate - Specify if the exemption claim covers all items purchased or limit the exemption to certain items.

- Section 3: Basis for Exemption Claim - Check the appropriate box that applies to your exemption claim and provide any required information, such as sales tax license numbers or the percentage of use for agricultural production or industrial processing.

- Section 4: Certification - This section must be completed by the purchaser, including typing or printing the name of the person completing the form, their title, and the date signed. A signature is required for paper submissions, but not for electronic submissions.

Do I need to send a copy of this form to the Michigan Department of Treasury?

No, a copy of the Michigan Form 3372 should not be sent to the Michigan Department of Treasury unless specifically requested. The seller keeps the form to substantiate the exempt transaction. It is essential for both parties to keep a copy of this form for their records in case of an audit.

What happens if I incorrectly claim an exemption using the Michigan Form 3372?

If an exemption is claimed incorrectly using the Michigan Form 3372, the purchaser is liable for the unpaid tax, in addition to any applicable penalties and interest. It is the purchaser’s responsibility to ensure the eligibility of the exemption claimed and to provide accurate information. If the exemption claim is disallowed upon review or audit, the purchaser must rectify the situation by reimbursing the vendor for the tax and possibly accrued interest.

How long should I keep the Michigan Form 3372 for my records?

It is recommended that both the purchaser and seller retain a copy of the completed Michigan Form 3372 for at least four years after the transaction. This retention period aligns with tax audit practices and ensures that both parties can substantiate the exemption claim if reviewed by the Michigan Department of Treasury.

Common mistakes

One common mistake when filling out the 3372 Michigan Sales and Use Tax Certificate of Exemption lies in the handling of Section 1: TYPE OF PURCHASE. Purchasers often incorrectly choose between "One-Time Purchase" and "Blanket Certificate" options. This decision is pivotal because it dictates how the form applies to transactions. A One-Time Purchase selection should only be used for a singular transaction, whereas a Blanket Certificate applies to ongoing purchases from the same seller. When the wrong option is selected, it can lead to the form not covering all intended transactions or requiring unnecessary paperwork for a single purchase.

In Section 2: ITEMS COVERED BY THIS CERTIFICATE, a frequent mistake is failing to specify the items covered when the "Limited to" option is chosen. This section requires clarity to ensure both the purchaser and seller understand which items the exemption applies to. General or vague descriptions can lead to confusion and potential disputes during tax audits. It's crucial to list the exempt items or services explicitly to avoid any ambiguity regarding the exemption's applicability.

Another area prone to errors is Section 3: BASIS FOR EXEMPTION CLAIM. Here, purchasers must select the basis for their exemption claim and, in some cases, provide additional information such as a sales tax license number or a use tax registration number. Not providing these details, when applicable, can invalidate the exemption claim. Additionally, choosing the incorrect basis for exemption because of a misunderstanding of how an exemption category applies to the purchaser's situation can lead to the claim being disallowed, resulting in the purchaser being liable for tax, penalty, and interest.

Last but not least, Section 4: CERTIFICATION is often overlooked in terms of importance. This section requires a declaration under penalty of perjury that the information provided on the certificate is true and accurate. A signature is necessary when the form is provided in paper format. However, a key mistake made by purchasers is not signing the form or providing the relevant business title. This oversight can lead to the exemption certificate being considered invalid. It is vital to complete this section fully and accurately to affirm the exemption claim's legitimacy.

Documents used along the form

When filing the Michigan Department of Treasury 3372, Michigan Sales and Use Tax Certificate of Exemption, several other forms and documents are often required to ensure comprehensive compliance and accurate reporting. These documents support various exemption claims and provide detailed business information needed for verification purposes. Understanding each document ensures a smoother process.

- Form 3520, Michigan Sales and Use Tax Contractor Eligibility Statement: This form is specifically for contractors to declare their eligibility for certain exemptions. The form enables contractors to buy or rent tangible personal property or services tax-free for use in specific projects.

- Michigan Sales Tax License: A fundamental document that verifies a business is registered with the Michigan Department of Treasury to collect sales tax. It is crucial for businesses making sales at retail or providing taxable services in Michigan.

- Use Tax Registration Number: Similar to the Sales Tax License, this number is for businesses that need to report use tax. It's essential for those who purchase tangible goods or services for use, storage, or consumption in Michigan where sales tax was not charged at the time of purchase.

- Nonprofit Exemption Letter from Michigan Department of Treasury: This document confirms a nonprofit organization's tax-exempt status under Michigan law. It is necessary for nonprofits claiming exemption on purchases related to their exempt activities.

- IRS Determination Letter: This federal document affirms an organization's tax-exempt status under the Internal Revenue Code. It supports exemption claims by verifying the entity's nonprofit status.

- Agricultural Exemption Certificate: Utilized by those in agricultural production to buy goods and services without paying sales tax on items used exclusively in farming and agricultural operations.

Collecting and preparing the right documentation is critical for accurately filing the Michigan Sales and Use Tax Certificate of Exemption (Form 3372). Each document plays a vital role in substantiating the exemption claim, reducing the likelihood of errors or audits. Remember, these forms and documents not only ensure compliance but also protect your business by establishing a clear record of exemptions claimed.

Similar forms

The Streamlined Sales and Use Tax Agreement Certificate of Exemption is similar because it is also designed to help businesses and organizations claim exemptions on applicable sales and use taxes for purchases or leases, specifying the reason for exemption.

Resale Certificate shares similarities, as it is used by purchasers who are buying an item intending to resell it, which aligns with the resale exemption option on the Michigan form.

Exemption Certificate for Government Agencies parallels the Michigan form's option for government entities to claim exemption, specifying the nature of the governmental or nonprofit entity making the purchase.

The Nonprofit Exemption Certificate corresponds closely with the sections of the form dedicated to nonprofit organizations, recognizing their tax-exempt status for purchases related to their operations.

Agricultural Exemption Certificate finds its counterpart in the agricultural production exemption claim available in the form, allowing for tax exemption on purchases related to agricultural operations.

An Industrial Processing Exemption Certificate is akin to the form's option for claiming exemptions for items used in industrial processing, providing a way to avoid sales tax on materials that are part of a manufacturing process.

The Direct Pay Permit resembles the direct pay authorization on the form, which lets entities pay use tax directly to the Michigan Department of Treasury on qualified transactions.

A Contractor's Exemption Certificate is related to the section on the form that allows contractors to claim exemptions, typically for materials used in real property improvements or construction projects.

The Use Tax Certificate of Exemption is similar in its purpose of allowing businesses or individuals to claim an exemption from use tax under specific circumstances, paralleling the form's broader use for both sales and use tax exemptions.

Motor Carrier Exemption Certificate links to the exemption claim for rolling stock purchased by an interstate motor carrier, offering a tax exemption on vehicles used in interstate commerce.

Dos and Don'ts

When filling out the 3372 Michigan form, which is crucial for claiming sales and use tax exemptions, it's essential to follow specific dos and don'ts to ensure the process is completed accurately and efficiently. Below are five key things you should do, along with five things you should avoid.

Do the following:

- Read the instructions carefully before starting the form to understand each section's requirements and ensure all necessary information is provided correctly.

- Choose the correct type of purchase at the beginning of the form (One-Time Purchase or Blanket Certificate) and include all relevant details, such as invoice numbers or expiration dates, as applicable.

- Be clear and specific when listing the items covered by the exemption in Section 2 to prevent any confusion regarding what is exempt from tax.

- Check the appropriate basis for the exemption claim in Section 3 and provide any required information, such as license numbers or exemption percentages, to validate your claim.

- Ensure the certification in Section 4 is signed if submitting a paper copy of the form. A digital form may not require a signature, but it's crucial to verify that all provided information is accurate and true.

Avoid the following:

- Do not leave any sections incomplete. Failing to fill out all the required fields can result in the form being invalid or delay the processing of your exemption claim.

- Avoid guessing or making assumptions about which exemptions apply to your purchase. If uncertain, review the Michigan Department of Treasury guidelines or seek clarification.

- Do not forget to check whether you’re eligible for the claimed exemption. Improperly claimed exemptions can lead to liability for tax, penalty, and interest.

- Avoid using outdated forms. Always ensure you are completing the latest version of the form (Rev. 01-21) to comply with current tax laws and regulations.

- Do not send the completed form to the Treasury unless specifically requested. This form should be provided to the seller for their records to substantiate the tax-exempt sale.

Misconceptions

Misconceptions surrounding the Michigan Department of Treasury 3372 form, known as the Michigan Sales and Use Tax Certificate of Exemption, abound, ranging from its purpose to specifics about completion and qualifications. Understanding these misconceptions is crucial for businesses and individuals aiming to utilize the form correctly.

- Misconception 1: The form must be sent to the Michigan Department of Treasury immediately upon completion.

This form should not be sent to the Treasury unless specifically requested. It is primarily a document exchanged between the purchaser and the seller to claim a tax exemption on qualified transactions.

- Misconception 2: A digital signature is always required.

If the form is provided in electronic format, a signature is not necessary for the exemption claim to be valid. This adjustment accommodates modern, paperless transactions.

- Misconception 3: The form grants an automatic exemption for all purchases.

Exemptions are specific to the transactions that meet the qualifications outlined in the form. Claims must be based on the purchaser's intended use of the property or services, or the purchaser's exempt status. This means not all purchases may qualify for exemption.

- Misconception 4: Every section must be filled out for every transaction.

While all sections must be completed for the form to be valid, the details required vary depending on the type of purchase and the basis for the exemption claim. The form is designed to accommodate a range of transaction types, including one-time purchases and recurring business relationships.

- Misconception 5: A "tax exempt number" from the Michigan Department of Treasury is required to claim an exemption.

Michigan does not issue "tax exempt numbers". Sellers are instructed not to rely on such a number but rather to assess the validity of each exemption claim based on the information provided in the form.

- Misconception 6: The form serves as a blanket exemption for all future purchases.

While the form can be used to establish a blanket certificate for recurring transactions with the same seller, each transaction must still qualify under the provided exemption categories. Blanket certificates also have an expiration date, further limiting their scope.

- Misconception 7: Sellers bear no responsibility for the accuracy of the information on the form.

Sellers are required to maintain accurate records of exempt sales and ensure that the exemption claims received are valid. Failure to do so could result in the seller being liable for uncollected tax, penalty, and interest.

- Misconception 8: Only physical goods are covered by this exemption certificate.

The certificate can be used for both tangible personal property and certain services, highlighting the form's versatility in accommodating a wide range of exempt transactions under Michigan law.

- Misconception 9: The exemption claim is valid indefinitely.

Claims of exemption are subject to audit and must be reasserted for each transaction or covered period. Additionally, blanket certificates have a maximum validity of four years, after which a new certificate must be filed for ongoing transactions.

Addressing these misconceptions is essential for correctly applying the 3372 Michigan form, ensuring compliance, and taking advantage of the exemptions it offers. Both purchasers and sellers need to be aware of these nuances to navigate Michigan's sales and use tax regulations effectively.

Key takeaways

The Michigan Department of Treasury provides Form 3372, a Sales and Use Tax Certificate of Exemption, which enables purchasers to claim exemption from sales and use tax on eligible transactions. Understanding and precisely completing this form is crucial for both buyers and sellers to ensure compliance with Michigan tax laws.

The form demands detailed information across four sections, covering the type of purchase, items covered, the basis for exemption claim, and certification by the purchaser. Failing to completely fill out any part may invalidate the exemption claim.

Section 1 requires a selection between "One-Time Purchase" and "Blanket Certificate," contingent on whether the purchase is singular or expected to recur within or beyond a 12-month period, respectively. The "Blanket Certificate" can have a validity of up to four years.

In Section 2, purchasers specify whether the exemption is for all items purchased or limited to specific items, thereby providing clear guidance on the applicability of the exemption.

The form outlines various bases for exemption in Section 3, including but not limited to resale, agricultural production, government entities, and certain nonprofit organizations. Detailed documentation and specific identifications may be required to substantiate the claim.

Importantly, the form emphasizes the purchaser's responsibility for ensuring the legitimacy of the exemption claim. Erroneous exemption claims can lead to the purchaser being liable for unpaid taxes, penalties, and interest.

Maintaining accurate records of exempt sales is imperative for sellers. Michigan does not issue tax-exempt numbers, hence relying solely on such a number in place of a completed Form 3372 does not constitute a valid exemption claim.

All exemption claims made through Form 3372 are subject to audit by the Michigan Department of Treasury. Both sellers and purchasers should exercise due diligence in documenting and verifying the accuracy of the information provided to uphold compliance and avoid potential penalties.

Correct and mindful completion of Form 3372 is a shared responsibility between the purchaser and seller. It serves as a vital tool in the prudent management of tax liabilities and ensures both parties adhere to Michigan's tax regulations.

Popular PDF Templates

Michigan Amended Tax Return Instructions - MI-1040X-12 forms must be filed only after the original tax return has been processed by the Michigan Department of Treasury.

Michigan Tax Exempt Form - The form requires a detailed description of the business activity, along with the start date of the business in the local tax collecting unit.